ESG & Mandate Risk

Recent events in various US jurisdictions have highlighted an important set of questions around ESG investing. We believe these need to be considered by those holding a position of trust in the management of investor funds. Specifically, questions have been raised publicly about the nature and form of mandates governing the actions of funds.

In this blog we take no sides in the question of whether ESG investing adds value. Instead, we take a closer look at questions related to investment mandates under ESG and find that it may be worth those with fiduciary responsibilities taking their mandate into full and frank account.

Recent Challenges

Environmental, Social and Governance – ESG - investment platforms made unexpected headlines in the United States through Q3.

This included certain reports.

19 US state attorneys general wrote to BlackRock, arguing that the investment manager’s ESG investment policies may violate the ‘sole interest’ rule, which in the US requires that conflicts of interest in fiduciary relationships be avoided.

Attorneys General in Indiana and Louisiana issued warnings to their respective state pension boards that ESG investing may be a violation of their fiduciary duty.

West Virginia barred Blackrock, JPMorgan, Goldman Sachs, Morgan Stanley and Wells Fargo from contracting for new business in the state after determining that through ESG policies they were boycotting the fossil fuel industry.

Texas identified 10 companies, and 348 investment funds whom legislators labelled ‘boycott energy companies’, including BlackRock, Credit Suisse and UBS, prohibiting them from contracting with state agencies and local governments.

Our attention was drawn to this by a recent Wall Street Journal piece which noted that the principles invoked in the letters sent to Blackrock are “part of the common and statutory laws of almost every state.”

While it may be tempting to dismiss the Journal’s authors as partisans assembling contestable assertions, see here and here, we leave the tactical debate to others, for example:

Harvard Business Review:

o Yes, Investing in ESG Pays Off; versus

o An Inconvenient Truth About ESG Investing,

What we find interesting is that:

The various state-based challenges reignite a debate around fiduciary responsibilities that emerged when Corporate Social Responsibility, started to emerge in the early 2000’s; and, more importantly

ESG investment may be argued to contravene the Uniform Prudent Investor Act, adopted by 44 US states and the District of Columbia, which states:

No form of so-called "social investing" is consistent with the duty of loyalty if the investment activity entails sacrificing the interests of trust beneficiaries – for example, by accepting below-market returns -- in favor of the interests of the persons supposedly benefitted by pursuing the particular social cause.

The Journal’s writers, William Barr and Jed Rubenfeld, go on to note that “a defence to ESG investing asserts that ESG factors, though nonpecuniary, are material to profitability and that ESG investing will therefore produce superior outcomes.”

This appears contestable, as the varying Harvard studies amply prove, but when canvassing for views from among Martialis clients and contacts one message stood out: most managers have been inundated with requests for ESG-overlay and careful observance, not the opposite.

Fiduciary Duty in Australia

We hope to follow up on this blog with a more detailed look at the nature of fiduciary responsibilities in an Australian context. The aim will be to get a much clearer definitional picture from experts, so watch for that in coming issues.

What we do note is that there appear to be similar provisions within the Corporations Act to those written-in to the US’s Uniform Prudent Investor act. For example, a responsibility under the Australian Act is that responsible entities (of registered schemes) duties include acting “in the best interests of the members and, if there is a conflict between the members' interests and its own interests, [to] give priority to the members' interests."

Perhaps the risk for fund directors lies in the definition of what constitutes a member's interests? Is it to maximise returns with an ESG filter or overlay, or simply to maximise returns?

In our view, risk here can likely be distilled into to a fundamental question of fund mandate.

Where a fund has ensured beneficiaries are aware of the nature of the decisions being made – whether ESG-based or otherwise – a mandate sets the parameters within which a portfolio is managed, thus setting properly informed beneficiary expectations.

But what of funds that have started overlaying ESG filters without addressing beneficiaries or their mandate?

To us, this seems problematic.

A problematic greenium

As the market transparency of ESG investing modes develops it will be increasingly easy for fund beneficiaries to assess the decision-making path of fund managers.

To reinforce this, we note that Bloomberg has embarked on an extensive ESG program designed collect some data to the ESG metrics.

Bloomberg’s Environmental, Social & Governance (ESG Data) dataset offers ESG metrics and ESG disclosure scores for more than 14,000 companies in 100+ countries. The product includes as-reported data and derived ratios as well as sector and country-specific data points. In addition to the extensive ongoing data coverage, we provide historical data going back to 2006.

This allows Bloomberg subscribers to gain access quite remarkable decision-making tools and transparency.

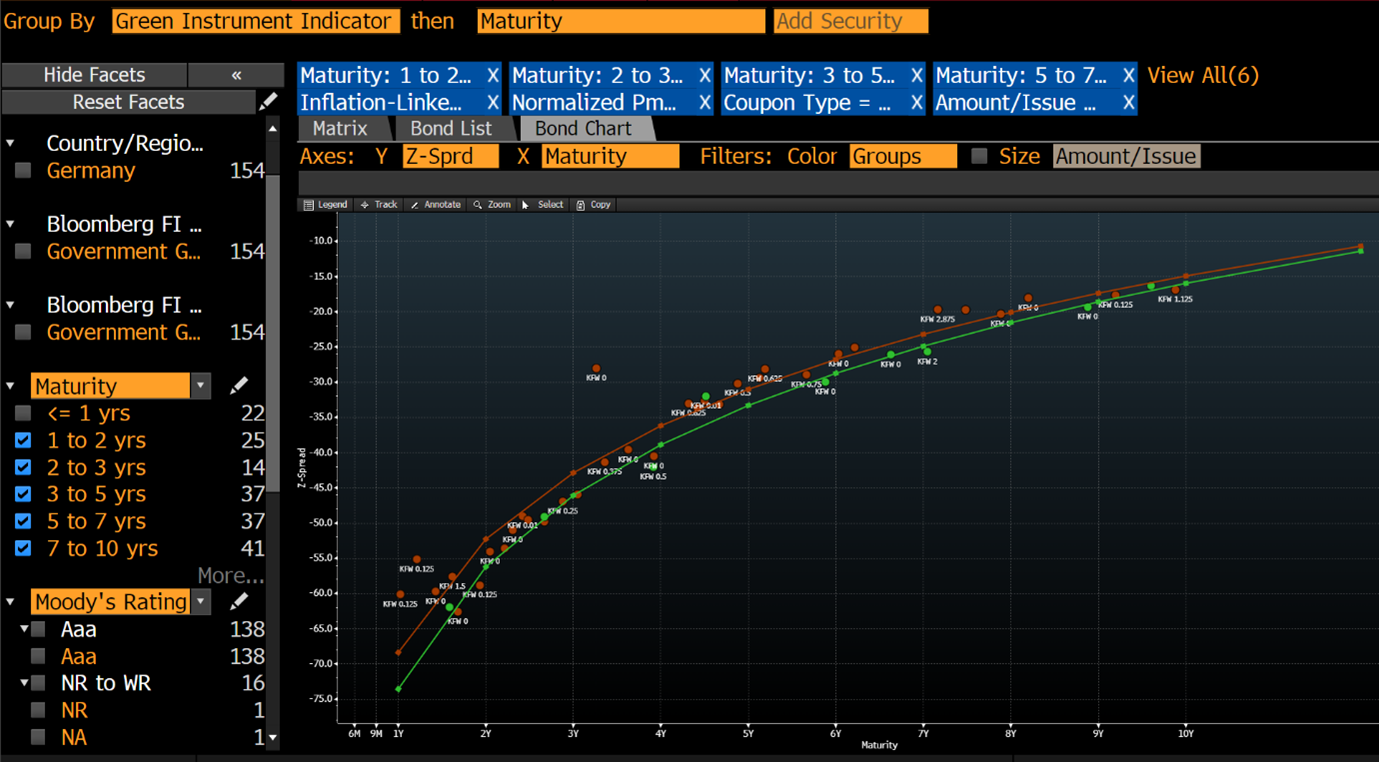

For example, here is a screenshot of Bloomberg’s Green Instrument Indicator:

Which means that transparency is assured.

What then of a situation in which, for example, a bond fund manager is considering a purchase of bonds/bunds of, say, a noted green issuer - the Federal Republic of Germany?

The German state issues both green and non-green bonds, and has gone to impressive lengths to distinguish between the two:

The use of proceeds from Green German Federal Securities always corresponds to federal expenditure from the previous year. Spending from the previous year’s budget that qualifies as “green” is assigned to the securities. The Green Bond Framework lists five main green expenditure categories that can be assigned to Green German Federal Securities.

These are:

Transport

International cooperation

Research, innovation and awareness raising

Energy and industry

Agriculture, forestry natural landscapes and biodiversity

Noting that the yield differential between a 10-year green and traditional bund is around 5.0 basis points, it’s not hard to see a potential fiduciary risk problem emerging.

If our bond fund manager notes the differing market yield representing the ‘greenium’ (which we imply as resulting in a lower monetary yielding outcome for the investor) and has no mandate for such a product we suggest there is a potential problem.

Why?

Because a beneficiary who considers their best interests to be served by owning higher yielding paper – irrespective of their views of ESG outcomes - could make the argument that the manager was in breach of their fiduciary duty. Transparency makes their argument much easier.

Which brings us back to the question of fund mandates, and several important questions:

· Is the fund mandate current?

· If mandate changes that were likely to diminish fund returns have been implemented, were beneficiaries advised of these changes?

Those holding fiduciary responsibilities should take their mandate into full and frank account, or at least ask two questions:

1. Is our mandate current?

2. Is our mandate clear?

Summary

ESG investing is very topical among investors. However, the investment mandates are important documents which need to be observed. In addition, regulators and legislators are now taking interest in the investments and often taking action to protect their industries.

We will be writing more on this in the near future.