Lessons on the road to cessation – the JPY capital markets

In our last post we resorted to a smorgasbord metaphor to help carry the point that in the post-LIBOR world market participants have so many alternate benchmarks they should carefully evaluate for choice. Given some of the feedback, we thought it worth following up with a close look at progress in Japan. It’s a jurisdiction with a massive savings pool where benchmark choices appear somewhat different to USD and GBP.

What we found was more than interesting.

The USD market – real progress since 2019

On July 31st 2019, the world’s first SOFR deal settled; JP Morgan was issuing another piece of its regular preferred stock offerings. As Risk.Net sagely noted at the time, the issue had a “first-of-its-kind provision buried in the small print.” What they were pointing to was that the floating leg would “pay a forward-looking term rate based on SOFR, the secured overnight financing rate.” The $2.25 billion deal was set to pay a fixed-coupon of 5% through to August 1, 2024 thereafter switching to “a floating rate of three-month term SOFR, plus a spread of 3.38%.”

Which was quite brave of JP Morgan; term-SOFR had not yet hurdled regulatory approval let alone seen the light of day, and there could have been no certainty regarding the future viability of Term-SOFR.

Today, USD issuance in a SOFR format is more common than LIBOR, so much so that the CME run a SOFR Issuance Tracker, offer a wide suite of futures, and OTC market-makers have followed the obvious trend. Market conventions appear to have largely settled.

Looking into issuance data, what we note is that the hallmarks of a successful USD product transition are falling into place. Likewise, UK markets have carried-off a similar transition to their SONIA-based future, with markets now almost entirely absent GBP-LIBOR dealings. Thus, the crucial USD and GBP-based capital and financial markets appear to have the necessary features that promote their proper functioning:

For the sake of building up a point of comparison from which to judge the ARR scene in Japan, we review USD issuance since mid-2019.

Which to us is an impressive backdrop.

The Yen market – limited progress

In our comparative look at Japanese markets, we asked a simple question; what’s been happening in the market for JPY alternate reference rates (ARRs)?

Here is what we found for the same period (Mid-2019 onwards):

The Bank of Japan’s Cross-Industry Committee on Japanese Yen Interest Rate Benchmarks was established in August, 2018, and in November 2019, Quick Corporation’s forward-looking TORF benchmark was announced as the rate “most supported by public consultations.” The availability of an OIS-based TORF (in production since April 26th 2021) offers market participants a Japanese Term-SONIA lookalike in most respects, and it should be operationally easier than compounded alternates.

And JPY issuers have a range of other choices they can tap:

TIBOR, the Japanese Bankers Association administered rate, has been calculated and published as "Japanese Yen TIBOR" since November 1995 and is NOT scheduled to cease when JPY-LIBOR does.

Compound or Simple Interest TONA, could be thought of as Japan’s version of SONIA (unsecured, unlike SOFR), the modern form of TONA was introduced in 2016 and is administered and published by the Bank of Japan.

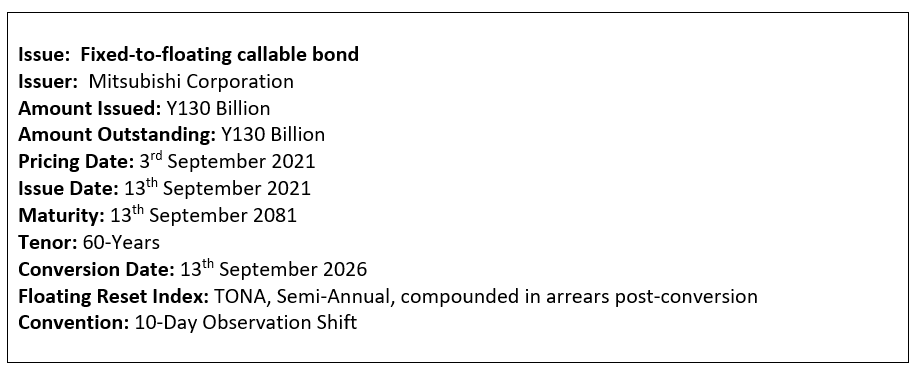

Digging a little further, we found that the single instance of TONA use in issuance was actually deferred until September 2026, coming as it does in the form of a convertible security issued by Mitsubishi Corporation:

What this points to is that notwithstanding the Mitsubishi callable (which we note could be called before it ever converts), there is currently not a single floating issue referencing compound or simple TONA, and none referencing TORF whatsoever (further queries on this with major data providers confirmed that there have been no TORF security issues).

We will follow-up this analysis with a look at JPY-based corporate and syndicated facilities in coming posts.

Digging still further we took a deeper look at historic behaviour of the various choices, and noted that the annual volatility (a favourite measure, expressed in basis-points of underlying yield) of different ARR’s, including those where a particular convention might be used can be vastly different.

Consider the following distinctive range of volatilities over the past 10 years data:

JPY-LIBOR is clearly the most volatile, which is not unreasonable given LIBORs credit sensitivity, whereas TONA variants and TORF do not. But this opens the question of: why does TIBOR not travel at a similar volatility to JPY-LIBOR? And looking across time, why has TIBOR remained where it is despite the collapse in JPY-LIBOR and TONA to negative rates?

This suggests that those looking to Japan’s capital markets need to tread carefully around benchmark liquidity as well as expected benchmark performance, and those offering JPY drawings have to be able to find appropriate points of funding.

Are Japanese institutional features at play here?

To help us answer the question of why JPY markets have largely ignored the development of ARR’s we turned to macro-economic texts and some research on the features of Japanese finance.

These indicate that there are a range of features at play:

Existing Bank of Japan interest rate settings continue to compress short-dated JPY yields, e.g., the JPY OIS Curve is negative to 4-Years, 9-Months

Forward yield projections are partially implied by the extent to which the Bank of Japan is expected to hit its “Price Stability Target” of 2% at a time when Japanese Core Consumer Prices have been negative for all but one of the past twelve months

The size of the household saving ratio in Japan (estimated at 11.4% percent for 2020) is the highest since 1994, adding to the existing Japanese savings pool

To the extent that Japanese Corporations require funds there is a long-run preponderance of bank funding over bond funding

To gain a stronger feel for whether these features are right we turned to a Japanese based interest-rate dealer, Stuart Giles a Japan-based interest rate dealer

RB – Stuart, you’ve traded Japanese markets and rates for an extended period, can you give us a feel for why Japanese floating-rate issuance is exceptionally low?

SG – Traditionally there’s been an over reliance on bank funding vs domestic market issuance, but this has changed marginally in the Covid-19 era. Demand for floating-rate paper remains low as it provides yield starved local investors little in terms of carry or potential for capital gain. With essentially no prospect of higher floating rates here I don’t expect this to change. Floating-rate issuance also serves no practical purpose for hedging ALM mismatches

RB – Can you see the TORF benchmark developing momentum and liquidity in the manner of say Term-SONIA or SOFR?

SG – With the recent pickup in liquidity in TONA, this increases the robustness of the TORF benchmark given that TORF is based on the uncollateralized overnight call rate. There are still some important issues with the use of TORF to be addressed such as the establishment of the governance structure and an improvement of transparency in the calculation process however.

RB – If you had to guess, what would be the prominent Japanese benchmark in 10-20 years’ time from now?

SG – A further shift away from TIBOR may require additional pressure from regulators, so near term I’d expect it remains the dominant reference rate. The momentum is clear however that risk-free reference rates are the global norm, and Japan will likely keep moving in this direction also. TORF is well designed with advance fixing and thus predictability of cash flow like Tibor/Libor fixings. Once we have the availability of cleared TORF products I think this benchmark can become the dominant reference point for markets.

Lessons

Our main take-away from these surprising JPY findings is that big assumptions can be quite dangerous. The Japanese economy and it’s institutional features and pressures have all ‘conspired’ to ensure that Japan’s capital markets are different to GBP and USD, and other currencies, and thus the path to JPY-LIBOR’s cessation is quite distinctive.

For those considering tapping one of the world’s largest savings pools the lesson here is that it will pay to fully understand the range of factors that drive your outcome; which is likely to rest in the fundamental nature of the underlying benchmark.