Term rates are crucial market infrastructure

Late in 2022 the Canadian Alternative Reference Rate working group (CARR) announced it would accede to market pressure and develop a Term-CORRA interest rate benchmark.

Somewhat unusually, CARR’s announcement was made prior to release of summary responses to their consultation on a potential new term rate. This was released on January 23rd.

Leaving aside the unusual delay, it is instructive to review the summary of the consultation’s responses. As I hope to explain, survey responses to regulatory surveys such as these give us important insights into the financial infrastructure requirements of a modern economy.

The market demand for Term-CORRA is telling. It tells us that Term Rates are crucial market infrastructure, not just a addition.

Recapping CDOR’s demise

We took a look at Canadian benchmark reform last year, see here, but to recap, the principal elements within Canadian benchmark reform are:

The mid-2024 cessation of Canadian Dollar Offered Rate, CDOR, the primary interest rate benchmark in Canada since market inception, with the proposed replacement rate being:

The Canadian Overnight Repo Rate Average, CORRA.

CORRA is Canada’s official risk-free rate based on daily transaction-level data on repo trades. These measure “the cost of overnight general collateral funding in Canadian dollars using Government of Canada treasury bills and bonds as collateral for repurchase transactions,” and is thus quite similar to USD-SOFR.

Similar to the approach taken in both the UK and US, and mirrored elsewhere, CARR has published its own well-laid transition roadmap to guide participants:

Source: https://www.bankofcanada.ca/wp-content/uploads/2022/05/transition-roadmap.pdf

What had been lacking from the Canadian plan was the development of a term rate similar to Term-SONIA and Term-SOFR.

Respondents emphatic call for Term-CORRA

To address the absence of a term rate solution, on May 16th CARR surveyed Canadian market participants to “seek feedback on the need for a potential forward-looking term rate (i.e. Term CORRA) to replace CDOR in certain loan and hedging agreements.?”

The survey responses were emphatic and instructive, for example:

Question 1) Does your institution need a Term CORRA rate?

All non-financial firms “wanted a Term CORRA benchmark”.

As did a majority of financial firms.

Overall, a clear majority (37 of 42 respondents) supported its creation.

Which to our mind is as emphatic a statement of end-user demand as any consult on this topic we have seen, clearly prompting CARR’s response as announced in October:

‘In response to the overwhelming support for a Term CORRA, CARR members agree to try to develop a Term CORRA, so long as a robust and IOSCO compliant rate can be created’, my emphasis added.

However, it was the feedback received on why firms felt they needed Term-CORRA that was most instructive.

To help summarise the feedback, I have bracketed the stated respondent reasoning into two areas:

1. Functional/Operational Reasoning:

cash flow predictability, including the need for accurate cash flow forecasting given hedge accounting considerations;

operational simplicity, thus obviating the need for treasury system overhauls, and reducing operational burdens on staff, particularly among smaller firms;

reducing the liquidity risk where a significant change in interest rates were to occur towards the end of an interest-period, firms may have difficulty acquiring adequate cash to meet interest by the due date; and

as a market basis for discount calculations where a present value is needed (e.g., financial reporting).

2. Commercial/Product Reasoning:

Non-financial companies noted:

hedging loan facilities (e.g., for derivatives products to hedge term SOFR-denominated USD borrowings to a CAD term equivalent) and other term rate exposures;

transfer pricing for inter-company loans;

as a reference rate when negotiating contracts with third parties (e.g., vendors, JV partners, customers) or related entities (e.g., partnership loans);

as a rate for inventory/receivables financing;

securitization products with floating rate tranches (asset-matching); and

financial leases.

Financial companies noted:

clients’ hedging activity (i.e., where firms require hedges for Term CORRA interest rate swaps, caps and floors based on the same benchmark);

derivative products, including the hedging of Term CORRA derivatives in the inter-dealer market (as US banks offering Term SOFR products are facing substantial issues managing the associated risks);

securitisations of Term CORRA-based lending; and

where operational constraints on some of the parties to the contract limit their ability to use overnight rates.

To which we are inclined to add:

Sharia-compliant products fundamentally require forward-looking rates (i.e., to establish rates of profit in-advance);

import/export financings of capital projects, in order to forecast cash flows or arrange outgoing foreign currency denominated payments; and

trade and commodity prepayments, for a range of calculations that by definition require forward-looking rates.

Which are all reasons why Term-RFR benchmarks can’t not exist…

We have delved into the topic of Term-RFR rates from several dimensions over the past year:

All of which have served to buttress our view that term rates simply can’t not exist in post-LIBOR finance; they are fundamental to the proper working of whole industry segments.

Taking this further, we see the proper evolution of term rates (bother in RFR and credit sensitive formats) as a desirable goal for the global regulatory family, particularly given trade and capital linkages between jurisdictions.

Then there’s the question of risk dispersion

As the CARR consult respondents noted, Canadian financial respondents wanted the ability to access an inter-dealer market:

Derivative products, including the hedging of Term CORRA derivatives in the inter-dealer market (as US banks offering Term SOFR products are facing substantial issues managing the associated risks) – my emphasis again.

Our evolving view is that while use-case limits are a not unreasonable consideration, they are a) likely unnecessary, and b) possibly responsible for a build-up of essentially un-hedgeable basis risk in dealer swap books that cannot be a positive for financial stability.

And understanding the Use-Case Limits

As I explored last year in Term RFR use limits; what use are they?, if use-case limits are here to stay, firms should start considering the use-case environment and their response quite carefully:

Ensure that use-case controls prevent dealing activity that contravenes regulator or industry preferences, and/or licensing requirements.

Establish a rules-based exceptions mechanism for allowance of Term-RFR use where use is warranted, and processes that document and track artefacts where use-case exemptions are approved.

Understand the peculiar reset risk that exists where Term-RFR’s are hedged via traditional OIS products.

Define and tag Term-RFR products as such, including within risk systems where unexpected basis and reset risk can emerge (between Term-RFR and traditional OIS hedges).

Ensure key staff understand term rates, their role in finance, their use-case limits, particularly where such staff are customer facing.

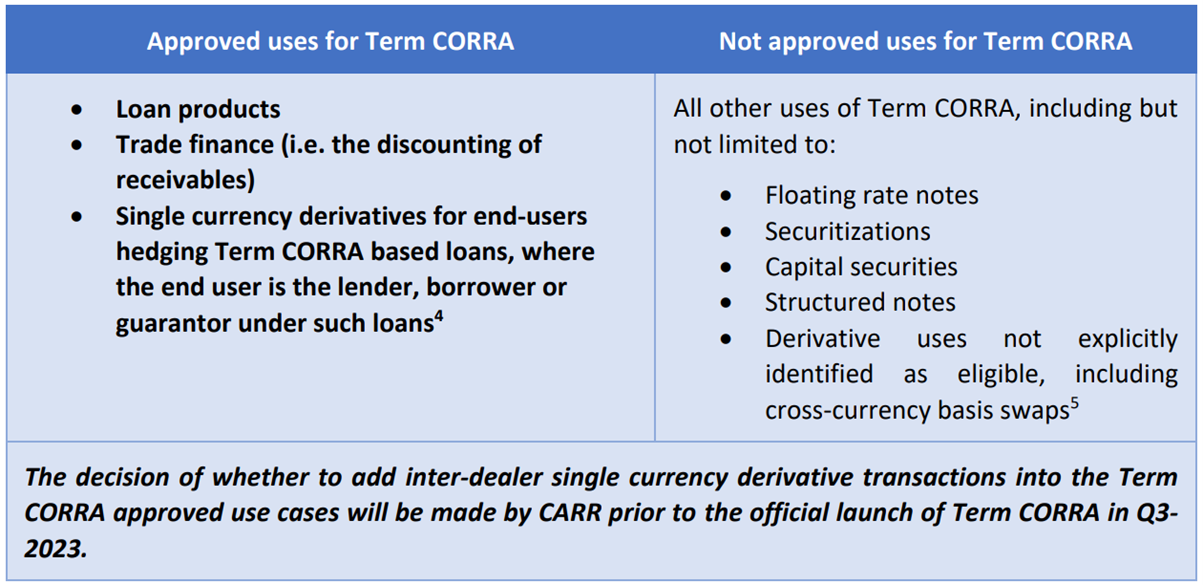

For Canadian-dollar risk, we would add that it will be important to understand the subtle variation that CARR has flagged already:

This appears to open up the possibility that a Canadian term rate could trade in interdealer markets, though how that might be ‘policed’ is another matter.

To our mind it would be better if the wish list of CARR’s Canadian respondents were met fulsomely, and preferably with a generous relaxation of use-case limits – a topic which we intend to explore in greater detail through 2023.

Summing up

Canada continues to surprise markets with the evolution of CORRA, and now a Term-CORRA benchmark solution. This is in a helpful alignment to developments in the US, where CME Term-SOFR activity continues to develop apace.

Other jurisdictions should be thinking about the market infrastructure developments that the Canadians see as crucial building blocks for finance and financial markets in an IBOR world.

From where we sit it really is hats off to the Bank of Canada and their Canadian Alternative Reference Rate Working Group.