We know it’s a global issue - Part II

In 2023, ASIC Chair Joseph Longo foreshadowed increased regulatory interest in the market practice of pre-hedging, noting that his commission was aware of industry calls for guidance on the topic.

ASIC followed this up with their Guidance for market intermediaries on pre-hedging in February. While this no doubt has been welcomed by the sell-side, there remains little to guide those who actually bring large or sensitive transactions to market on the buy-side.

In this blog I follow up my earlier work on this topic and put forward some possible points of buy-side guidance.

We’ve heard your calls for guidance, and we hope to provide some soon.

With this, ASIC Chair Joseph Longo acknowledged what most who’ve worked on major deal risk-transfers know well – the available guidance on pre-hedging is written up in many places, none of which could be described as being definitive.

ASIC made good on their Chair’s hopes in February, squarely directing a new note: Guidance for market intermediaries on pre-hedging, at “market intermediaries,” with the Commission seeking to:

raise and harmonise minimum standards of conduct related to pre-hedging

improve transparency so that clients are better informed when making investment decisions

promote informed markets and a level playing field between market intermediaries, and

uphold integrity and investor confidence in Australian financial markets.

Adding a now familiar reminder:

Market intermediaries need to manage confidential client information very carefully and have robust, closely monitored and frequently tested arrangements for ensuring conflicts of interest are appropriately managed and in compliance with the Corporations Act 2001 (Corporations Act).

What we have noted is that a heavy set of obligations is now placed squarely on sell-side intermediaries in relation to pre-hedging. The default responsibility is for sell side firms to “minimise market impact”, and ensure they achieve “the best overall outcome for clients,” which we thoroughly unpacked in our recent work summarising the obligations – see here and here.

As we have noted, this latest guidance is consistent with global equivalents, providing intermediaries “with clear reference to the relevant Australian legislation and regulatory guidance.” But as we have also written before, there remains a gap in guidance with respect to guidance for buy-side.

Why guide the buy side?

While ASIC defines those bringing large deals to market as “clients” this is a simplification in any setting that includes exceptionally large risk transfers. When an entity brings a deal that is larger than the combined risk-limits of major bank dealing desks the notion of there being a client-party in any traditional sense becomes blurred. “Parties to a risk transfer” might be a better description, with one party seeking to lay off its risk problem to one or more others.

As we have seen, the conduct of the buy side can be exposed within court proceedings when exceptional deals turn to dispute, including in the most recent high-profile case.

Which suggests that minimum guidance for those who bring deals in which pre-hedging may feature is overdue.

This could include guidance aimed at:

Encouraging firms to establish an appropriate deal strategy prior to passing information-sensitive details to market intermediaries

Ensuring proper communications plans and controls are in place before large deals are brought to market –to make certain that execution-consistent comms are planned for, restricting sensitive information to a strict “need to know”, and avoiding information slippage

Removing the risk that Chinese walls inconsistent with their intended approach to deal execution, with partitions between corporate finance, credit, and operations teams, and the dealing teams who may be asked to manage market risks

Avoiding unveiling credit or collateral deal mechanics and related topics such as deal novation to relevant market risk dealers

Carefully controlling the number and type of firms that may be placed in contest for deals, while ensuring suitability-of-counterpart is considered

Reducing the chance that execution dry runs don’t transmit key information beyond that necessary to gauge price and/or ensure no market disruption can arise

Ensuring buy side parties consider time-of deal and time-to-clear liquidity considerations relative to the available depth of the market in question

Placing the onus on buy side parties to clearly and in written agreement specify pre-hedging assent if any, the manner, and type of approval required to permit pre-hedging deals and the recording of such dealings

Creating a genuine, level playing field through equal treatment of market intermediaries to be asked to quote

If provided, such guidance could be argued as raising and harmonising minimum standards of conduct for those who carry large positions they wish to disperse into the market. Such treatment would be consistent with the status of clients as dealing parties as specified within the Global FX Code and acknowledge conformity with International Organization of Securities Commissions (IOSCO), the European Markets Authority (ESMA), and the Financial Markets Standards Board (FMSB).

As the Global FX Code states, the code:

‘is expected to apply to all FX Market Participants that engage in the FX Markets, including sell-side and buy-side entities, non-bank liquidity providers, operators of FX E-Trading Platforms, and other entities providing brokerage, execution, and settlement services.’

With “clients” defined as:

‘a Market Participant requesting transactions and activity from, or via, other Market Participants…’

Market Intermediaries

The essence of our view is that market intermediaries now bear a disproportionate responsibility for conflict-free, non-disruptive risk transfers of large deals.

With the best intentions and fully complying with ASIC’s latest guidance, it’s entirely possible, even under the best conditions, that dealing outcomes convey an impression of having been the result of conflict or having disrupted a market, based on how the aggressor firm acts – what communication they convey and what style of execution conducted.

It’s little wonder that market intermediaries are now wary of large deals and have sought improved guidance. After all, if the existing pre-hedging guidance were clear, the ASIC Chair would not need to have acknowledged the widespread calls for it.

Placing clear and reasonable markers for those who bring large deals could ultimately help ASIC achieve its stated aim of promoting informed markets and a level playing field between market intermediaries.

The case for options – Part II…

We recently wrote of our surprise at a further deterioration in the relative take-up rates of option products across financial markets. Ultra-low options usage has been a feature of markets since the big bang, but do such low rates make any sense? We think it points to a likely lack of understanding of the when and why use-cases (plural) for options.

In this blog, we use a simple model to show why a blanket aversion to options use is not rational and can limit choices and potentially increase the costs of hedging.

The tired old use-case arguments

The first text we point to when we are asked how clients can gain a better understanding of financial options is Sheldon Natenberg's "Option Volatility & Pricing: Advanced Trading Strategies and Techniques." First published in 1994, this is a market classic containing the clearest explanation of pricing we’ve read. It adds to this with a comprehensive exploration of the trading domain and of a wide array of various trading strategies.

What’s unusual about Natenberg’s work is that it doesn’t delve into defining clear use cases for financial options, relative or otherwise. Though the use cases are implied throughout, there’s no depiction of the kind of market settings or circumstances in which using an option could hold advantages over, for example, outright forwards.

Given this, we list below some of the classic arguments for when options use is generally considered to hold advantages in comparison to alternates:

When a participant has elevated decision-making uncertainty about the future path of a financial market. For example, when there is an event such as a close election of high consequence or a piece of likely market-moving economic data. We have seen these types of environments before in the form of Brexit and the 2016 US Presidential Election.

When a participant anticipates a period of elevated market volatility that could make decision-making fraught. Most market participants will recall 2007-2009.

When a participant wants the certainty of a known cost versus the (theoretically) unlimited loss of a fixed hedge, for example in a situation where a contingent risk is confronted.

These are particularly relevant for managers who face performance benchmarks or are in a highly competitive trade-exposed industry. In these cases, the quality of decision making and application of the right product in the right environment takes on added importance since a performance light will eventually be shed on the quality of collected decisions.

A forgotten use case argument

But what of the state of the market itself? Should this be a factor?

At this point it is worth considering a hypothetical example of a historic state-of-the-market conundrum; one in which the use of options could be considered advantageous. While the example below is hypothetical, it will remind many market participants of actual events. This may or may not be a coincidence.

Consider the case of a heavily trade-exposed Australian importer with USD obligations in a highly competitive industry segment:

Dateline March 2001, the AUDUSD exchange rate is trading at 0.4975, having just broken below 0.5000 for the first time in history,

The company’s long-run viability is compromised if import invoices are met at an exchange rate below their breakeven hedge rate of 0.5000 for an extended period,

Having elected not to hedge (i.e., sell AUD forward) at levels above 0.5500 over prior months the company’s management calls a crisis meeting,

The company’s treasurer has prepared advice on whether the company:

Should hedge using a series of outright FX forwards to try to protect against a solvency problem.

Do nothing, thus taking a currency view.

Purchase a series of AUD Put options with amounts and expiries corresponding to those of the proposed outright forwards.

In such a difficult situation the existential risk to the firm is obvious but less obvious is the fact that the decision of management should also factor in a reasonable assessment of competitor behaviour given the market state. Have competitors hedged? Are they similarly exposed?

Here we have deliberately avoided pricing up forward rates and/or option strategies for this hypothetical. Why? Because they are unnecessary.

In such a situation the use case for an options solution becomes much greater than it might be if the AUDUSD were higher since use of outright forwards can lock the company into hedges at unfavourable levels (at breakeven) that simply defer a potential solvency problem.

By locking in forwards, the company cannot participate in the economic relief that might arise if the exchange rate were to recover (from all-time lows) – over the tenor of the forwards put into place. Others who make “better” decisions have a chance to participate in a market state recovery.

Hence, options are of clear relative attractiveness given this state-of-the-market.

For Australian exporters, a similar hypothetical example could easily be constructed for the extended period where AUDUSD sat above 1.1000 USD.

A test of this argument

What if we can test the state of the market argument in favour of options usage?

To do this we established a simple decision rule set-up for exporters and importers – and again we will use the AUDUSD exchange rate for our test. The arbitrary decision rules we will test using historic data run as follows:

Exporters always BUY Forward, except when AUDUSD is above +1 standard deviation “dear,” in which case they use an ATM Call option.

Importers always SELL Forward, except when AUDUSD is below -1 standard deviation “cheap,” in which case the use an ATM Put option.

The analysis presented here is based on averages that imply a daily process, which is of course quite unrealistic. Nonetheless, for both exporters and importers the average results are meaningful in the sense that on average they can expect to gain advantages of a similar dimension over time. The analysis holds whether they trade occasionally and on non-defined framework as far as timings are concerned.

The mean and standard deviation statistics are simply based on the complete historic AUDUSD dataset since 1990, not some arbitrarily picked moving average (from which we could be accused of playing around with stats to make things fit our argument).

Testing for 6-month AUD exposures on a serial basis (daily test), we compared the outcomes of serially using outright FX forwards versus the use of options when the market was unfavourably positioned above or below one standard deviation from long run mean. The options payoffs assumed hold-to-expiry conditions rather than a discretionary exploitation of, for example, periods of high volatility.

Our findings demonstrate that on average a forward-only strategy produced a rate of 0.78593. This becomes the benchmark against which our test “model” can be compared, and we found that the model improved all-in FX rates for both exporters and importers by the following amounts:

Exporter improvement from using the model +0.0011,

Importer improvement from using the model +0.0022,

Which is consistent with our intuitive feel for this simplest of hedging models.

Couldn’t these results be the result of dumb luck?

To ensure that the results are not simply the result of randomness, we decided to test the model across multiple tenors, with interesting results that are consistent with the original Black-Scholes paradigm (the advantage gets larger with tenor).

Testing for 3-month through to 6-month tenor horizons we found our model demonstrated the following economic advantages versus serial use of forwards:

Which tends to validate the state-of-market use case argument which we could summarise as:

It can be beneficial to consider options use versus locking in unfavorable forward rates when the market has moved materially against your interests.

Which implies hedgers should assess their product of choice in a proper framework (not simply copying this simplistic approach).

Put another way:

It could be considered irrational to use only one type of financial markets product in all market circumstances and states.

Is 11 beeps a big deal?

While the gains from this simple model appear small, this is again a question of relativities. A gain of 0.0011 for a firm that exports A$100,000 of goods or services amounts to U$110.00, but what if you were importing or exporting billions quarterly?

Our point is not about scale perse – it’s about appropriate strategy and having robust frameworks that can provide benefits, not least of which is the demonstration of best practice.

And if all firms employed such frameworks, with the associated controls and dealing delegations, we suspect the options category would be a more frequently favored category, more in balance with fixed hedges than is currently the case.

The case for options

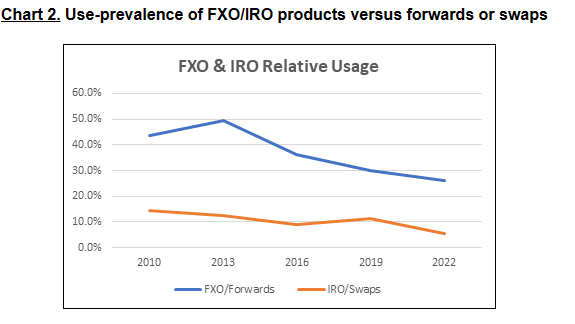

As long-term market participants and observers of product trends, we have been surprised by the low take-up rates of option products in evidence within the 2022 BIS Triennial data. The structural drift lower in option product usage rates doesn’t seem to make much sense.

In this blog, we take a look at the low usage rates, try to make sense of why options are being avoided, and explain why this may be irrational.

BIS data doesn’t lie

The BIS has been surveying financial markets since 1986. Its most recent triennial snapshot of the foreign exchange and OTC derivatives markets confirmed the steady relative trend away from the use of option products in financial markets.

Since the 2010 Triennial, the simple proportion of daily foreign exchange options (FXO) turnover within the FX category has fallen from an already low 5.2% of activity to 4.1% in 2022. The decline has been more pronounced for interest rate options (IRO), falling from an 8.9% usage rate to 4.6%. T

A more concerning picture becomes apparent when we consider the relative usage rates between competing hedge instruments.

Again, using the BIS data, the split of activity between FXO and Outright forwards confirms the high-level story. In FX, for every $100 use of an outright forward only $43.6 of FXO products were recorded at the 2010 Triennial, falling to only $26.2 by 2022. In interest rates, the relative IRO usage fell from $14.3 per $100 of swaps usage in 2010, to only $5.3 per $100 in 2022.

And the use-prevalence of options among counterparts who could be considered pure hedgers (labelled by the BIS as “non-financial customers”) mirrors these wider trends.

With very worrying trends for IRO prevalence in the IR-derivatives category. For every $100 of swaps only $3.20 of IRO products are traded among non-financials.

It is important to note that these are relative declines off an already-low activity base. Nominally, both FXO and IRO markets have grown; just not at the robust growth rates seen in the wider FX and/or IR derivatives markets.

To summarise: despite healthy nominal growth rates, use of option-based products continues to lag wider industry growth off a low starting base. More is being traded, a greater aggregate delta of risk is being taken or hedged, but the option-based share of this activity is in long-run decline.

In our view this suggests market participants either don’t understand the nature of the products or are systematically avoiding them. A viable product set that should be even-handedly evaluated in relation to their alternatives is being avoided.

Why the long-run decline?

We presented work on the topic of ‘premium aversion’ and ‘premium illusion’ in finance in 2022, see here and here. In these we postulated that:

Premium aversion is the desire or preference to avoid paying premiums, regardless of the assessed value of an option holding in a particular risk setting,

Premium illusion is a mistake of premium value-interpretation and comes in two forms:

the impression that premium expenses are almost certainly irrecoverable, or typically worthless; and

the impression that non-premium instruments (e.g., outright risk positions) are ‘free’ or contain no potential future premium in the form of opportunity, or actual loss.

In our view, both premium aversion and illusion are barely disputable as factors that serve to reduce the rate of options use.

Yet, aversion to paying premiums could be described as a constant factor, not one that should be weighing more heavily as financial markets grow – particularly given the high underlying volatility of the pandemic and post-pandemic markets.

Among other factors, we would highlight:

Concerns over the accounting treatment for options given the up-front premium expense of traditional option products,

Cash flow impacts stemming from option premium payments,

A general lack of confidence in assessing the nominal and/or relative value of options,

Widespread aversion to ‘sophisticated’ derivatives use.

Which means that the low take-up rate for option-based products is explicable and may arguably be rational.

Despite these, we question these ultra-low usage rates and posit that avoiding viable products in finance is irrational, likely self-defeating.

Is there a case for rethinking the use of options?

Our 2022 works demonstrated how premium aversion and premium illusion can serve to distort decision making in finance. The distortionary effects we pointed to tend to reduce option take-up rates, so we will leave that work stand.

Likewise, we leave others to consider whether administrative deterrents around cash flows and accounting treatments are sufficient to limit the options use case, though there are simple measures that can alleviate the cash-flow deterrent (premium in-arrears product variants).

Given this, the potential ‘for’ case in any rethink of options usage can be made on two grounds, one theoretical, the other more practical and economic.

The theoretical case for a rethink

Turning to economic theory, “indifference theory” has been a feature in economic works since the late 19th Century, typically in microeconomics studies of consumer preferences.

To leverage from the theory (without attempting to generate financial markets indifference curves), we should find general agreement with respect to the following statement:

“In the absence of other factors, if the economic outcomes (risk versus reward) of option-based product-use were known to be similar to that of alternatives (such as outright forwards or swaps), options use rates should reflect indifference and thus approximate an even share of activity across a sufficiently large and diverse customer base (such as that measured by the BIS Triennial Survey).“

To put this another way: if market participants were gaining advantages from the use of options to the same extent as from their alternatives, usage rates should be relatively even between the competing products.

So, what has been the historical pattern of the economic outcomes?

A comprehensive study of multiple asset classes and lookback tenors is beyond the scope of this blog. Nonetheless, in a study of strategy performance we should find that over sufficiently long timeframes, option premiums priced in competitive markets should tend to reflect the risks of the underlying asset. If, for example, they were consistently overpriced, few would ever hedge or speculate using options. If they were consistently underpriced, activity in forwards and swaps would be commensurately lower.

A relatively simple study of historic outcomes can demonstrate but not necessarily prove this.

Take the following study of hypothetical hedgers within the AUD/USD foreign exchange market:

AUD/USD Currency Hedgers

Serial six-month exposures,

Hedge products (strategies) deployed can be one of either:

Six-Month Outright Forward purchase or sale, or

Purchase of Six-Month Call or Put Options.

To determine comparative economic outcomes, we make several assumptions regarding ultimate pay-off conditions:

Where the outright forward is deployed the strategy ‘outcome’ is the average six-month forward rate over the study period.

For the option strategy we will assume that the pay-off rate is, market dependent, the average of the most favourable rate of either:

The option strike rate, plus or minus the premium paid, where the option expires in-the-money, or

Where spot traverses above/below the premium-break-even level favourable to the hedger prior to expiry (spot plus/minus option premium), allowing them sell or buy currency at spot and sell back the option for its remaining (residual) value, or

Some other rate between i and ii above (i.e., where the option is not exercised at expiry and the market did not hit favourable breakeven in the prior six months).

Assumption 2 will appear complicated and may seem restrictive in terms of assessing the value of the option strategy. However, our study cannot assign a value to the option buyer maintaining unlimited and unknowable freedom to leverage the option for profit. Our objective is not to determine a more profitable strategy per-se, but to accurately determine whether cost of option premium pays back the buyer within the bounds of pricing theory (i.e., consistent with the Black-Scholes paradigm).

We tested both strategies for hedge buyers and sellers using daily data running from 1st January 2002 to end September 2023 and found the following results:

The findings demonstrate a skew in outcomes, with buyer participants historically losing -40.7-basis point (BP) from use of (CALL) options instead of outright forwards and sellers gaining a +63.7 BP advantage from the use of (PUT) options.

Interestingly, the net benefit is a positive +23 BP buyer gain in favour of options usage. Though a wider study would be needed to provide more robust results, this suggests market participants shunning options use are missing potential value, particularly those on the importer side of the Australian financial markets.

This is a one-tenor, one currency, and one asset-class example that can hardly be labelled a ‘study’; however, it does point to there being reasonable inherent value in options product use and such use is worth fair consideration – not the obvious lack of interest as shown in the BIS study.

A potential practical factor

For those participants who remain uncollateralised as bank customers, options use may contain slightly lower initial transaction costs relative to forwards and swaps – i.e., at the point of deal execution.

Whereas payment of an initial option premium effectively collateralises an options trade, forward and swap products will typically need to be collateralised via the addition of an XVA charge.

The determinants of a final XVA charge range from credit (CVA) to funding (FVA) and capital costs (KVA). It is a topic that we may blog on in the coming year.

To summarise

As long-term market participants and observers of product trends, we have been surprised by the low take-up rates of option products that have validity. We are further surprised by the structural drift lower in option product usage rates in evidence within the BIS Triennial data.

If we consider the exceptional market volatility in interest rate markets since the demise of Global ZIRP (Zero Interest Rate Policy), we are particularly surprised by the low usage rate of IRO products.

Given the market disconnects between rational behaviour and the data, we intend to blog some more on this topic in 2023.

Pre-hedging - We know it’s a global issue…

At a recent ISDA/AFMA Forum, ASIC Chair Joseph Longo foreshadowed greater regulatory interest in the elusive subject of pre-hedging.

There can be little doubt that clear and consistent regulatory guidance on the topic would be well received, but this may actually be unrealistic.

In this blog I focus on why global clarity around pre-hedging has proven so difficult and share some thoughts on what regulators may be missing.

ASIC Chair

At the recent ISDA/AFMA Forum in Sydney, ASIC Chair Longo made the following comment in relation to pre-hedging:

We know it’s a global issue, so we’ve been engaging with ESMA on its call for evidence in Europe, as well as the FMSB and IOSCO, which is considering work in this area.

It is hard not to read this as an acknowledgment that the subject has multiple layers of complexity and that a globally consistent approach has, to date at least, proven elusive.

In separate news, Risk.Net reports that IOSCO is examining the question of “how dealers place hedges before executing trades,” and is expected to release its findings in Q3 2024. This is welcome, but some way off.

Pre-hedging?

So, what exactly is pre-hedging?

Here I submit standard industry and regulatory definitions, which are similarly framed but subtly different.

According to the European Securities and Market Authority, ESMA, pre-hedging is a practice in which a:

“…liquidity provider undertakes one or several transactions to hedge an order before it is received.”

The keyword being “before.”

While noting that pre-hedging is not defined under EU law, the authority concludes that:

“…pre-hedging is a voluntary market practice which entails a risk of conflicts of interest between the investment firm and the client/counterparty.”

The Financial Markets Standards Board, FMSB, has described the practice with a subtly different definition it its “Standard for the execution of Large Trades in FICC markets”:

“Pre-hedging is the management of the risk associated with one or more anticipated client trades. Pre-hedging is undertaken where a dealer legitimately expects to take on market risk in circumstances where such dealer does not have an irrevocable instruction from the client.”

The keyword here being “anticipated.”

The Global FX Committee, GFXC, provides a definition that describes pre-hedging in strictly legitimate terms:

“Pre‐hedging is the management of the risk associated with one or more anticipated Client orders, designed to benefit the Client in connection with such orders and any resulting transactions.”

While adding the highly important rider that:

“Pre‐hedging done with no intent to benefit the liquidity consumer, or market functioning, is not in line with the FX Global Code (Code) and may constitute illegal front‐running, depending on the laws of the relevant jurisdictions.”

These all provide useful individual points of guidance, but they cannot mitigate some fundamental problems that confront liquidity providers the moment information about a large or sensitive transaction first crosses an information barrier.

A number of very reasonable questions arise for liquidity providers (ESMA’s descriptor for sell-side firms) when a potential risk-transfer situation is first revealed:

Is there a clear, unambiguous, and enforceable pre-hedging agreement?

Can I trust the client (liquidity consumer)?

Who else is aware of the impending transaction?

What do these others know relative to my information?

Is my existing book at risk of loss given the potential transaction flows?

Could natural market factors move the market against the client if and when I execute pre-hedges?

Such questions could be thought of as the tip of an endless catalogue of questions in an endless range of potential dealing settings. Which may explain why a comprehensive and readily enforceable global standard has proven elusive.

Why so elusive?

It is not as if the conflict risk surounding pre-hedging is new.

The potential for large trades to convey sensitive market information is well understood and could be argued to be a problem as old as markets themselves. What is odd is that regulatory efforts to guide market participants with respect to dealing conduct are only relatively new.

Consider the following timeline:

2016 – FMSB, Reference Price Transactions standard for FICC markets,;

2017 – GFXC, FX Global Code;

2019 – ESMA, Market Abuse Regulation review;

2020 – FMSB, Standard for the execution of Large Trades in FICC markets;

2021 – GFXC, Commentary on the role of pre‐hedging; and

2024 – IOSCO’s pending pre-hedging investigation.

Which is all quite recent work, particularly considering that the US Insider Trading Sanctions Act was first enacted in 1984.

And these more recent efforts, though excellent initiatives, are tellingly somewhat different and come in the form of general industry codes or guidance. Which makes ASIC Chair Longo’s hint of possible ASIC engagement with ESMA, the FMSB, and IOSCO look all the more reasonable.

Some comments

Here I leverage the impressive work completed by the GFXC in 2017.

Firstly, it is clear from the GFXC FX Global Code that pre‐hedging conducted without the intent to “benefit the liquidity consumer, or market functioning” may “constitute illegal front‐running, depending on the laws of the relevant jurisdictions.”

“The intent of any pre‐hedging by the liquidity provider should always be to benefit the liquidity consumer and help facilitate the transaction.

Any pre‐hedging should be done in a manner so that it is not meant to disadvantage the client nor cause market disruption.”

What is unclear is how one proves “intent,” regardless of jurisdiction. As the GFXC concedes, intent “exists in the mind of a liquidity provider.”

Regardless of intent, what if circumstances arise that suggest pre-hedging contributed to an observable market move against the interests of the liquidity consumer? Or to an observable market disruption?

This problem of “intent” may therefore be intractable, a kind of wicked problem in financial markets and one bearing the unfortunate potential to mire relatively common market activities in protracted dispute.

Which suggests the existing jurisdictional mix of insider legislation, which leaves clear conduct risk hanging, may remain a kind of natural limit to governing pre-hedging in practice.

What about obligations for liquidity consumers?

One area that regulators appear to have paid little attention to is that of conduct obligations for liquidity consumers.

While it has made sense for regulator and industry attention to focus squarely on the actions and incentives of providers it seems odd that those who generate, carry, and/or convey potentially market-sensitive information have not been subject to much closer scrutiny.

It should be clear for those handling large transactions that when deal information is conveyed onto a dealing floor it can restrict the freedom of portfolio manoeuvre of the liquidity provider to an unknowable extent. Hence, generally agreed protocols for observance by liquidity consumers should be assembled with a view to restricting information slippage and miscommunication. These could be developed with industry input to limit the ways and extent to which misconduct on both sides of large deal settings may arise.

Here I pose some technical arrangements that regulators might consider, perhaps forming the basis for wider industry consultation(s):

Define a common and well understood threshold for deals that constitute “market sensitive transactions,” perhaps labelled MSTs. There are a range of possible approaches to defining such a threshold which would be related to market liquidity.

Define a suite of conduct obligations for those carrying market sensitive information related to deals above the MST threshold, not limited to:

o information security and communication protocols;

o formation and extent of information barriers;

o dealing panel formation and extent;

o request for indicative quote (RFI) protocols;

o RFQ protocols;

o pre-hedging communication and agreements; and

o clear markets and risk transfers.

Consider alignment of subsequent guidance with the well-received FMSB Reference Price Transactions (RPT’s) standard for the Fixed Income markets and their Standard for the execution of Large Trades in FICC markets. RPT’s may have particular advantages in removing conflicts and improving dealing price formation – for parties on either side of large deals.

This is a clearly non-exhaustive list, but I pose it as a possible starting point for the development of buy side protocols that might level the large deal playing field – and lead to more balanced outcomes for all parties.

Buy-side considerations

Whatever paths regulators eventually take, large deal strategy, frameworks and well-established dealing/execution protocols can be shown to meaningfully improve outcomes for those whom ESMA refers to as liquidity consumers.

Some important considerations:

No large transaction should ever be contemplated without a comprehensive transaction and associated deal communications strategy.

A deal situation-assessment should be used to inform and develop the transaction strategy.

Transaction strategy should include consideration of ultimate deal execution approach and path-to-execution, with proper assessment of:

o product suitability;

o hedge cost and risk assessment, including versus doing nothing; and

o counterparty evaluation and ranking – with reasonable consideration given to determining which party may provide the right home for the associated deal risk and/or product.

Communication strategy – crucial to minimising the risk of conflicts – should be more robust than the simplistic “needs to know” principle, covering:

o communication milestones;

o internal and external communication and controls;

o timing and establishment of robust information barriers;

o timing of RFI/RFQs and any deal rehearsals if appropriate; and

o panel bank composition and engagement timings.

It can be useful to imply a best-interests test to help inform and guide decision-makers, and to evidence best practice.

The unloved task of maintaining suitable records should be adopted.

Conclusions

With increasing regulatory attention, the observance of the approaches outlined here can help ensure firms exceed what we might term the implied industry obligations. Observance can be shown to reduce hedging costs and risks and reduce the chance that large deals result in disrupted markets.

For market participants of all types, global comprehensive standards for these sensitive market risk transfers really cannot come soon enough. In the absence of clear guidance great care in the approach to large dealings is warranted.

ESG maturing, far from settled…

We have been asked on several occasions whether we believe ESG-Investing has reached a state of reasonable maturity in capital and financial markets?

On each occasion I have proffered a rather hurried and wholly inadequate answer in the negative. In this blog I attempt to address this by cataloguing evidence of where greater maturity and/or standardisation is needed.

By way of reminder, Martialis takes no sides in the question of whether ESG investing adds value. If there is a value-assessment debate it is for others to determine, though we view the ultimate goals as laudable.

What follows should not be considered complete. While I have attempted to filter objectively, the starting point for the catalogue is inevitably opinion-based, or based on our experiences, and as usual – everything is contestable.

Some fundamentals

Let me start by making two general observations on the question of whether matters-ESG are ‘settled.’ This is a somewhat different question to whether they are, as yet, mature.

Firstly, modern investing owes much to the earliest open-air markets that started to evolve in and around the Warmoesstraat in Amsterdam in the late 15th Century. In their seven hundred-plus years evolution various approaches to investing have advanced and diversified, but never settled. Hence, at this relatively early stage, we should expect the ESG-investing domain to likewise advance and potentially diversify over time.

Secondly, while the world’s capital markets are truly enormous, it’s not clear whether there are sufficient ESG-rated securities to meet demand at any point. For example: if the world’s savings pool were directed entirely at ESG-rated assets above a certain score, their availability would be an obvious limitation. This is also food for thought for those who might be concerned at prospective concentration and/or asset hoarding risk (a topic for another day.

With this aside, I focus on reasonably objective areas that demonstrate that more mature ESG investing environment remains ahead of us.

The catalogue

John Feeney’s recent blog underscored the benefits of industry standardisation in benchmark setting, noting that:

“Markets depend on a level of benchmark standardisation that makes each dealer and end-user confident of the performance and valuation of each product.”

And:

“Most deep and liquid markets depend on a standard benchmark for risk resetting which is widely available and used in the majority of traded products.”

While John was pointing to the benefits across traded products, I think it is reasonable to extend these contentions to global finance more generally.

What we know is that in domains such as, say, transport, standardisation that turned cargo freight into uniform cargo in the form of ISO-standardised containers and pallets has driven incredible efficiencies. We can also agree that in financial markets high degrees of homogeneity have dramatically improved the efficient movement of capital between economic agents.

Thus, the catalogue that follows leans heavily on our enterprise view of the attractiveness, benefits, and likely efficiency-gains of adopting highly standardised and transparent approaches in markets:

ESG Ratings

Whereas the credit rating domain settled around a group of core agencies with well-understood approaches and ratings actions, the ESG ratings space continues to evolve.

As John noted, ESG evaluation criteria vary between multiple different rating platforms and are typically not independently verified, thus there is “no existing robust and standardised measure of ESG which captures a wide range of inputs and could be classified as a financial benchmark.”

Separately, it’s reasonably clear that ESG ratings are themselves an emerging specialisation, evidenced most recently in the unfortunately high ratings achieved by FTX on governance measures by a prominent ESG ratings firm.

Investment managers should note that ratings and ratings standards are neither fixed, nor a one-way bet.

2. Pricing (particularly sustainability premium or ‘greenium’)

We would normally view pricing as the rather obvious interaction between buyers and sellers known as price discovery in transparent markets, but this is a feature of mature markets. In less mature settings the pricing of individual deals may be shrouded by ‘tailored estimation’ (in the absence of an observable markets), and price discovery may be problematic given the one-sided nature of demand.

And this appears to be the case with ESG deal price-setting.

We note that in a recent ISDA survey, The Way Forward for Sustainability-linked Derivatives, the association asked members how ESG premiums are determined. Of 69 survey respondents a clear majority (45) indicated they “did not know how these premiums are determined.” ISDA also referred to the SLD market (sustainability linked derivatives market) as being “nascent” and described the sustainability premium or “greenium” as a “new concept in derivatives trading.”

These are obvious features of illiquid or partially formed markets such as those found in the price of highly complex derivatives.

3. Primacy

Corporate finance valuations have generally advanced down return or risk-compensated return dominant pathways. This was the logical advance of finance theory driven by advances in thinking around CAPM models and the like, aided by return-based concepts such as RoIC, RoCE, and RoE and broader economy concepts such as those found in the macroeconomics field.

While the layering of ESG filters within investment processes can take many forms, the question of ESG primacy arises. At what point should ESG filters be applied? Is there a fixed line, or some flexibility? What of exceptions? Should ESG factors take precedence, before traditional valuation approaches are applied?

We note that there are a variety of approaches being taken among clients, and other investment entities with whom we are close. Few are attempting a strict Blackrock ETF-like approach, though all have found themselves under pressure to respond in some fashion.

4. Portfolio Construction

Portfolio construction and asset allocations are considered by many to be at the heart of investment management performance.

Linked to the question of ESG-primacy is the question of whether a filtering process (particularly very strict approaches) may have unintended consequences in terms of optimal portfolio construction?

This is an emerging yet important topic. Is a traditionally risk-efficient portfolio, one suited to one or more beneficiaries under traditional allocation approaches, corrupted when ESG filters are applied (particularly if stringent filters remove whole sectors from consideration)?

There are a range of views on this, and I do not propose to dig into them here, however, we note that ESG scores for certain investable sectors are more readily achieved than in some others. At a minimum, we would expect this to have a bearing on portfolio concentration (and this may have played-out across the sweeping return-themes of 2022, in the dramatically skewed returns to energy sectors compared with new-economy stocks).

5. Emerging Standards

Perhaps the greatest area driving ESG towards maturity at present is that of the impending transparency, particularly in the sustainable finance edge of ESG. We see this as being driven by a range of government and regulatory agents.

There are simply too many global initiatives in-train to mention at present, but by way of example:

Australia - National Sustainable Finance Strategy,

We view these as likely to shape and enhance ESG maturity by bringing a degree of standardisation, but this will take time.

In this sense such initiatives are to be welcomed, but they are not yet embedded or systematically applied. They are also occurring on a multi-jurisdictional basis, and though we can acknowledge the work of the UN, there appears to be only vague international coordination.

We urge investment managers to watch these developments closely, since differing or changing standards can have a bearing on portfolio composition considerations.

6. Fiduciary Risk

We covered this topic in my blog of November 9th; ESG & Mandate Risk, which received reasonable interest and viewership. Judging by the number of follow-up engagements on the topic we expect the fiduciary question to linger.

Opinions certainly vary among readers as to whether fiduciary risk rises or falls away, but this itself is a sign that the question of fiduciary responsibility is not entirely settled. It may also be prone to shifting political sands on a jurisdictional basis (down to state level in the US as one example).

More recently, we have seen additional thought pieces on this topic appear, for example, Does ESG investing have a problem with fiduciary duty?, and related news that demonstrates there is a distance to travel before maturity is reached:

We continue to assess the various risks within this space.

Summing up

To sum up, we have been taking stock of the ESG domain for considerable time and have had several interesting client engagements on the topic. Much of what I have expressed here has been driven by such engagements, which have been highly productive and somewhat illuminating.

Our role is always to consider what is happening and be in a position to help inform decision-makers as their navigational needs arise, and as they ask where they should be positioned as events unfold To this end, it is helpful to be challenged on any topic, but on the question of how mature the ESG domain is for investment managers this has been very much the case, and we expect the challenges to continue.

While we are inclined to point out that there is a potentially long way to go, we can at least note that ESG investing is maturing but not yet settled.

As always in finance, some complexity remains, and market participants will have to keep adjusting.

Trading ESG Risk

Deep and liquid traded markets

Many financial risks can be acquired or modified through trading of securities and/or derivatives. For example, derivative products related to interest rates have been traded for many years and has seen the considerable growth of markets to shift risk from firm to firm. An active market to trade the risk has enhanced the ability of investors and borrowers to settle on the type and amount of risk best suited to their needs.

Another example is equity risk which also have deep and tradable markets. In this case, derivatives often reference an index such as Dow, S&P500 and NASDAQ which allow participants to trade the general direction of the market or alternatively trade sectors or even individual names. In each case, the underlying floating rate or index is clear and readily referenced to benchmark the trade.

Markets depend on a level of benchmark standardisation that makes each dealer and end-user confident of the performance and valuation of each product. Even the much-maligned LIBOR played a pivotal part in the development of traded interest rate markets. Without a standardised measure for risk setting such as LIBOR, derivative markets, for example, would have been impossible to trade in such a simple and definable way. And as LIBOR was replaced by Risk Free Rates such as SOFR and SONIA, the traded markets have adapted and continued to grow.

Likewise, equity markets have developed effective benchmarks for pricing in markets and allow for efficient risk transfer.

Most deep and liquid markets depend on a standard benchmark for risk resetting which is widely available and used in the majority of traded products.

The ESG markets – the next frontier

The ESG markets do not, at present, have the ability to trade the ESG risk in an equivalent way to interest rate or equity risk. There is no inter-dealer ESG derivative market and no standardised rate or benchmark to reference in a similar way to interest rates or equities.

A few firms do produce ‘ESG Scores’ which are not, technically, benchmarks. These include:

rating agencies such as S&P, Moody’s and Fitch;

Data providers such as Bloomberg and Refinitiv; and

Others such as ISS, MSCI, Datalytics etc.

While these agencies and vendors produce a ‘score’ from publicly available data (such as annual reports from companies) they are quite clear that these are not independently verified. In this sense, they are not benchmarks and could not be used under the regulatory requirements of many jurisdictions for the purposes of a benchmark, I.e., typically defined as refixing a variable rate or valuing a security.

So, there is no existing robust and standardised measure of ESG which captures a wide range of inputs and could be classified as a financial benchmark.

Why does the lack of a benchmark matter

If you have a risk or a desire to trade a financial product, you usually look at a screen where the bids and offers are posted for the products in which you have an interest. The products have standards and definitions which are supported by contracts and documentation such as that provided by ISDA for derivatives.

Whether it is a swap for fixed against floating or a fixed rate security, there is a need for an index or benchmark to provide the floating side of the trade and/or the valuation of a security. This is at the very heart of ‘price discovery;’ itself an important efficiency-driver.

It is particularly useful to use a standardised benchmark for obvious reasons. Once the benchmark is defined and readily available then there is a consequent reduction in the complexity of the trading because everyone is referencing the same rate or index.

Without a standardised benchmark, ESG products are difficult (I.e., near impossible) to trade in the inter-dealer market which means everyone simply builds up risk with no effective way to trade this into a market where the other side may be found.

One-sided or two-sided markets if an ESG benchmark can be developed

There is a market view that any ESG market would only be a one-sided (i.e., everyone wants to receive ‘fixed’ and pay ‘floating’ ESG). It is likely the result of the rush into ESG exposure and the perceived lack of floating rate investments that seems to drive this argument.

However, I take a slightly different view. Let’s take the example of a company with a debt linked to ESG performance. These have been transacted where the margins on the fixed or floating debt reduces as ESG performance improves (however that is measured!).

In this case, if the company had assets with fixed returns, then they may be a natural fixed rate payer of the derivative to match the asset risk to the liability risk. So why have ESG linked debt? Well, investor demand may be such that ESG debt represents cheaper funding, but it needs to be swapped for better risk management.

The investor argument is also important. Not every fund is ESG focussed, and some investors may actually need additional non-ESG exposure if they can only acquire assets with ESG links in the names they need for diversification.

I am a believer in traded market efficiency. If there is a market which is clear and standardised, a basis may form but equally the arbitrageurs will move in if that basis is unfounded. Price discovery is fundamental to their work.

Summary

The ESG market is growing and evolving as borrowers and investors respond to changes in demand. The current products are generally customised and structured for individual needs and are therefore not easily tradeable.

For deep and liquid markets to develop, there will need to be considerable development of standards and documentation for products (see ISDA survey) and credible benchmarks to support the products. While there are some ‘scores’ available there are no robust benchmarks to apply to products.

Along with the products for borrowers and investors, a supporting derivative market is essential to allow firms an efficient way to move and diversify the risk. A derivatives market needs a benchmark, and this is one of the major components of the market yet to develop.

ESG & Mandate Risk

Recent events in various US jurisdictions have highlighted an important set of questions around ESG investing. We believe these need to be considered by those holding a position of trust in the management of investor funds. Specifically, questions have been raised publicly about the nature and form of mandates governing the actions of funds.

In this blog we take no sides in the question of whether ESG investing adds value. Instead, we take a closer look at questions related to investment mandates under ESG and find that it may be worth those with fiduciary responsibilities taking their mandate into full and frank account.

Recent Challenges

Environmental, Social and Governance – ESG - investment platforms made unexpected headlines in the United States through Q3.

This included certain reports.

19 US state attorneys general wrote to BlackRock, arguing that the investment manager’s ESG investment policies may violate the ‘sole interest’ rule, which in the US requires that conflicts of interest in fiduciary relationships be avoided.

Attorneys General in Indiana and Louisiana issued warnings to their respective state pension boards that ESG investing may be a violation of their fiduciary duty.

West Virginia barred Blackrock, JPMorgan, Goldman Sachs, Morgan Stanley and Wells Fargo from contracting for new business in the state after determining that through ESG policies they were boycotting the fossil fuel industry.

Texas identified 10 companies, and 348 investment funds whom legislators labelled ‘boycott energy companies’, including BlackRock, Credit Suisse and UBS, prohibiting them from contracting with state agencies and local governments.

Our attention was drawn to this by a recent Wall Street Journal piece which noted that the principles invoked in the letters sent to Blackrock are “part of the common and statutory laws of almost every state.”

While it may be tempting to dismiss the Journal’s authors as partisans assembling contestable assertions, see here and here, we leave the tactical debate to others, for example:

Harvard Business Review:

o Yes, Investing in ESG Pays Off; versus

o An Inconvenient Truth About ESG Investing,

What we find interesting is that:

The various state-based challenges reignite a debate around fiduciary responsibilities that emerged when Corporate Social Responsibility, started to emerge in the early 2000’s; and, more importantly

ESG investment may be argued to contravene the Uniform Prudent Investor Act, adopted by 44 US states and the District of Columbia, which states:

No form of so-called "social investing" is consistent with the duty of loyalty if the investment activity entails sacrificing the interests of trust beneficiaries – for example, by accepting below-market returns -- in favor of the interests of the persons supposedly benefitted by pursuing the particular social cause.

The Journal’s writers, William Barr and Jed Rubenfeld, go on to note that “a defence to ESG investing asserts that ESG factors, though nonpecuniary, are material to profitability and that ESG investing will therefore produce superior outcomes.”

This appears contestable, as the varying Harvard studies amply prove, but when canvassing for views from among Martialis clients and contacts one message stood out: most managers have been inundated with requests for ESG-overlay and careful observance, not the opposite.

Fiduciary Duty in Australia

We hope to follow up on this blog with a more detailed look at the nature of fiduciary responsibilities in an Australian context. The aim will be to get a much clearer definitional picture from experts, so watch for that in coming issues.

What we do note is that there appear to be similar provisions within the Corporations Act to those written-in to the US’s Uniform Prudent Investor act. For example, a responsibility under the Australian Act is that responsible entities (of registered schemes) duties include acting “in the best interests of the members and, if there is a conflict between the members' interests and its own interests, [to] give priority to the members' interests."

Perhaps the risk for fund directors lies in the definition of what constitutes a member's interests? Is it to maximise returns with an ESG filter or overlay, or simply to maximise returns?

In our view, risk here can likely be distilled into to a fundamental question of fund mandate.

Where a fund has ensured beneficiaries are aware of the nature of the decisions being made – whether ESG-based or otherwise – a mandate sets the parameters within which a portfolio is managed, thus setting properly informed beneficiary expectations.

But what of funds that have started overlaying ESG filters without addressing beneficiaries or their mandate?

To us, this seems problematic.

A problematic greenium

As the market transparency of ESG investing modes develops it will be increasingly easy for fund beneficiaries to assess the decision-making path of fund managers.

To reinforce this, we note that Bloomberg has embarked on an extensive ESG program designed collect some data to the ESG metrics.

Bloomberg’s Environmental, Social & Governance (ESG Data) dataset offers ESG metrics and ESG disclosure scores for more than 14,000 companies in 100+ countries. The product includes as-reported data and derived ratios as well as sector and country-specific data points. In addition to the extensive ongoing data coverage, we provide historical data going back to 2006.

This allows Bloomberg subscribers to gain access quite remarkable decision-making tools and transparency.

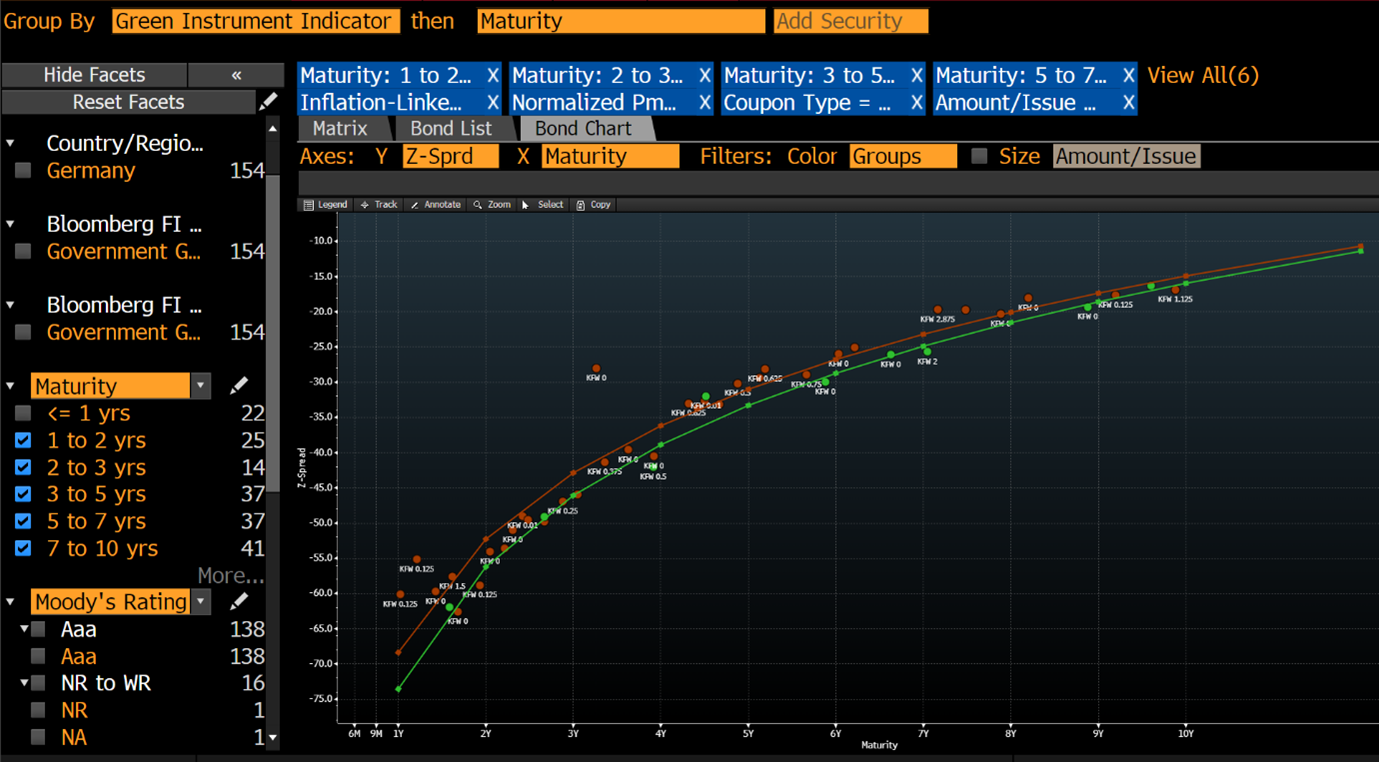

For example, here is a screenshot of Bloomberg’s Green Instrument Indicator:

Which means that transparency is assured.

What then of a situation in which, for example, a bond fund manager is considering a purchase of bonds/bunds of, say, a noted green issuer - the Federal Republic of Germany?

The German state issues both green and non-green bonds, and has gone to impressive lengths to distinguish between the two:

The use of proceeds from Green German Federal Securities always corresponds to federal expenditure from the previous year. Spending from the previous year’s budget that qualifies as “green” is assigned to the securities. The Green Bond Framework lists five main green expenditure categories that can be assigned to Green German Federal Securities.

These are:

Transport

International cooperation

Research, innovation and awareness raising

Energy and industry

Agriculture, forestry natural landscapes and biodiversity

Noting that the yield differential between a 10-year green and traditional bund is around 5.0 basis points, it’s not hard to see a potential fiduciary risk problem emerging.

If our bond fund manager notes the differing market yield representing the ‘greenium’ (which we imply as resulting in a lower monetary yielding outcome for the investor) and has no mandate for such a product we suggest there is a potential problem.

Why?

Because a beneficiary who considers their best interests to be served by owning higher yielding paper – irrespective of their views of ESG outcomes - could make the argument that the manager was in breach of their fiduciary duty. Transparency makes their argument much easier.

Which brings us back to the question of fund mandates, and several important questions:

· Is the fund mandate current?

· If mandate changes that were likely to diminish fund returns have been implemented, were beneficiaries advised of these changes?

Those holding fiduciary responsibilities should take their mandate into full and frank account, or at least ask two questions:

1. Is our mandate current?

2. Is our mandate clear?

Summary

ESG investing is very topical among investors. However, the investment mandates are important documents which need to be observed. In addition, regulators and legislators are now taking interest in the investments and often taking action to protect their industries.

We will be writing more on this in the near future.

That’s not a framework…

At Martialis, we routinely advise in situations where an absence or the presence of adequate frameworks has led to problems that client firms might otherwise have avoided; which explains our somewhat obsessional interest in promoting frameworks.

Obsessions aside, we do not suggest every minor firm issue needs a framework -far from it. But those that feature prominently in firm outcomes, particularly where issues may undermine the outcomes for firm shareholders, should be considered (if nothing else).

In this blog I venture into listing the attributes of what we believe constitute healthy frameworks, sharing the collected Martialis house view. It’s not the work of academia or a collection of on-line material, rather it is our experience of how solid framework brings positive results.

I start with an example of a framework which has stood the test of time.

An example of solid frameworks - Ray Dalio

Connecticut based, Bridgewater Associates is one of the world’s largest and most successful hedge fund managers. With circa U$150 billion under management, in certain size categories it would be considered the world’s largest, just as in certain return-series the firm’s returns have been simply Buffet-like, astounding.

Founded in a Manhattan apartment in 1975, Bridgewater has been a success at almost everything it has touched; from consulting, to research, and through to money management (particularly), and many readers will associate the firm with its founder and inspirational leader, Ray Dalio.

Aside from the many successes of Bridgewater, one of the things that singles the firm out as unique is Dalio’s preparedness to spread his view of how to build a great business (or great anything really).

He does this by promoting access to the firms Principles: Life and Work, which has been variously turned into:

Having read the earliest versions of Dalio’s work (in its initial e-book stage), like so many of my peers in financial markets I wanted to get a feel for how the Bridgewater founder thought; what was his firm’s recipe for success? At a mind-numbing list of actual principles (I haven’t counted them, but the condensed version lists 157), I love so many aspects of the list, but I’m not sure they can easily be lived by, and Dalio himself doesn’t suggest one actually try.

In making a point about Ray Dalio in a work exploring the importance of frameworks, readers should note that Principles mentions ‘framework(s)’ literally only three times. This might present as strange, but the reason for this is simple: Ray Dalio actually considers his work a framework in its own right, noting eventually (see page 315) that Principles is: “a framework you can modify to suit your needs (Principles: Life and Work, Ray Dalio, Simon & Schuster, New York, Page 315).

Which is my point.

Bridgewater’s success is well known to be the result of the firm’s leadership embracing Dalio’s Principles as their overarching framework. A framework that guides how people operate within the firm, not necessarily as we might infer, some codified system of rules and/or controls that manage specific matters.

The key is that Bridgewater has an amazing high-level framework that guides staff when they make decisions; witness the quite staggering compound benefits.

Principles or Frameworks?

One could easily argue all day about what constitutes a principle and what constitutes a framework. The two concepts are obviously related, though subtly different, but we believe they play important and somewhat different roles at different points in the hierarchy of firm management and control.

And the difference, subtle or otherwise, should not be dismissed.

Taking the Oxford Dictionary definitions in turn:

Principle: a moral rule or a strong belief that influences your actions

Framework: a set of beliefs, ideas or rules that is used as the basis for making judgements, decisions, etc.

Perhaps the best way to explain the difference is by resorting to the example of the founding of the United States as an independent nation.

The framers of the US constitution settled on a set of five guiding principles for the system of government they wanted to establish; which included: federalism, limited government, popular sovereignty, republicanism, with checks and balances.

These were enshrined throughout the Constitution that was eventually crafted, and it – The Constitution for the United States - became the crucial written framework for how the US form of government would work.

At Martialis, we believe that in a firm-management context it is this latter distinct and crucial difference between principles and frameworks that matters when it comes to how best to order firm workings:

Principles provide high-level guidance with respect firm directions and values

Frameworks establish rules-based structures in particular areas, circumstances, and where enterprise risks are present

Which brings us to the question of what constitutes a healthy framework?

Principles of Healthy Frameworks

In formulating the following, we naturally lean towards our experience within financial markets. However, we believe in most cases these could be applied to firms in almost any industry setting.

There are seven Martialis principles for healthy frameworks, in what is still for us a work in progress:

Principle 1 - Tailored for Task

Individual frameworks should be tailored for the specific circumstance, task, objective, or risk the firm wishes to manage or control; no more, no less.

The degree of tailoring is theoretically limitless, but we believe should be calibrated based on relevant elements such as:

Degree of subject-matter complexity

Degree of prescriptiveness desired

Formality, for example: guidance versus policy

In financial-market risk, macro-economic factors and correlations should also be considered and/or formally assessed when tailoring.

In assisting clients in a range of subject-matter, we are often tasked with cross-reference reviews into firm frameworks. In this we often note that elements of quite workable frameworks sit in disparate fragments, while others can be beautifully crafted and perfectly concise, while sitting hidden in tome-like volumes. We therefore recommend that any individual framework be tailored in ways that avoid fragmentation or the risk of the work becoming submerged (out of sight, out of mind).

Principle 2 - Designed to avoid reactive decision-making

Reactive decision-making can be argued to invite randomness into firm outcomes, particularly in financial-market risk settings. Ensuring a framework minimises reactive decision-making is crucial.

It’s important to note that for Martialis, we believe this should apply on both sides of firm outcomes, avoiding reactivity across different states, such as:

When markets deliver unfavourable conditions,

When market conditions are favourable,

When market conditions are stable/unremarkable

I note that very few of the frameworks we have encountered have any definition of what might be done when market conditions present opportunities.

In my most recent blog I recounted the story of a firm that had a ‘do-nothing’ framework based on a buffer-rate, while maintaining a significant (actually existential) firm sensitivity to an exchange rate. This unfortunately ensured that when currency market conditions favourable to the setting of longer-term risk hedges were reached the firm continued to do nothing.

In our view firms who seek to manage outcomes need to be mindful of the practical impact of the framework at both ends of the risk continuum, not simply on one side. In favourable circumstances rainy-day hedges can prove highly beneficial. Frameworks should encourage latitude to manage the upside as well as the downside.

Principle 3 - Accountabilities should be clearly defined

Where decision-making accountabilities are involved unambiguous accountabilities as to delegated authority are vital, and ideally formally maintained. This includes decision-making forums, particularly where a quorum is needed before time-sensitive decision making is prevalent.

Who is delegated to make a decision?

Who can make the decision in the event they cannot?

To whom is the decision-maker responsible, and to whom can a decision be escalated?

On what basis can they make their decision? E.g., do they require formal advice?

What is the boundary on the extent of their decision-making delegation?

What decision-making artefacts should be preserved once a decision is taken?

We mentioned in Principle 2, that reactive decision-making invites randomness into firm outcomes. This is often due to the fact that key decisions are often forced upon firms in time-sensitive settings, particularly where financial market risk is concerned. It is also the case that risk-reward asymmetry can play a role (a topic for a future blog, but losses are psychologically different to gains). Healthy frameworks are those devised to minimise decision-making ambiguity in all its guises’.

Put another way: ambiguity invites eventual disaster.

Principle 4 - Thresholds should be thoughtfully calibrated and consequential

Where circumstances demand the imposition of framework thresholds, for example in areas of stopping risk or losses, it’s important that the thresholds themselves be:

Carefully considered (and maintained on an ongoing basis where appropriate)

Respected

Monitored

Policed if necessary

This remains the case regardless of the decision-making latitude afforded to key staff.

Our firm has deep experience in managing teams in various financial markets settings, including settings which afforded key-staff quite generous decision-making latitude. It’s important to note that in these settings robust frameworks were not devised to prevent active management of financial risk, but quite the opposite.

Well thought out thresholds, for example: well thought-out loss tolerances, can promote good decision-making, but only if thresholds set and agreed are meaningfully policed.

Principle 5 - A framework should be formally recorded

Lack of formal recording of frameworks, particularly risk-bearing elements such as delegations and authorities can be as dangerous as the absence of a proper framework. We recommend a reasonable degree of formality be associated with the task, and proper recording is not difficult once a framework has been tailored and agreed upon.

Proper recording has many associated benefits, not limited to:

·Minimising confusion and downstream dispute

Ensuring stakeholder awareness

Facilitating appropriate 2nd/3rd line ex-post review

As a record of decisions-taken,

As mentioned in my last blog, the absence of formal record keeping of firm policies can present as a weakness of governance where firms are targeted in acquisitions.

Here I will simply remind readers of our standard refrain: If it’s not written down, it doesn’t exist.

Principle 6 - Good frameworks are memorable, and readily accessible

Overly complex frameworks and/or frameworks that are inaccessible in normal conditions to reasonably well-informed staff should be avoided.

In Martialis experience, illogical or overly complex frameworks can be self-defeating and open firms to dispute and/or policy non-adherence. Where framework records are poorly kept or buried within excessively large policy manuals similar problems can arise.

Logical, internally consistent, and easily understood policies that can be retrieved from internal firm libraries should be thought of as good practice that promotes framework effectiveness.

It was the highly regarded Austrian-American management consultant and educator, the late Peter Drucker, who coined the phrase: “what gets measured gets managed.” We’re not as certain of Drucker’s claim in the age of big data, but we do agree with the thrust and suggest firms consider what happens when things that can and should be managed are poorly managed.

Our experience suggests that if staff can’t give a reasonable elevator pitch about a particular topic, they either don’t understand it, or they aren’t aware of it. The same is true of frameworks. Well calibrated frameworks with appropriate thresholds that are readily retained by key staff are more likely to be deployed when circumstances demand they be deployed; not left open to the vagaries of chance or random outcomes.

Principle 7 - Good frameworks are memorable, and readily accessible

We believe frameworks should be subject to ongoing review, particularly in situations where market circumstances can change rapidly. Markets and economies are constantly evolving, hence frameworks judiciously formed in one setting can be found wanting, or even inappropriate.

This does not mean that the tempo of review has to be disruptive, nor onerous, but a degree of regularity can be expected to pay dividends.

We note that firms that review policies and procedures keep their frameworks current, and the simple process of review can lead to improvements not recognised at framework inception.

There are few elements of business that couldn’t benefit from a commitment to ongoing review. For firms in financial markets the post-GFC regulatory environment has turbo-charged the extent of necessary policy and compliance standards that firm policy-libraries are now basically overflowing.

But this is not likely to change; which means adaptation is key.

We believe that firms who accept the realities of ongoing review and adapt to the environment stand a better chance of negotiating future risks, and of maintaining the operational poise to gain from future opportunities.

Thus, well laid policies and protocols, modern and judiciously maintained, have an intrinsic value far beyond the costs of production and ongoing maintenance, and a regular tempo of review only adds to that value.

A tedious topic?

The topic is tedious, certainly; but should it be ignored?

We intend to write more on frameworks in coming blogs, which is something of a measure of how much emphasis we believe firms should place on their proper formation: making them and keeping them fit-for-purpose.

In the context of the risk-bounty found in financial markets, I will leave you with a simple quote from Ray Dalio, explaining his personal success in his 2019 CBS 60-Minutes expose.

Ray Dalio: “It’s 100% in those principles, in other words, principles are like, um, when you’re in a situation, what choices should you make? “

Why Robust Frameworks Matter…

At Martialis, we have a simple standard refrain: if it’s not written down it doesn’t exist.

In my mid-December blog I introduced the topic of decision-making frameworks and why they can be used to promote outcomes of higher quality in a range of fields exposed to uncertainty. I extended this into the area of hedging market risk, since financial markets are a field shrouded in uncertainty.

In today’s blog I am going to expand on this theme by presenting a catalogue of reasons why firms should carefully consider robust frameworks for managing market risk.

Charles had a framework

Working in financial markets in Melbourne in the early-1990’s I’d occasionally take a call from my entrepreneurially gifted friend Charles (a great friend to this day, but not his real name).

Since I worked in a major dealing room, Charles was always interested in what I thought of the Australian dollar exchange rate. It didn’t matter that I’d moved across from an utterly failed stint as a currency trader (FX-options) to an equally questionable time running a bond-option/swaption book, Charles wanted to know what I thought ‘Aussie’ might do (markets love their pet names); where was Aussie headed?

Charles business imported a unique brand of high-end outdoor gear and consequently had a particularly acute sensitivity to the value of the AUD/USD rate. His suppliers demanded monthly payments in USD while his sales were uniformly made in AUD, as is common among Australian businesses. Charles was “long-AUD,” in market parlance; if the Aussie fell his average cost of sales would balloon and his business would suffer accordingly.