Trade execution methodologies and strategies

This is the first in a series of blogs which will look more closely into some successful approaches to designing effective derivative and FX trade execution strategies for clients. “Effective’, in my definition is a fair outcome for both sides of the transaction which also minimises any chance of offending regulatory and legal requirements.

For example, pre-hedging is one strategy that I have found very useful (when managed correctly) to reduce risks and achieve positive outcomes for clients. It is particularly effective in managing large trades and/or illiquid markets to avoid adverse price movements.

We have written previously on the topic of ‘pre-hedging’ and how this challenging matter can present both buy and sell-side market participants with real decisions.

This blog looks at identifying a preferred outcome, developing a series of potential strategies and deciding on the appropriate strategy to follow. Future blogs will look at examples of alternative strategies, how to you may choose to implement these strategies and managing counterparties.

Identifying the preferred outcome(s)

The first step is to identify and internally agree the preferred outcomes. Basically, if you do not know and agree how you want this to end, it is hard to make plans that support that end.

Some outcomes could include:

Is there a specific price or level that is important to hit?

In some cases, there is a price point that delivers an outcome which is required for cashflow, target price, accounting simplicity etc.

Do you have any counterparties you have to include?

Sometimes relationships and/or other dependencies on a counterparty may mean they need to be part of any trade.

Are there any other counterparties you would like to include?

Is there a balance between best price and relationship?

Are there any internal parties that need to be included in decisions?

For large transactions, the board may need to be informed, and they may have some specific requirements.

Prioritise the preferred outcome(s)

The next step is to prioritise the preferred outcomes.

If you have more than one preferred outcome, then they will need to be prioritised.

In most cases, you will need to compromise on lower priority outcomes if you need to meet the highest priorities.

Look at alternative strategies to achieve the preferred outcomes

There are many ways to achieve the outcomes, but a strategy suited to the market liquidity conditions, counterparties and preferences will greatly improve the probability of a favorable outcome.

Some of the strategies include:

Single counterparty only for the trade

Running a tender involving several potential counterparties

Using a syndicate of banks who all get some of the trade

Using a single bank to execute the hedge before novating the hedges to a syndicate of banks

Single bank to arrange a pre-hedge the trade before novating to a syndicate of banks

Etc.

And note, each strategy has merits and challenges!

Deciding which strategy to adopt for this transaction

It is important to match the strategy to the preferred outcome.

Not all strategies will be effective for all outcomes

So, a decision will need to be made as to the best strategy in this situation.

Summary

The better approaches spend time and effort on making sure the outcomes are well understood (and agreed) before proceeding to the strategy to get the best chance of achieved that outcome.

Not all situations are the same so matching the strategy to the conditions is also important.

The next blog will look at examples of the strategies above. I will look more closely at the merits and better uses of each strategy and the ways they may be used to get an effective outcome.

How to manage change in your life post trading - an interview with Kent Bray

Season 1 - Episode 8

Pre-hedging and the use of electronic execution platforms

Recently we published a podcast on the Martialis website where I discussed the development and use of electronic execution platforms with Anthony Robson. Anthony was CEO of Yieldbroker where they created the electronic trading infrastructure over 20 years and serviced the fixed income markets in Australia.

One of the topics we explored was the role of electronic execution platforms for pre-hedging of client trades by market participants. This has been a very important subject recently.

FMSB published ‘Pre-hedging: case studies’ in July 2024 which looked at the role of execution platforms in pre-hedging.

This blog looks at the FMSB case studies and relates the relevant example to my conversation with Anthony.

Recap on recent guidance on pre-hedging

Several industry and regulatory groups globally have provided guidance on pre-hedging in financial markets. We have reviewed them in previous blogs which can be found here, here, here, and also here. As you can tell, we have been busy in this subject!

One of the earliest examples of global guidance was within the FX Global Code first published in 2017. Principle 11 specifically addressed pre-hedging and was updated in 2021.

The FMSB has also updated their guidance in 2021. This has been recently supported by some case studies which are designed to assist market participants identify and manage pre-hedging activities.

The Australian regulator, ASIC, has also weighed in with a ‘Dear CEO’ letter published in February 2024. ASIC proposed 8 points which sell-side firms may use in any pre-hedging activity.

However, any advice or guidance can only assist market participants and will be subject to local regulatory and legal requirements. In other words, all market participants should pay close attention to the specific situation and their involvement in pre-hedging.

Most guidance emphasises any pre-hedging should be designed to:

Benefit the client or, at least, not adversely impact that client.

Be done with reasonable expectation of winning the trade. Note that a trader knowing they will win the trade in the very near future may not be consistent with ‘reasonable expectation’ and may constitute front running.

The role of electronic execution platforms

Returning to the FMSB, the 2024 case studies include 4 different examples of pre-hedging.

Case studies 1a, 1b and 1d all include using an electronic platform as the execution method. In all cases the client order is sent as a ‘RFQ’ (Request for Quote) in a liquid or illiquid market or product. The banks receiving the RFQ react in different ways based on whether it is a 1 or 2-way price request and/or by either pre-hedging or not. The trade is awarded to a single bank in each case.

The challenges for the banks receiving the RFQs on electronic platforms include:

Potential for the information to leak from the pricing desk to other traders thereby providing them with non-public information.

Pre-hedging may be permissible as long as it follows points 1 and 2 in the previous section.

While the time to respond to a RFQ may be very short (seconds typically) manual pre-hedging is impractical but algorithmic trading can quickly access electronic platforms. This needs to be carefully considered by banks and clients.

Illiquid markets and products present special challenges. While attempting to manage the possible position from winning the RFQ, a bank may impact the market price substantially.

I also note that the FMSB case studies include some client responsibilities to communicate clearly and honestly and be very clear about whether they accept any pre-hedging activity.

It is important to note that obligations and responsibilities impact both the intermediary (bank) and the clients.

The benefits of electronic platforms

The podcast with Anthony really highlighted using electronic platforms can have major benefits in managing risks as well as compliance with market obligations.

In the example of Yieldbroker (and I assume most platforms I have used), the electronic records of all activity are collected as a matter of routine.

There is a complete audit trail of activity that can be used for checks and analysis.

Platforms are generally required to conduct some form of surveillance to identify unusual behaviors or potential market abuse.

Orders and RFQs can be explicit about whether pre-hedging is permitted and record that agreement.

While it is possible to use another platform for pre-hedging apart from the one with the RFQ, it is possible to collect data from many platforms, check the time and activity and cross reference the pricing and trading.

Is pre-hedging permitted?

The simple answer is yes, provided it follows the rules and is agreed to by both parties.

Electronic trade execution platforms are often the dominant form of RFQ and trade execution especially in FX and fixed income markets. As such they have an important role and have functionality and characteristics which differ from voice markets.

How much is traded on electronic platforms?

The market data on turnover is difficult to gather accurately because it is spread across a number of different reporting entities including CFTC, ESMA, BIS, industry bodies such as ISDA as well as the platform providers.

However, it is generally understood that:

US and European markets trade approximately 70 – 90% of interest rate derivatives electronically due to regulatory requirements.

Around 30 – 50% of non-spot FX is traded electronically.

75 – 85% of spot FX is traded electronically.

I do note that these percentages can vary widely across regions and currencies but represent a significant proportion of the traded risk.

With relatively high percentages traded on electronic platforms, perhaps the FMSB focus on pre-hedging cases on those platforms is timely and relevant.

Summary

Electronic platforms for executing derivative and FX trades are well established and commonly used by market participants.

FMSB has recognised this and has recently provided a number of case studies of pre-hedging which related directly to the use of such platforms.

My discussion with Anthony Robson was very useful in understanding how the platforms are used and how they can provide great data for analysis of trading patterns. The complete audit trail including orders and trades can help identify when participants are trading and in what manner.

Electronic platforms are commonly used for trade execution and are very amenable to algorithmic trading: this aspect can create additional risks for market participants and may require additional controls.

In the case of pre-hedging, this could be detected by platform analytics and particular care needs to be exercised by all market participants to align their obligations to clients and markets with their trading patterns.

Calculating the market-based probabilities of official cash rate movements

Season 1 - Episode 5

Strategies for hedging financial market risk - going beyond pre-hedging

Season 1 - Episode 4

All the guidance in the world…

In February, ASIC released their Dear CEO Guidance for market intermediaries on pre-hedging setting out the Commission’s expectations in relation to a market practice that’s increasingly in the spotlight.

This was making good on a promise of ASIC Chair Joseph Longo, who back in 2023 noted industry’s “calls for guidance” on this thorniest of topics.

In this blog I ask a simple question: when it comes to pre-hedging, does ASIC’s (or anyone else’s) guidance matter?

‘Principles and guidance are great but they’re not enforceable. ‘

With these word’s the US-based Managing Director of a major global market association neatly summed up the rather uniquely Australian pre-hedging conundrum. Faithfully abiding by industry and regulatory guidance might be helpful, but it is only partially helpful if your trading patterns and deal outcomes appear to put you on the wrong side of the Corporations Act.

And what happens if you are on the wrong side of the Corporations Act, inadvertently or otherwise?

What we know is that it is the Corporations Act that matters. While pre-hedging situations may be rare, any ASIC investigative and/or enforcement action carries risk and almost certain business disruption (that can carry for many years).

ASIC’s Guidance

We‘ve blogged on this topic a lot in the past year, with John Feeney’s February post arguably the best of available summaries and one that helpfully provides a kind of guidance on the guidance.

Here I plagiarise in order to recap John’s points of what constitutes best practice in ASIC’s view:

Document and implement pre-hedging policies and procedures to ensure compliance with the law.

Provide effective disclosure to clients of the intermediary’s execution and pre-hedging practices in a clear and transparent manner – before any pre-hedging is conducted.

Obtain explicit and informed client consent prior to each transaction.

Monitor trade execution and client outcomes and seek to minimise market impact from pre-hedging.

Appropriately restrict access to and prohibit misuse of confidential client information and adequately manage conflicts of interest.

Have robust risk and compliance controls, including trade and communications monitoring and surveillance arrangements, to provide effective governance and supervisory oversight of pre-hedging activity.

Record key details of pre-hedging undertaken for each transaction (including the process taken).

Undertake post-trade review to determine the quality of execution for complex and/or large transactions.

ASIC went on to reminded CEO’s that:

‘failure to live up to these standards can be unfair and unconscionable.’

The market response?

It’s fair to say that the Dear CEO letter generated a lot of market interest and discussion among domestic and international firms alike. Some feel that ASIC has inserted a new higher standard with point seven.

For others, the insertion of point seven signalled the creation of what amounts to a uniquely Australian arrangement.

To recap ASIC’s pre-hedging guidance, point seven:

7. Record key details of pre-hedging undertaken for each transaction (including the process taken).

This is a definite extension of the guidance provided by both the FMSB and within the FX Global Code.

FMSB - Standard for the execution of Large Trades in FICC markets

Global Foreign Exchange Committee - Commentary on Principle 11 and the role of pre‐hedging in today’s FX landscape

And it doesn’t matter how large the underlying transactions are, the Corporations Act is in force down to the cent. The key point here is that the legislation does not appear to only refer to ‘large transactions’.

What are some of the practical risks and difficulties this creates?

It’s important to remember that when dealers are engaging in pre-hedging, they’re doing so as principals – i.e., as principal risk takers. They are also operating in risk-transfer settings, typically with multiple stakeholder interests to consider as they go about serving customers, managing an order book, and their firm’s own risks.

We also note that the dealing environment can vary between quiet periods of relative inactivity and periods of high turnover and volatility. In the latter the exercise of dealer discretion and split-second decision making are very normal, for example when market data is released or there is significant news flow.

We ask:

How do firms treat trades conducted in proximate time and price around the level of those that are recorded as pre-hedges for a specific transaction?

Is there a risk that by specifying a who-gets-what requirement for individual fills that a situation evolves where there is (real or perceived) ‘good-trades for us bad-trades for the client’ event ?

Which makes us think pre-hedge transactions should probably be recorded contemporaneously with a compliance operative present? But gosh, that adds a whole new layer of dealing oversight, complexity, and potential disruption.

We also ask, what if after all of the best compliance with ASIC guidelines, the market moves adversely against the client’s interests regardless?

There appears to be no easy answer to these questions.

So, does ASIC’s (or anyone else’s) guidance matter?

We’ve mentioned previously that we believe market intermediaries now bear a disproportionate responsibility for conflict-free, non-disruptive risk transfers in financial markets.

The latest ASIC guidance appears to add further to that burden.

We are also on the record as encouraging the development of guidelines for those who bring deals on the buy-side. But such guidance seems unlikely to emerge, at least any time soon.

In the absence of some new move to amend the Corporations Act, we therefore encourage firms to follow the guidelines with clarity, and think particularly carefully about:

documenting pre-hedging policies and procedures

recording the details of pre-hedging undertaken for each transaction

Our own mantra is worth remembering:

‘If it’s not written down it doesn’t exist.’

If it doesn’t exist, you probably have a risk you don’t need.

So yes, the guidance matters, and it matters a lot since a failure to demonstrate compliance will surely count against firms that become exposed to post-deal investigations.

The ability to demonstrably show compliance with the ASIC guidance may be all that actually protects a firm

Pre hedging and trading: A practical guide and recent experiences of balancing outcomes

With the recent regulatory interest in pre-hedging, there has been a predictable focus on how this will impact both sides of the market: buy and sell. The ASIC letter to CEOs and the impending IOSCO guidance will add to the existing FMSB and Global FX Code publications.

At Martialis, we have recently worked with intermediaries (i.e., banks) and their clients (corporates and non-bank financials) to look at the practical ways to manage trade execution within the regulatory and market practice guidelines.

This article summarises our recent experiences where the balance between the banks and their clients is managed for derivative transactions.

The buy-side

Buy-side clients are always very much on top of their balance sheet exposures. They really understand the funding and liquidity needs for their businesses and frequently use derivatives and FX to hedge exposures.

They often use derivatives as hedges against liabilities. The derivatives of choice are interest rate and/or cross-currency swaps which can be relatively simple or complex. The swaps can be restructures of existing positions or traded as new swaps.

In restructures, the same counterparty as the original trade must be in the conversation. Our observations have shown repeatedly that some banks do add cost to the trade simply because the client has little choice of counterparty; that is, they are ‘captured’.

New trades are different, they can be shown to a variety of banks and the competitive tension is much more clearly reflected in new deal pricing. The prices tend to be more aggressive, perhaps reflecting the approach that getting the deal allows for restructuring later (see the previous paragraph).

The sell-side

Banks and intermediaries have a tough balance to maintain: what is a realistic price, and does it cover my costs and required returns?

This balance can be difficult to manage and can lead to the typical dilemma: How do banks get to an attractive price while meeting target returns?

How does a trader manage risks in an existing book while not creating an inappropriate market impact that may be (or perceived to be) pre-hedging?

Sales staff are equally challenged to maintain the relationship with their client while only divulging the minimum, appropriate information to traders. Clearly there needs to be some communication, but what is considered ‘appropriate’?

In many cases, the sell-side is considering carefully the management of all trades with clients to balance the regulatory requirements.

What are we seeing?

Pre-trade market moves certainly appear to be happening, and we have seen such price moves in markets just prior to trading.

The price moves may not be associated with any potential counterparties, but it happens often enough that may not be a coincidence.

Is it pre-hedging? We cannot be certain.

Strategy is everything. For the buy-side, agreeing a clear approach before talking to any bank is imperative. As soon as we ‘break cover’ there is a possibility markets move against the client interest and/or we place banks in a position which amplifies the potential conflicts of interest.

Limiting the information provided to the banks and the timing of the release of that information can reduce risks (and costs) for both sides of the trade.

Dry runs are a must. The dry run will help align the pricing especially for restructures and complex trades. This gives us time with the client to identify outliers and negotiate the pricing well before the trade execution time.

Keep the actual execution time confidential for as long as possible. Dry runs help get pricing issues resolved but keeping the actual date and time of trading confidential minimises the potential for market moves related to the trade.

XVAs (CVA, FVA and possibly KVA) need to be priced independently. Banks can layer additional spreads into KVAs. This may be done by individual bank staff or as a corporate policy.

Getting an independent price for the trades and the XVAs before talking to potential counterparties gives our clients the ability to identify any anomalies and confirm the actual spreads they will be paying.

Just comparing prices from different counterparties is not very effective because differences in details which impact prices can go undetected. Getting a full breakdown of the trade mid and spreads means both sides can confirm the details and minimise the chance of miscommunication.

SummarY

Moves in markets just prior to trades for buy-side clients do happen. And it occurs with sufficient regularity to suggest this is not entirely coincidence. Whether this is pre-hedging or not is an open question.

However, if a bank is involved in a trade where the markets moved just prior to the execution of the trade, we recommend they look at whether there was any involvement by their traders. The activity may be unrelated, but it is better to confirm this at the time via an independent review.

A very effective sell-side practice is to look at the trade from the perspective of the client. If they intentionally move a market or pre-hedge, this may be ok if the client benefits overall. But be clear about this before the trade and review after the trade.

We are yet to see any disclosure from banks that they may pre-hedge a trade. At best it appears in the disclaimers (in the small print) but has not been explicitly discussed in our experience.

We continue to work with many market participants on both buy and sell side firms. Our best advice is to get independent and informed advice on the strategy and pricing before executing trades.

We know it’s a global issue - Part II

In 2023, ASIC Chair Joseph Longo foreshadowed increased regulatory interest in the market practice of pre-hedging, noting that his commission was aware of industry calls for guidance on the topic.

ASIC followed this up with their Guidance for market intermediaries on pre-hedging in February. While this no doubt has been welcomed by the sell-side, there remains little to guide those who actually bring large or sensitive transactions to market on the buy-side.

In this blog I follow up my earlier work on this topic and put forward some possible points of buy-side guidance.

We’ve heard your calls for guidance, and we hope to provide some soon.

With this, ASIC Chair Joseph Longo acknowledged what most who’ve worked on major deal risk-transfers know well – the available guidance on pre-hedging is written up in many places, none of which could be described as being definitive.

ASIC made good on their Chair’s hopes in February, squarely directing a new note: Guidance for market intermediaries on pre-hedging, at “market intermediaries,” with the Commission seeking to:

raise and harmonise minimum standards of conduct related to pre-hedging

improve transparency so that clients are better informed when making investment decisions

promote informed markets and a level playing field between market intermediaries, and

uphold integrity and investor confidence in Australian financial markets.

Adding a now familiar reminder:

Market intermediaries need to manage confidential client information very carefully and have robust, closely monitored and frequently tested arrangements for ensuring conflicts of interest are appropriately managed and in compliance with the Corporations Act 2001 (Corporations Act).

What we have noted is that a heavy set of obligations is now placed squarely on sell-side intermediaries in relation to pre-hedging. The default responsibility is for sell side firms to “minimise market impact”, and ensure they achieve “the best overall outcome for clients,” which we thoroughly unpacked in our recent work summarising the obligations – see here and here.

As we have noted, this latest guidance is consistent with global equivalents, providing intermediaries “with clear reference to the relevant Australian legislation and regulatory guidance.” But as we have also written before, there remains a gap in guidance with respect to guidance for buy-side.

Why guide the buy side?

While ASIC defines those bringing large deals to market as “clients” this is a simplification in any setting that includes exceptionally large risk transfers. When an entity brings a deal that is larger than the combined risk-limits of major bank dealing desks the notion of there being a client-party in any traditional sense becomes blurred. “Parties to a risk transfer” might be a better description, with one party seeking to lay off its risk problem to one or more others.

As we have seen, the conduct of the buy side can be exposed within court proceedings when exceptional deals turn to dispute, including in the most recent high-profile case.

Which suggests that minimum guidance for those who bring deals in which pre-hedging may feature is overdue.

This could include guidance aimed at:

Encouraging firms to establish an appropriate deal strategy prior to passing information-sensitive details to market intermediaries

Ensuring proper communications plans and controls are in place before large deals are brought to market –to make certain that execution-consistent comms are planned for, restricting sensitive information to a strict “need to know”, and avoiding information slippage

Removing the risk that Chinese walls inconsistent with their intended approach to deal execution, with partitions between corporate finance, credit, and operations teams, and the dealing teams who may be asked to manage market risks

Avoiding unveiling credit or collateral deal mechanics and related topics such as deal novation to relevant market risk dealers

Carefully controlling the number and type of firms that may be placed in contest for deals, while ensuring suitability-of-counterpart is considered

Reducing the chance that execution dry runs don’t transmit key information beyond that necessary to gauge price and/or ensure no market disruption can arise

Ensuring buy side parties consider time-of deal and time-to-clear liquidity considerations relative to the available depth of the market in question

Placing the onus on buy side parties to clearly and in written agreement specify pre-hedging assent if any, the manner, and type of approval required to permit pre-hedging deals and the recording of such dealings

Creating a genuine, level playing field through equal treatment of market intermediaries to be asked to quote

If provided, such guidance could be argued as raising and harmonising minimum standards of conduct for those who carry large positions they wish to disperse into the market. Such treatment would be consistent with the status of clients as dealing parties as specified within the Global FX Code and acknowledge conformity with International Organization of Securities Commissions (IOSCO), the European Markets Authority (ESMA), and the Financial Markets Standards Board (FMSB).

As the Global FX Code states, the code:

‘is expected to apply to all FX Market Participants that engage in the FX Markets, including sell-side and buy-side entities, non-bank liquidity providers, operators of FX E-Trading Platforms, and other entities providing brokerage, execution, and settlement services.’

With “clients” defined as:

‘a Market Participant requesting transactions and activity from, or via, other Market Participants…’

Market Intermediaries

The essence of our view is that market intermediaries now bear a disproportionate responsibility for conflict-free, non-disruptive risk transfers of large deals.

With the best intentions and fully complying with ASIC’s latest guidance, it’s entirely possible, even under the best conditions, that dealing outcomes convey an impression of having been the result of conflict or having disrupted a market, based on how the aggressor firm acts – what communication they convey and what style of execution conducted.

It’s little wonder that market intermediaries are now wary of large deals and have sought improved guidance. After all, if the existing pre-hedging guidance were clear, the ASIC Chair would not need to have acknowledged the widespread calls for it.

Placing clear and reasonable markers for those who bring large deals could ultimately help ASIC achieve its stated aim of promoting informed markets and a level playing field between market intermediaries.

Some practical approaches to ASIC’s February 2024 letter on pre-hedging - Part 2

We published a blog in February 2024 which looked at the content of the ASIC letter for market intermediaries on ‘pre-hedging’.

That blog was focused on our interpretation of the ‘Dear CEO’ letter which was written to many banks and intermediaries. In most cases, as is normal for ASIC, the firms were required to provide a response.

A significant challenge for intermediaries is the practical application of the contents of the letter. This is further complicated by firm’s obligations under the FX Global Code and the FMSB guidance on handling large trades which offer similar but subtly different guidance to that in the ASIC letter.

It should be noted that many market participants have signed up to the FX Global Code and/or are members of the FMSB so are bound by those publications.

In addition, IOSCO is due to publish the results of a survey on pre-hedging later in 2024. This will likely add to the mix of guidance and will have the backing of many global regulators (including ASIC) who are IOSCO members.

All the codes and guidance have overlaps but also have some differences. This is to be expected because each jurisdiction is bound by their legislation and regulations which can and do differ across regions.

So, what is an intermediary to do? This blog looks specifically at the ASIC guidance and offers some practical alternatives for firms to consider when looking to comply with the Australian requirements.

Our summary of the ‘Dear CEO” letter from the previous blog

We provided this summary in the previous blog. It is a useful starting point for practical ways to address the point in the letter.

‘While consistent with global equivalents, the 8 points provide intermediaries with clear reference to the relevant Australian legislation and regulatory guidance.

It is very important to note that this is Australian guidance, and it may not be identical with other jurisdictions due to the local environment.

The challenge for many firms is the practical implementation of the contents of the letter.

How do you define which transactions will require explicit client consent to pre-hedge?

Who is an informed client and who may need additional assistance to fully appreciate the implications of pre-hedging?

How do you define and measure market impact when markets can vary in both the liquidity and the participants in each product?

How do managers oversee the pre-hedging and ensure it is consistent with regulation and guidance?

Since the guidance is a ‘Dear CEO’ letter, how does a CEO ensure compliance?’

The summary poses 5 questions which we believe are important for intermediaries to consider for pre-hedging.

We now look at each question related to the 8 points provided by ASIC and offer some practical ways to address the contents of the letter.

The 8 ASIC points with thoughts on a practical approach to compliance

The 8 separate points follow which make up the guidance. The ASIC extracts are in italics and our views are in normal script.

‘document and implement policies and procedures on pre-hedging to ensure compliance with the law. They should ideally be informed by consideration of the circumstances when pre-hedging may help to achieve the best overall outcome for clients.’

Update the current policies and procedures with reference to pre-hedging if there is no explicit mention.

This could be assisted by using pre-hedging in the examples.

Provide updated training to impacted staff which specifically includes pre-hedging as a worked example.

2. ‘provide effective disclosure to clients of the intermediary’s execution and pre-hedging practices in a clear and transparent manner. Better practice includes:

·upfront disclosure, such as listing out the types of transactions where the intermediary may seek to pre-hedge; and

post-trade disclosure, such as reporting to the client how the pre-hedging was executed and how it benefitted (or otherwise impacted) the client;’

Include an explanation of the pre-hedging practices (that this may occur) in the pre-trade discussion and written material.

Include the specific instruments that may be accessed for pre-hedging.

Explain how this will benefit the client.

Outline any risks that may be present, e.g., price moves against the client.

Make it clear that price moves may not have resulted from pre-hedging and may be a result of unrelated market activity.

We assume somebody has spoken with the client about the trade to get their request and provide a quote. Adding some specific points on pre-hedging should not be too difficult given training and some pro-forma scripts.

3. ‘obtain explicit and informed client consent prior to each transaction, where practical, by setting out clear expectations for what pre-hedging is intended to achieve and potential risks such as adverse price impact. For complex and/or large transactions, the intermediary should take additional steps to educate the client about the pre-hedging rationale and strategy;’

Take additional care when assessing ‘where practical’. For example, if the client calls urgently for a price for immediate execution, then a long conversation may not be practical. In this case, it is difficult to see where any pre-hedging could occur because there is insufficient time for it to be undertaken.

Assume it is ‘practical’ and have specific processes in place to inform the client and get their consent prior to accepting the trade or order.

Have a very wide view of ‘complex and/or large’. This is relative to the client and what each firm may not consider complex and/or large may be just that for the client.

Assess the client and the trade and explain pre-hedging accordingly.

4. ‘monitor execution and client outcomes and seek to minimise market impact from pre-hedging’

Make certain you have accurate records of all trades and times.

‘seek to minimise market impact’ should always be a goal in trading but may not always happen so be aware of the possibility of a large move.

If this does happen, then review the trades and markets to establish the cause of the move.

5. ‘appropriately restrict access to, and prohibit misuse of confidential client information and adequately manage conflicts of interest arising in relation to pre-hedging. It is critical that appropriate physical and electronic controls are established, monitored, and regularly reviewed to keep pace with changes to the business risk profile’

The nuclear option: completely separate (different rooms) the sales and trading staff and ban electronic communications except on approved channels. Back this with clear instructions of what information can be passed between them.

The other option: physically separate the sales and trading so that discussions cannot be overheard. This may mean a distance of some meters and clear instructions on moving between the 2 areas. This will be supported by clear communication restrictions.

Whichever option a firm takes, make it clear that finding ways to circumvent restrictions is not in anyone’s interest and is strictly forbidden.

6. ‘have robust risk and compliance controls, including trade and communications monitoring and surveillance arrangements, to provide effective governance and supervisory oversight of pre-hedging activity’

Most firms already have oversight of their trading activity.

We suggest checking this includes specific alerts for pre-hedging and add them if they are not included now.

7. ‘record key details of pre-hedging undertaken for each transaction (including the process taken, the team members involved, and the client outcome) to enhance supervisory oversight and monitoring and surveillance’

Points 2 and 3 should provide the necessary inputs for the record-keeping.

However, if the pre-hedging is agreed prior to the trade, a post-trade review should be done -and transparency such as this is the kind of sunlight that can prevent downstream dispute of misinterpretation.

This can be relatively automated and done as business as usual.

8. ‘undertake post-trade reviews of the quality of execution for complex and/or large transactions. This should be performed by independent and appropriately experienced supervisory team members.’

Complex and/or large trades (see point 3) should get special attention for the post-trade review.

An independent person or team should be used to remove any suggestion of ‘marking your own homework’.

If there is a client complaint, then an independent review should be conducted.

Intentional or unintentional pre-hedging

Many intermediary firms are looking at how to manage their trading books in a complex environment of actual or potential client trades which may be seen as pre-hedging.

Traders need to engage with the markets to manage existing positions, including the working of orders in a complex book. Such activity could be interpreted as pre-hedging if a client trade is transacted or anticipated. This is the problem: is this activity pre-hedging?

A post-trade review (see point 8 above) could reveal trader activity which is consistent with pre-hedging but, in fact, is just the regular and necessary book management. This is unintentional and should be interpreted as such.

Intentional pre-hedging is completely different. Trading is undertaken with the explicit intention of hedging a specific trade and would clearly need to follow the ASIC letter.

But how does the intermediary firm decide whether the hedging is intentional or unintentional. And how do they review and maintain records showing how this decision was made?

This is a difficult question and will need to be specifically addressed by each firm according to their activities and internal policies. Clear and ongoing communication of intentions seems important here.

Summary

There is no question that banks and other intermediaries have existing positions which need to be managed. But how do they balance their pre-hedging obligations described in the ASIC letter with this normal activity?

We see the only practical approach could include:

· Recognise there can be intentional and unintentional pre-hedging activity and define them as clearly as possible.

· Make sure your policies and processes are supported by clear frameworks which maintain confidentiality and separate traders and sales information (point 5) specific for pre-hedging.

· If all trades are subject to pre-hedging disclosure and explicit agreement (point 3) make sure the scripting for sales staff is very clear and outlines all required information for clients.

· Unless you are very certain the client is ‘sophisticated’ in the product and market of the trade, make very certain the scripts are followed (points 2 and 3).

· Take extra care with large/complex trades, however you define them.

· Check your record-keeping and policies for post-trade reviews.

· Consider adding specific training for pre-hedging for relevant staff to the current requirements (point 1).

There is no correct answer or quick fix.

The approach will need to be dependent on the situation, the client and firm’s existing policies.

We believe all firms should be aware of their responsibilities and make efforts to specifically address the ASIC letter. While it may be tempting to assume pre-hedging is already covered in the current policies, this may not always be the case.

The letter makes the ASIC position very clear and the fact that they have decided to send a letter to CEOs emphasizes the importance ASIC attach to the practice f pre-hedging.

I'd encourage you to expand on these slightly. It seems like an abrupt ending.

The case for options – Part II…

We recently wrote of our surprise at a further deterioration in the relative take-up rates of option products across financial markets. Ultra-low options usage has been a feature of markets since the big bang, but do such low rates make any sense? We think it points to a likely lack of understanding of the when and why use-cases (plural) for options.

In this blog, we use a simple model to show why a blanket aversion to options use is not rational and can limit choices and potentially increase the costs of hedging.

The tired old use-case arguments

The first text we point to when we are asked how clients can gain a better understanding of financial options is Sheldon Natenberg's "Option Volatility & Pricing: Advanced Trading Strategies and Techniques." First published in 1994, this is a market classic containing the clearest explanation of pricing we’ve read. It adds to this with a comprehensive exploration of the trading domain and of a wide array of various trading strategies.

What’s unusual about Natenberg’s work is that it doesn’t delve into defining clear use cases for financial options, relative or otherwise. Though the use cases are implied throughout, there’s no depiction of the kind of market settings or circumstances in which using an option could hold advantages over, for example, outright forwards.

Given this, we list below some of the classic arguments for when options use is generally considered to hold advantages in comparison to alternates:

When a participant has elevated decision-making uncertainty about the future path of a financial market. For example, when there is an event such as a close election of high consequence or a piece of likely market-moving economic data. We have seen these types of environments before in the form of Brexit and the 2016 US Presidential Election.

When a participant anticipates a period of elevated market volatility that could make decision-making fraught. Most market participants will recall 2007-2009.

When a participant wants the certainty of a known cost versus the (theoretically) unlimited loss of a fixed hedge, for example in a situation where a contingent risk is confronted.

These are particularly relevant for managers who face performance benchmarks or are in a highly competitive trade-exposed industry. In these cases, the quality of decision making and application of the right product in the right environment takes on added importance since a performance light will eventually be shed on the quality of collected decisions.

A forgotten use case argument

But what of the state of the market itself? Should this be a factor?

At this point it is worth considering a hypothetical example of a historic state-of-the-market conundrum; one in which the use of options could be considered advantageous. While the example below is hypothetical, it will remind many market participants of actual events. This may or may not be a coincidence.

Consider the case of a heavily trade-exposed Australian importer with USD obligations in a highly competitive industry segment:

Dateline March 2001, the AUDUSD exchange rate is trading at 0.4975, having just broken below 0.5000 for the first time in history,

The company’s long-run viability is compromised if import invoices are met at an exchange rate below their breakeven hedge rate of 0.5000 for an extended period,

Having elected not to hedge (i.e., sell AUD forward) at levels above 0.5500 over prior months the company’s management calls a crisis meeting,

The company’s treasurer has prepared advice on whether the company:

Should hedge using a series of outright FX forwards to try to protect against a solvency problem.

Do nothing, thus taking a currency view.

Purchase a series of AUD Put options with amounts and expiries corresponding to those of the proposed outright forwards.

In such a difficult situation the existential risk to the firm is obvious but less obvious is the fact that the decision of management should also factor in a reasonable assessment of competitor behaviour given the market state. Have competitors hedged? Are they similarly exposed?

Here we have deliberately avoided pricing up forward rates and/or option strategies for this hypothetical. Why? Because they are unnecessary.

In such a situation the use case for an options solution becomes much greater than it might be if the AUDUSD were higher since use of outright forwards can lock the company into hedges at unfavourable levels (at breakeven) that simply defer a potential solvency problem.

By locking in forwards, the company cannot participate in the economic relief that might arise if the exchange rate were to recover (from all-time lows) – over the tenor of the forwards put into place. Others who make “better” decisions have a chance to participate in a market state recovery.

Hence, options are of clear relative attractiveness given this state-of-the-market.

For Australian exporters, a similar hypothetical example could easily be constructed for the extended period where AUDUSD sat above 1.1000 USD.

A test of this argument

What if we can test the state of the market argument in favour of options usage?

To do this we established a simple decision rule set-up for exporters and importers – and again we will use the AUDUSD exchange rate for our test. The arbitrary decision rules we will test using historic data run as follows:

Exporters always BUY Forward, except when AUDUSD is above +1 standard deviation “dear,” in which case they use an ATM Call option.

Importers always SELL Forward, except when AUDUSD is below -1 standard deviation “cheap,” in which case the use an ATM Put option.

The analysis presented here is based on averages that imply a daily process, which is of course quite unrealistic. Nonetheless, for both exporters and importers the average results are meaningful in the sense that on average they can expect to gain advantages of a similar dimension over time. The analysis holds whether they trade occasionally and on non-defined framework as far as timings are concerned.

The mean and standard deviation statistics are simply based on the complete historic AUDUSD dataset since 1990, not some arbitrarily picked moving average (from which we could be accused of playing around with stats to make things fit our argument).

Testing for 6-month AUD exposures on a serial basis (daily test), we compared the outcomes of serially using outright FX forwards versus the use of options when the market was unfavourably positioned above or below one standard deviation from long run mean. The options payoffs assumed hold-to-expiry conditions rather than a discretionary exploitation of, for example, periods of high volatility.

Our findings demonstrate that on average a forward-only strategy produced a rate of 0.78593. This becomes the benchmark against which our test “model” can be compared, and we found that the model improved all-in FX rates for both exporters and importers by the following amounts:

Exporter improvement from using the model +0.0011,

Importer improvement from using the model +0.0022,

Which is consistent with our intuitive feel for this simplest of hedging models.

Couldn’t these results be the result of dumb luck?

To ensure that the results are not simply the result of randomness, we decided to test the model across multiple tenors, with interesting results that are consistent with the original Black-Scholes paradigm (the advantage gets larger with tenor).

Testing for 3-month through to 6-month tenor horizons we found our model demonstrated the following economic advantages versus serial use of forwards:

Which tends to validate the state-of-market use case argument which we could summarise as:

It can be beneficial to consider options use versus locking in unfavorable forward rates when the market has moved materially against your interests.

Which implies hedgers should assess their product of choice in a proper framework (not simply copying this simplistic approach).

Put another way:

It could be considered irrational to use only one type of financial markets product in all market circumstances and states.

Is 11 beeps a big deal?

While the gains from this simple model appear small, this is again a question of relativities. A gain of 0.0011 for a firm that exports A$100,000 of goods or services amounts to U$110.00, but what if you were importing or exporting billions quarterly?

Our point is not about scale perse – it’s about appropriate strategy and having robust frameworks that can provide benefits, not least of which is the demonstration of best practice.

And if all firms employed such frameworks, with the associated controls and dealing delegations, we suspect the options category would be a more frequently favored category, more in balance with fixed hedges than is currently the case.

ASIC’s guidance on pre-hedging February 2024

ASIC recently (1 February 2024) released some guidance for market intermediaries on the difficult subject of ‘pre-hedging’ While not specifically mentioned, this was in the aftermath of Federal Court findings in a high-profile case of relevance.

This blog focusses on the content and provides some comments on the meaning of that guidance. Our next blog will build on the guidance and look more closely at the practical implications for both buy and sell-side firms.

ASIC also released a ‘Dear CEO’ letter which has some more detail on the obligations for intermediaries when considering and/or engaging in pre-hedging of transactions.

While ASIC acknowledge the role of pre-hedging in managing liquidity and price risks associated with client trades, there are considerable concerns about conflicts of interest. Specifically:

‘ASIC acknowledges that pre-hedging has a role in markets, including in the management of market intermediaries’ risk associated with anticipated client orders and may assist in liquidity provision and execution for clients. However, it can also create significant conflicts of interest between a client and the market intermediary which actively trades in possession of confidential information about the client’s anticipated order or trade.’

ASIC state that they have observed ‘a wide range of pre-hedging practices in the Australian market, with some falling significantly short of its expectations. Differences in pre-hedging practices can disrupt fair competition and the effective functioning of markets’.

International regulators including IOSCO, ESMA, FMSB and FX Global Code have all provided some commentary and limited guidance on pre-hedging. ASIC does point out that their guidance is in addition to and consistent with both the international practice and the Australian legal and regulatory requirements.

Our interpretation of the ‘Dear CEO” letter

The letter starts with some principles where the guidance aims to:

raise and harmonise minimum standards of conduct related to pre-hedging;

improve transparency so that clients are better informed when making investment decisions;

promote informed markets and a level playing field between market intermediaries; and

uphold integrity and investor confidence in Australian financial markets.

These principles are very clear, but the real guidance is in the section headed ‘ASIC’s Guidance’. The reference to the Corporations Act (section 912A) reminds CEOs of their obligations to act efficiently, honestly and fairly.

Eight separate points follow which make up the guidance. The ASIC extracts are in italics and our views are in normal script.

1. ‘document and implement policies and procedures on pre-hedging to ensure compliance with the law. They should ideally be informed by consideration of the circumstances when pre-hedging may help to achieve the best overall outcome for clients.’

This requirement is common to many ASIC better practices for trading financial products. The important point is to show documentation and ongoing training that supports the relevant policies and procedures.

It is imperative to ensure that the policies and procedures give clear direction on how firms decide whether pre-hedging will benefit the client.

2. ‘provide effective disclosure to clients of the intermediary’s execution and pre-hedging practices in a clear and transparent manner. Better practice includes:

upfront disclosure, such as listing out the types of transactions where the intermediary may seek to pre-hedge; and

post-trade disclosure, such as reporting to the client how the pre-hedging was executed and how it benefitted (or otherwise impacted) the client;’

Point 2 is quite clear that intermediaries need to be very specific where pre-hedging is beneficial to the client before the trading commences.

Detailed records will also be essential to support a post-trade report to the client as to how this was actually executed and how the client derived some benefit.

3. ‘obtain explicit and informed client consent prior to each transaction, where practical, by setting out clear expectations for what pre-hedging is intended to achieve and potential risks such as adverse price impact. For complex and/or large transactions, the intermediary should take additional steps to educate the client about the pre-hedging rationale and strategy;’

This point uses ‘explicit and informed’ when describing client consent and appears to preclude general comments about pre-hedging often included as footnotes to term sheets. It puts in place a requirement to obtain explicit consent, i.e., specific acknowledgement of the pre-hedging for that transaction.

There is also a need for sell-side firms to make certain the client is ‘informed’, particularly for larger or complex transactions.

We expect a ‘sophisticated client’ designation may not be sufficient to demonstrate the client is informed and aware of the detailed use of pre-hedging for a specific transaction.

4. ‘monitor execution and client outcomes and seek to minimise market impact from pre-hedging’

Proper record-keeping will be essential. Firms will need to show how they monitored the trade execution and what explicit steps for each transaction they took to minimise market disruption.

Note, markets may move as a result of firms’ pre-hedging. However, it will be up to the intermediary to demonstrate that this is for the overall benefit of the client and exercised with due diligence to not unfairly disadvantage other firms involved in relevant markets at that time.

5. ‘appropriately restrict access to, and prohibit misuse of confidential client information and adequately manage conflicts of interest arising in relation to pre-hedging. It is critical that appropriate physical and electronic controls are established, monitored, and regularly reviewed to keep pace with changes to the business risk profile’

This point is self-explanatory and follows current regulation. However, note the additional requirement to keep aligned with changes to technology and presumably monitor many channels of communication to maintain confidential material.

6. ‘have robust risk and compliance controls, including trade and communications monitoring and surveillance arrangements, to provide effective governance and supervisory oversight of pre-hedging activity’

This requirement is not new but the application to pre-hedging could be difficult to implement. We expect intermediaries will need to:

identify pre-hedging activity before commencing any trading

monitor the trading of both the teams pre-hedging and anyone else who may have knowledge of the transaction

perhaps provide oversight during and after the pre-hedging activity

7. ‘record key details of pre-hedging undertaken for each transaction (including the process taken, the team members involved, and the client outcome) to enhance supervisory oversight and monitoring and surveillance’

This point reinforces the requirements for record-keeping in the normal oversight and surveillance of trading. The focus is on the accuracy and completeness of the record-keeping after identifying pre-hedging activity.

8. ‘undertake post-trade reviews of the quality of execution for complex and/or large transactions. This should be performed by independent and appropriately experienced supervisory team members.’

The post-trade review appears to be above the requirements for other trading activity. This will likely involve all the items in point 7 above and a thorough review and report of the decisions and outcomes relevant to the pre-hedging activity.

Also note that the review is independent so Risk and Compliance teams will need to be appropriately skilled and informed.

Summary

The February 2024 ASIC guidance for pre-hedging is timely.

While consistent with global equivalents, the 8 points provide intermediaries with clear reference to the relevant Australian legislation and regulatory guidance.

It is very important to note that this is Australian guidance, and it may not be identical to other jurisdictions .

The challenge for many firms is the practical implementation of the contents of the letter.

How do you define which transactions will require explicit client consent to pre-hedge?

Who is an informed client and who may need additional assistance to fully appreciate the implications of pre-hedging?

How do you define and measure market impact when markets can vary in both the liquidity and the participants in each product?

How do managers oversee the pre-hedging and ensure it is consistent with regulation and guidance?

Since the guidance is a ‘Dear CEO’ letter, how does a CEO ensure compliance?

There are many other questions which we will address in our next blog. The focus will be on practical approaches to the guidance for both buy and sell-side firms.

The case for options

As long-term market participants and observers of product trends, we have been surprised by the low take-up rates of option products in evidence within the 2022 BIS Triennial data. The structural drift lower in option product usage rates doesn’t seem to make much sense.

In this blog, we take a look at the low usage rates, try to make sense of why options are being avoided, and explain why this may be irrational.

BIS data doesn’t lie

The BIS has been surveying financial markets since 1986. Its most recent triennial snapshot of the foreign exchange and OTC derivatives markets confirmed the steady relative trend away from the use of option products in financial markets.

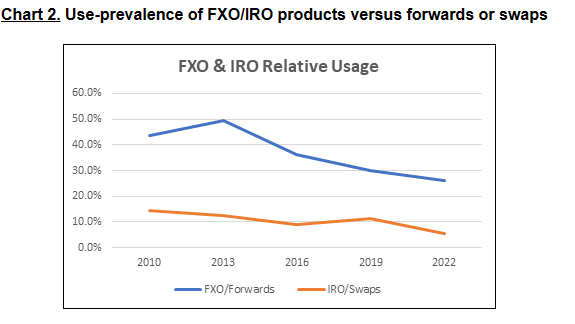

Since the 2010 Triennial, the simple proportion of daily foreign exchange options (FXO) turnover within the FX category has fallen from an already low 5.2% of activity to 4.1% in 2022. The decline has been more pronounced for interest rate options (IRO), falling from an 8.9% usage rate to 4.6%. T

A more concerning picture becomes apparent when we consider the relative usage rates between competing hedge instruments.

Again, using the BIS data, the split of activity between FXO and Outright forwards confirms the high-level story. In FX, for every $100 use of an outright forward only $43.6 of FXO products were recorded at the 2010 Triennial, falling to only $26.2 by 2022. In interest rates, the relative IRO usage fell from $14.3 per $100 of swaps usage in 2010, to only $5.3 per $100 in 2022.

And the use-prevalence of options among counterparts who could be considered pure hedgers (labelled by the BIS as “non-financial customers”) mirrors these wider trends.

With very worrying trends for IRO prevalence in the IR-derivatives category. For every $100 of swaps only $3.20 of IRO products are traded among non-financials.

It is important to note that these are relative declines off an already-low activity base. Nominally, both FXO and IRO markets have grown; just not at the robust growth rates seen in the wider FX and/or IR derivatives markets.

To summarise: despite healthy nominal growth rates, use of option-based products continues to lag wider industry growth off a low starting base. More is being traded, a greater aggregate delta of risk is being taken or hedged, but the option-based share of this activity is in long-run decline.

In our view this suggests market participants either don’t understand the nature of the products or are systematically avoiding them. A viable product set that should be even-handedly evaluated in relation to their alternatives is being avoided.

Why the long-run decline?

We presented work on the topic of ‘premium aversion’ and ‘premium illusion’ in finance in 2022, see here and here. In these we postulated that:

Premium aversion is the desire or preference to avoid paying premiums, regardless of the assessed value of an option holding in a particular risk setting,

Premium illusion is a mistake of premium value-interpretation and comes in two forms:

the impression that premium expenses are almost certainly irrecoverable, or typically worthless; and

the impression that non-premium instruments (e.g., outright risk positions) are ‘free’ or contain no potential future premium in the form of opportunity, or actual loss.

In our view, both premium aversion and illusion are barely disputable as factors that serve to reduce the rate of options use.

Yet, aversion to paying premiums could be described as a constant factor, not one that should be weighing more heavily as financial markets grow – particularly given the high underlying volatility of the pandemic and post-pandemic markets.

Among other factors, we would highlight:

Concerns over the accounting treatment for options given the up-front premium expense of traditional option products,

Cash flow impacts stemming from option premium payments,

A general lack of confidence in assessing the nominal and/or relative value of options,

Widespread aversion to ‘sophisticated’ derivatives use.

Which means that the low take-up rate for option-based products is explicable and may arguably be rational.

Despite these, we question these ultra-low usage rates and posit that avoiding viable products in finance is irrational, likely self-defeating.

Is there a case for rethinking the use of options?

Our 2022 works demonstrated how premium aversion and premium illusion can serve to distort decision making in finance. The distortionary effects we pointed to tend to reduce option take-up rates, so we will leave that work stand.

Likewise, we leave others to consider whether administrative deterrents around cash flows and accounting treatments are sufficient to limit the options use case, though there are simple measures that can alleviate the cash-flow deterrent (premium in-arrears product variants).

Given this, the potential ‘for’ case in any rethink of options usage can be made on two grounds, one theoretical, the other more practical and economic.

The theoretical case for a rethink

Turning to economic theory, “indifference theory” has been a feature in economic works since the late 19th Century, typically in microeconomics studies of consumer preferences.

To leverage from the theory (without attempting to generate financial markets indifference curves), we should find general agreement with respect to the following statement:

“In the absence of other factors, if the economic outcomes (risk versus reward) of option-based product-use were known to be similar to that of alternatives (such as outright forwards or swaps), options use rates should reflect indifference and thus approximate an even share of activity across a sufficiently large and diverse customer base (such as that measured by the BIS Triennial Survey).“

To put this another way: if market participants were gaining advantages from the use of options to the same extent as from their alternatives, usage rates should be relatively even between the competing products.

So, what has been the historical pattern of the economic outcomes?

A comprehensive study of multiple asset classes and lookback tenors is beyond the scope of this blog. Nonetheless, in a study of strategy performance we should find that over sufficiently long timeframes, option premiums priced in competitive markets should tend to reflect the risks of the underlying asset. If, for example, they were consistently overpriced, few would ever hedge or speculate using options. If they were consistently underpriced, activity in forwards and swaps would be commensurately lower.

A relatively simple study of historic outcomes can demonstrate but not necessarily prove this.

Take the following study of hypothetical hedgers within the AUD/USD foreign exchange market:

AUD/USD Currency Hedgers

Serial six-month exposures,

Hedge products (strategies) deployed can be one of either:

Six-Month Outright Forward purchase or sale, or

Purchase of Six-Month Call or Put Options.

To determine comparative economic outcomes, we make several assumptions regarding ultimate pay-off conditions:

Where the outright forward is deployed the strategy ‘outcome’ is the average six-month forward rate over the study period.

For the option strategy we will assume that the pay-off rate is, market dependent, the average of the most favourable rate of either:

The option strike rate, plus or minus the premium paid, where the option expires in-the-money, or

Where spot traverses above/below the premium-break-even level favourable to the hedger prior to expiry (spot plus/minus option premium), allowing them sell or buy currency at spot and sell back the option for its remaining (residual) value, or

Some other rate between i and ii above (i.e., where the option is not exercised at expiry and the market did not hit favourable breakeven in the prior six months).

Assumption 2 will appear complicated and may seem restrictive in terms of assessing the value of the option strategy. However, our study cannot assign a value to the option buyer maintaining unlimited and unknowable freedom to leverage the option for profit. Our objective is not to determine a more profitable strategy per-se, but to accurately determine whether cost of option premium pays back the buyer within the bounds of pricing theory (i.e., consistent with the Black-Scholes paradigm).

We tested both strategies for hedge buyers and sellers using daily data running from 1st January 2002 to end September 2023 and found the following results:

The findings demonstrate a skew in outcomes, with buyer participants historically losing -40.7-basis point (BP) from use of (CALL) options instead of outright forwards and sellers gaining a +63.7 BP advantage from the use of (PUT) options.

Interestingly, the net benefit is a positive +23 BP buyer gain in favour of options usage. Though a wider study would be needed to provide more robust results, this suggests market participants shunning options use are missing potential value, particularly those on the importer side of the Australian financial markets.

This is a one-tenor, one currency, and one asset-class example that can hardly be labelled a ‘study’; however, it does point to there being reasonable inherent value in options product use and such use is worth fair consideration – not the obvious lack of interest as shown in the BIS study.

A potential practical factor

For those participants who remain uncollateralised as bank customers, options use may contain slightly lower initial transaction costs relative to forwards and swaps – i.e., at the point of deal execution.

Whereas payment of an initial option premium effectively collateralises an options trade, forward and swap products will typically need to be collateralised via the addition of an XVA charge.

The determinants of a final XVA charge range from credit (CVA) to funding (FVA) and capital costs (KVA). It is a topic that we may blog on in the coming year.

To summarise

As long-term market participants and observers of product trends, we have been surprised by the low take-up rates of option products that have validity. We are further surprised by the structural drift lower in option product usage rates in evidence within the BIS Triennial data.

If we consider the exceptional market volatility in interest rate markets since the demise of Global ZIRP (Zero Interest Rate Policy), we are particularly surprised by the low usage rate of IRO products.

Given the market disconnects between rational behaviour and the data, we intend to blog some more on this topic in 2023.

Summary of the FOMC and RBA rate change expectation for Q3 and Q4 2023

I have continued to post the rate expectations for FOMC from August to December 2023.

Expectations have changed considerably in that time and reflect the changes in expectations for the inflation rate which is reflected in the market expectations for cash rates.

The following sections show the evolution of market expectations for rate changes in US and Austalia from August 2023 unti the present.

FOMC

No change to the target band since July 2023

Currently at 5.25% – 5.50%

Expectations of a rate rise have dramatically reversed by December 2023.

Now markets expect a fall of 25 – 50 basis points in Q2 2024 and continued falls thereafter

RBA

Increase of 25 basis points in November 2023 was widely expected just prior to the meeting.

Currently at 4.35%

Expectations have moved from a further 25 basis point increase to a 25% chance only.

Expectations continue to be volatile and closely follow the inflation figures with swings between 25% and 80% chance depending on the monthly CPI

Summary

Markets continue to change their expectations of cash rate moves in both US and Australia.

USA traders are pricing significant falls in the FOMC target cash rates in early 2024 while the Australian counterparts are still undecided and move their expectations as CPI data is published.

2024 is going to be an interesting year!

Pre-hedging - We know it’s a global issue…

At a recent ISDA/AFMA Forum, ASIC Chair Joseph Longo foreshadowed greater regulatory interest in the elusive subject of pre-hedging.

There can be little doubt that clear and consistent regulatory guidance on the topic would be well received, but this may actually be unrealistic.

In this blog I focus on why global clarity around pre-hedging has proven so difficult and share some thoughts on what regulators may be missing.

ASIC Chair

At the recent ISDA/AFMA Forum in Sydney, ASIC Chair Longo made the following comment in relation to pre-hedging:

We know it’s a global issue, so we’ve been engaging with ESMA on its call for evidence in Europe, as well as the FMSB and IOSCO, which is considering work in this area.

It is hard not to read this as an acknowledgment that the subject has multiple layers of complexity and that a globally consistent approach has, to date at least, proven elusive.

In separate news, Risk.Net reports that IOSCO is examining the question of “how dealers place hedges before executing trades,” and is expected to release its findings in Q3 2024. This is welcome, but some way off.

Pre-hedging?

So, what exactly is pre-hedging?

Here I submit standard industry and regulatory definitions, which are similarly framed but subtly different.

According to the European Securities and Market Authority, ESMA, pre-hedging is a practice in which a:

“…liquidity provider undertakes one or several transactions to hedge an order before it is received.”

The keyword being “before.”

While noting that pre-hedging is not defined under EU law, the authority concludes that:

“…pre-hedging is a voluntary market practice which entails a risk of conflicts of interest between the investment firm and the client/counterparty.”

The Financial Markets Standards Board, FMSB, has described the practice with a subtly different definition it its “Standard for the execution of Large Trades in FICC markets”:

“Pre-hedging is the management of the risk associated with one or more anticipated client trades. Pre-hedging is undertaken where a dealer legitimately expects to take on market risk in circumstances where such dealer does not have an irrevocable instruction from the client.”

The keyword here being “anticipated.”

The Global FX Committee, GFXC, provides a definition that describes pre-hedging in strictly legitimate terms:

“Pre‐hedging is the management of the risk associated with one or more anticipated Client orders, designed to benefit the Client in connection with such orders and any resulting transactions.”

While adding the highly important rider that:

“Pre‐hedging done with no intent to benefit the liquidity consumer, or market functioning, is not in line with the FX Global Code (Code) and may constitute illegal front‐running, depending on the laws of the relevant jurisdictions.”

These all provide useful individual points of guidance, but they cannot mitigate some fundamental problems that confront liquidity providers the moment information about a large or sensitive transaction first crosses an information barrier.

A number of very reasonable questions arise for liquidity providers (ESMA’s descriptor for sell-side firms) when a potential risk-transfer situation is first revealed:

Is there a clear, unambiguous, and enforceable pre-hedging agreement?

Can I trust the client (liquidity consumer)?

Who else is aware of the impending transaction?

What do these others know relative to my information?

Is my existing book at risk of loss given the potential transaction flows?

Could natural market factors move the market against the client if and when I execute pre-hedges?

Such questions could be thought of as the tip of an endless catalogue of questions in an endless range of potential dealing settings. Which may explain why a comprehensive and readily enforceable global standard has proven elusive.

Why so elusive?

It is not as if the conflict risk surounding pre-hedging is new.

The potential for large trades to convey sensitive market information is well understood and could be argued to be a problem as old as markets themselves. What is odd is that regulatory efforts to guide market participants with respect to dealing conduct are only relatively new.

Consider the following timeline:

2016 – FMSB, Reference Price Transactions standard for FICC markets,;

2017 – GFXC, FX Global Code;

2019 – ESMA, Market Abuse Regulation review;

2020 – FMSB, Standard for the execution of Large Trades in FICC markets;

2021 – GFXC, Commentary on the role of pre‐hedging; and

2024 – IOSCO’s pending pre-hedging investigation.

Which is all quite recent work, particularly considering that the US Insider Trading Sanctions Act was first enacted in 1984.

And these more recent efforts, though excellent initiatives, are tellingly somewhat different and come in the form of general industry codes or guidance. Which makes ASIC Chair Longo’s hint of possible ASIC engagement with ESMA, the FMSB, and IOSCO look all the more reasonable.

Some comments

Here I leverage the impressive work completed by the GFXC in 2017.

Firstly, it is clear from the GFXC FX Global Code that pre‐hedging conducted without the intent to “benefit the liquidity consumer, or market functioning” may “constitute illegal front‐running, depending on the laws of the relevant jurisdictions.”

“The intent of any pre‐hedging by the liquidity provider should always be to benefit the liquidity consumer and help facilitate the transaction.

Any pre‐hedging should be done in a manner so that it is not meant to disadvantage the client nor cause market disruption.”

What is unclear is how one proves “intent,” regardless of jurisdiction. As the GFXC concedes, intent “exists in the mind of a liquidity provider.”

Regardless of intent, what if circumstances arise that suggest pre-hedging contributed to an observable market move against the interests of the liquidity consumer? Or to an observable market disruption?

This problem of “intent” may therefore be intractable, a kind of wicked problem in financial markets and one bearing the unfortunate potential to mire relatively common market activities in protracted dispute.