XVA 1 - Credit Valuation Adjustment (CVA)

This blog looks at CVA in more detail and why it is important.

CVA is central to the pricing of derivatives and often forms a significant component of the spread paid by buy-side clients. CVA represents the credit exposure the bank has to the client over the entire life of the transaction.

Historically, credit spreads were calculated from tables which were updated from time to time.

They were a huge set of tables with all currencies, products and maturities. The bank’s dealer found the curency, product and maturity and matched the credit rating of the client. This was called the counterparty credit factor or CCF.

The calulation was very simple:

Cost of credit = CCF X Notional of the trade

Once the cost was calculated, it was converted into basis or FX points and used to adjust the price of the derivative.

But much has changed since then and the current methodologies are much more dynamic and market-related.

So much for history….

Thankfully, the pricing world has moved on from the basic approaches of the past.

Now most banks routinely use quantitative methods to calculate the CVA from live pricing, current credit spreads and the PV of the derivative.

From the previous blog:

CVA = -LGD * ∑ (EPE * PDc)

LGD = Loss given default (assumed to be 60%)

EPE = Discounted Expected Positive Exposure where only positive exposures are included

PDc = Probability of default of counterparty (market input)

The derivative is divided into a number of time steps and the EPE is calculated at each step (see below for the methods). The EPE is multiplied by the PDc to produce a potential loss (EPE) adjusted for the probability of that loss (PDc) for each time step. These are summed over the time steps.

Finally, the sum is multiplied by the LGD. The LGD adjusts the result for any expected recovery in the case of a default. The recovery rate is generally accepted to be 40%, so LGD = 100% - 40% = 60%

Probability of Default (PDc)

How is the PDc calculated?

Without going into the depths of the actual calculation, it is derived from the CDS (credit default swap) curve for the client. The CDS spread is converted to a probability of default for a specific period aligned to the time steps for the EPE calculation. This simply creates probability derived from market pricing of a counterparty default for that time step.

But what if there is no CDS pricing available? In this case, banks use an internal model to map the client to a known and observable (or derived) CDS curve and use that as a proxy.

The approximation for calculating PDc from CDS is:

Probability of default between ti-1 and ti;

PDs(i-1,i) ~ exp(-Si-1 * ti-1 / LGD) - exp(-Si * ti / LGD)

where, Si = the client credit spread at time i (i.e., CDS spread)

Expected Positive Exposure (EPE)

The EPE is used because the only time a bank has credit exposure to the client is when the client trade is ‘in the money’ for the bank, i.e., when the client owes money to the bank based of the forward valuations. For example:

an at the money interest rate swap has some time in and some time out of the money if the yield curve is not flat;

an interest rate swap with very large positive PV for the bank will have most time in the money; and

an interest rate swap with very large negative PV for the bank will have very little time in the money.

The EPE (from the bank’s perspective) will be impacted by the current PV of the derivative. The EPE will be less for an out of the money swap compared with an in the money swap.

How do banks calculate the EPE?

Basic method

This is very simplistic and just looks at the current PV at regular steps through the life of the derivative. It is based on the current market and is easy to calculate.

The basic method is very approximate and will almost always underestimate EPE.

Option method

The theory is that the price of the option out of the forward dates represents the value of one side of the trade such as the EPE. It is slightly better that the basic method but requires significant understanding of option calculations.

It is better than the basic method but is not used by most banks as it is too simplistic.

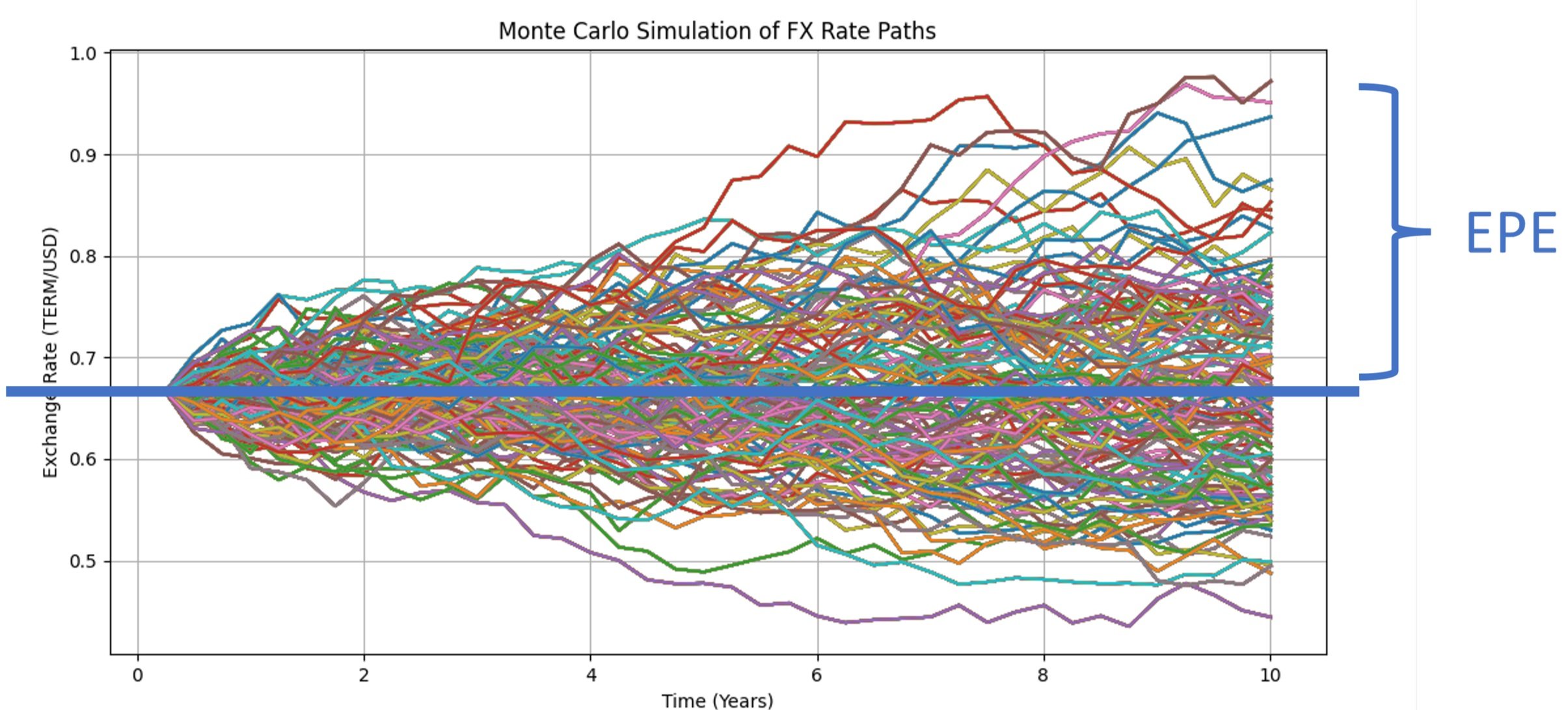

Monte carlo model

This is the most popular method as it gives more consistent results based on the current and forward market adjusted for volatility.

But this is not for the faint-hearted. The calculations are relatively simple but around 1,000 - 10,000 simulations are needed to get any chance of a correct EPE.

The following shows a typical simulation for an FX rate, in this case AUD/USD.

The EPE paths are marked and the actual EPE is the average of each path at the time point of calculation.

Summary of CVA

CVA represents the expected cost of the credit exposure of the bank to a client.

Best practice is to use monte carlo and CDS spreads to calculate the CVA.

CVA is dynamic: it changes over time as settlements occur, and market PV moves.

Banks always charge credit spreads, and the market practice is CVA.

Implications for the buy-side

This has some serious implications for the buy-side.

CVA is always a charge to the client.

Buy-side needs to be aware of the pricing and that banks do differ in their methodologies and inputs.

This means they will have different prices - so it pays to ask specifically for the CVA charge.

Derivative trade terminations are impacted - the buy-side should get a refund of the CVA charge included in the termination fee.

PV is important and trades that are significantly in or out of the money will attract very different CVA charges.

Recommendations

I always approach XVAs carefully while recognising different banks can use different methodologies and inputs,

This means they will have different prices, and it is important to understand their approach. Since I have been assisting buy-side clients with pricing and trade execution, I have been able to observe the way many banks price CVA. But I always calculate the CVA before approaching the banks so I can base-line the expected responses.

I suggest buy-side clients:

Plan trade execution and calculate the CVA before asking for pricing from banks - you may need some assistance in this calculation.

Understand why banks are pricing CVA in a particular way.

Negotiate and ask questions.

Be confident and get some independent assistance if required.

Good luck!