The case for options

As long-term market participants and observers of product trends, we have been surprised by the low take-up rates of option products in evidence within the 2022 BIS Triennial data. The structural drift lower in option product usage rates doesn’t seem to make much sense.

In this blog, we take a look at the low usage rates, try to make sense of why options are being avoided, and explain why this may be irrational.

BIS data doesn’t lie

The BIS has been surveying financial markets since 1986. Its most recent triennial snapshot of the foreign exchange and OTC derivatives markets confirmed the steady relative trend away from the use of option products in financial markets.

Since the 2010 Triennial, the simple proportion of daily foreign exchange options (FXO) turnover within the FX category has fallen from an already low 5.2% of activity to 4.1% in 2022. The decline has been more pronounced for interest rate options (IRO), falling from an 8.9% usage rate to 4.6%. T

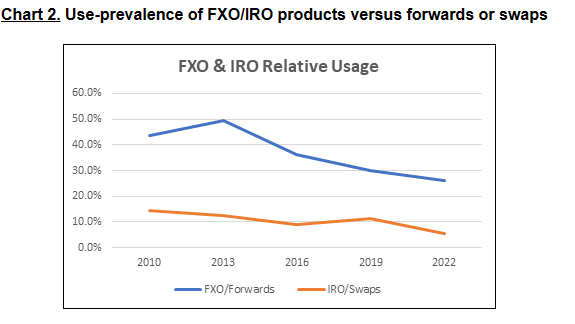

A more concerning picture becomes apparent when we consider the relative usage rates between competing hedge instruments.

Again, using the BIS data, the split of activity between FXO and Outright forwards confirms the high-level story. In FX, for every $100 use of an outright forward only $43.6 of FXO products were recorded at the 2010 Triennial, falling to only $26.2 by 2022. In interest rates, the relative IRO usage fell from $14.3 per $100 of swaps usage in 2010, to only $5.3 per $100 in 2022.

And the use-prevalence of options among counterparts who could be considered pure hedgers (labelled by the BIS as “non-financial customers”) mirrors these wider trends.

With very worrying trends for IRO prevalence in the IR-derivatives category. For every $100 of swaps only $3.20 of IRO products are traded among non-financials.

It is important to note that these are relative declines off an already-low activity base. Nominally, both FXO and IRO markets have grown; just not at the robust growth rates seen in the wider FX and/or IR derivatives markets.

To summarise: despite healthy nominal growth rates, use of option-based products continues to lag wider industry growth off a low starting base. More is being traded, a greater aggregate delta of risk is being taken or hedged, but the option-based share of this activity is in long-run decline.

In our view this suggests market participants either don’t understand the nature of the products or are systematically avoiding them. A viable product set that should be even-handedly evaluated in relation to their alternatives is being avoided.

Why the long-run decline?

We presented work on the topic of ‘premium aversion’ and ‘premium illusion’ in finance in 2022, see here and here. In these we postulated that:

Premium aversion is the desire or preference to avoid paying premiums, regardless of the assessed value of an option holding in a particular risk setting,

Premium illusion is a mistake of premium value-interpretation and comes in two forms:

the impression that premium expenses are almost certainly irrecoverable, or typically worthless; and

the impression that non-premium instruments (e.g., outright risk positions) are ‘free’ or contain no potential future premium in the form of opportunity, or actual loss.

In our view, both premium aversion and illusion are barely disputable as factors that serve to reduce the rate of options use.

Yet, aversion to paying premiums could be described as a constant factor, not one that should be weighing more heavily as financial markets grow – particularly given the high underlying volatility of the pandemic and post-pandemic markets.

Among other factors, we would highlight:

Concerns over the accounting treatment for options given the up-front premium expense of traditional option products,

Cash flow impacts stemming from option premium payments,

A general lack of confidence in assessing the nominal and/or relative value of options,

Widespread aversion to ‘sophisticated’ derivatives use.

Which means that the low take-up rate for option-based products is explicable and may arguably be rational.

Despite these, we question these ultra-low usage rates and posit that avoiding viable products in finance is irrational, likely self-defeating.

Is there a case for rethinking the use of options?

Our 2022 works demonstrated how premium aversion and premium illusion can serve to distort decision making in finance. The distortionary effects we pointed to tend to reduce option take-up rates, so we will leave that work stand.

Likewise, we leave others to consider whether administrative deterrents around cash flows and accounting treatments are sufficient to limit the options use case, though there are simple measures that can alleviate the cash-flow deterrent (premium in-arrears product variants).

Given this, the potential ‘for’ case in any rethink of options usage can be made on two grounds, one theoretical, the other more practical and economic.

The theoretical case for a rethink

Turning to economic theory, “indifference theory” has been a feature in economic works since the late 19th Century, typically in microeconomics studies of consumer preferences.

To leverage from the theory (without attempting to generate financial markets indifference curves), we should find general agreement with respect to the following statement:

“In the absence of other factors, if the economic outcomes (risk versus reward) of option-based product-use were known to be similar to that of alternatives (such as outright forwards or swaps), options use rates should reflect indifference and thus approximate an even share of activity across a sufficiently large and diverse customer base (such as that measured by the BIS Triennial Survey).“

To put this another way: if market participants were gaining advantages from the use of options to the same extent as from their alternatives, usage rates should be relatively even between the competing products.

So, what has been the historical pattern of the economic outcomes?

A comprehensive study of multiple asset classes and lookback tenors is beyond the scope of this blog. Nonetheless, in a study of strategy performance we should find that over sufficiently long timeframes, option premiums priced in competitive markets should tend to reflect the risks of the underlying asset. If, for example, they were consistently overpriced, few would ever hedge or speculate using options. If they were consistently underpriced, activity in forwards and swaps would be commensurately lower.

A relatively simple study of historic outcomes can demonstrate but not necessarily prove this.

Take the following study of hypothetical hedgers within the AUD/USD foreign exchange market:

AUD/USD Currency Hedgers

Serial six-month exposures,

Hedge products (strategies) deployed can be one of either:

Six-Month Outright Forward purchase or sale, or

Purchase of Six-Month Call or Put Options.

To determine comparative economic outcomes, we make several assumptions regarding ultimate pay-off conditions:

Where the outright forward is deployed the strategy ‘outcome’ is the average six-month forward rate over the study period.

For the option strategy we will assume that the pay-off rate is, market dependent, the average of the most favourable rate of either:

The option strike rate, plus or minus the premium paid, where the option expires in-the-money, or

Where spot traverses above/below the premium-break-even level favourable to the hedger prior to expiry (spot plus/minus option premium), allowing them sell or buy currency at spot and sell back the option for its remaining (residual) value, or

Some other rate between i and ii above (i.e., where the option is not exercised at expiry and the market did not hit favourable breakeven in the prior six months).

Assumption 2 will appear complicated and may seem restrictive in terms of assessing the value of the option strategy. However, our study cannot assign a value to the option buyer maintaining unlimited and unknowable freedom to leverage the option for profit. Our objective is not to determine a more profitable strategy per-se, but to accurately determine whether cost of option premium pays back the buyer within the bounds of pricing theory (i.e., consistent with the Black-Scholes paradigm).

We tested both strategies for hedge buyers and sellers using daily data running from 1st January 2002 to end September 2023 and found the following results:

The findings demonstrate a skew in outcomes, with buyer participants historically losing -40.7-basis point (BP) from use of (CALL) options instead of outright forwards and sellers gaining a +63.7 BP advantage from the use of (PUT) options.

Interestingly, the net benefit is a positive +23 BP buyer gain in favour of options usage. Though a wider study would be needed to provide more robust results, this suggests market participants shunning options use are missing potential value, particularly those on the importer side of the Australian financial markets.

This is a one-tenor, one currency, and one asset-class example that can hardly be labelled a ‘study’; however, it does point to there being reasonable inherent value in options product use and such use is worth fair consideration – not the obvious lack of interest as shown in the BIS study.

A potential practical factor

For those participants who remain uncollateralised as bank customers, options use may contain slightly lower initial transaction costs relative to forwards and swaps – i.e., at the point of deal execution.

Whereas payment of an initial option premium effectively collateralises an options trade, forward and swap products will typically need to be collateralised via the addition of an XVA charge.

The determinants of a final XVA charge range from credit (CVA) to funding (FVA) and capital costs (KVA). It is a topic that we may blog on in the coming year.

To summarise

As long-term market participants and observers of product trends, we have been surprised by the low take-up rates of option products that have validity. We are further surprised by the structural drift lower in option product usage rates in evidence within the BIS Triennial data.

If we consider the exceptional market volatility in interest rate markets since the demise of Global ZIRP (Zero Interest Rate Policy), we are particularly surprised by the low usage rate of IRO products.

Given the market disconnects between rational behaviour and the data, we intend to blog some more on this topic in 2023.