Derivatives and USD Term Rates

This article continues the series on the practical uses of term risk free rates (Term RFRs) in USD. Previously, Ross and myself have both looked at the USD term rates where we are seeing significant interest in Ameribor, AXI, BSBY, Term SOFR, CRITS and CRITR. They all have uses and many market participants are actively looking at the way these new reference rates can complement[RB1] compounded SOFR and provide a more appropriate solution to their requirements.

In this article I look at derivatives and how these important hedge products are being introduced into markets referencing the term rates.

Derivatives referencing compounded SOFR

The market for interest rate swaps and cross-currency swaps referencing compounding SOFR is well established now and supported by price-makers and some end users.

However, the basis swap market is still developing with some swap pairs liquid while others are less so. Examples with significant liquidity include:

USD LIBOR/SOFR; and

Fed Funds/SOFR.

Some examples of developing markets with identifiable pricing include:

BSBY/SOFR; and

Ameribor/SOFR.

Other reference rates such as AXI, CRITS and CRITR have some pricing transparency, but it has been somewhat more difficult to quantify at this early stage.

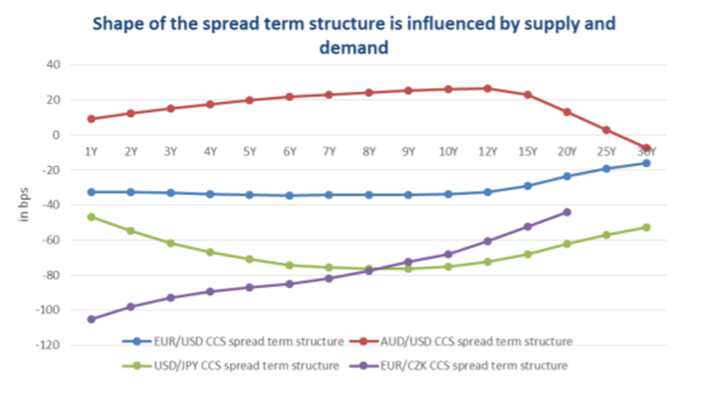

Basis swaps are not static and can vary considerably. The chart below shows the last 11 months (since BSBY has been available) of the USD SOFR versus other reference rates. Since there is some volatility (noting Fed Funds is on the secondary axis) many users may wish to hedge the exposure!

Basis swap markets are essential and provide different market participants the ability to transform their current risks to something more appropriate. For example, the combination of a fixed-rate debt issue by a corporate could be converted to and Ameribor reference by a combination of a Fixed rate to SOFR swap and a SOFR to Ameribor basis swap.

Of course, this can be delivered by a bank in a single swap, but the pricing would typically use the combination if a fixed swap and a basis swap to achieve the outcome for the corporate and a hedge in the inter-dealer market.

Derivatives referencing Term SOFR

Derivatives referencing Term SOFR are available for end-users. An active and available derivatives markets is essential to provide effective hedges for loans, debt issues and investments.

But there is a catch: the inter-dealer market for Term SOFR derivatives does not yet exist. Risk.net has a great article on this problem titled ‘Term SOFR restrictions spark valuation debate’. The Fed and ARRC guidelines restrict the use of Term SOFR derivatives and effectively do not allow inter-dealer trades.

This means dealer books can be one-way with the end-holders and there is no way to clear this risk in a similar way to other derivatives: i.e., hedging with other dealers with opposite positions or views.

There are no on-screen prices, so dealers are obliged to use internal models to replicate the valuation curves. While this is somewhat trivial (with the Term SOFR and compounded SOFR forward curves theoretically identical) there can be small differences due to hedging, collateral and one-way adjustments which need to be considered when building the curves.

In addition, if Term SOFR derivatives cannot be identically hedged then they may be consigned to the ‘structured’ book within the dealer firm and attract additional reserves and capital.

Either way, the absence of the interdealer market is very real and has consequences for all market participants who may use these derivatives.

Why does the absence of an inter-dealer Term SOFR derivatives market matter to end-users?

It matters for at least 2 reasons: cost and availability.

Firstly, dealer costs would very likely be higher for Term SOFR than for compounded SOFR. This is based on the provisions in the structured book and the higher capital applied to the trades. These costs will be passed on to the end-users.

Secondly, as dealers develop larger one-way books then internal risk limits may start to restrict the number and size of additional trades that can be added to the book.

The inter-dealer market could address both issues by allowing dealers to offset the risks with each other. If this cannot happen, then end-users must expect greater cost and potentially product restrictions and shortages which will likely lead to price inflation (which is quite topical in the economic sense).

What are we observing and hearing?

There is very clear demand for term rates from many buy and sell side consumers of reference rates. The reasons for the preferences of term rates over compounded SOFR are varied and include:

Current processes for operational management are difficult when you only know the refence rate at the end of the period.

Cash management is done well in advance for many firms and arranging for settlements and cash needs more than a few days to organise.

Accounting and planning processes are normally conducted when the rates and cashflows are known in advance of settlement.

Changes to interest rates (e.g., the recent Fed tightening) during a period can impact the costs and make planning for offsetting income more difficult to anticipate.

We often hear the expression ‘need or want’ applied to term rates. While many system issues can be resolved and remove part of the ‘need’, many process and planning issues remain and still represent a considerable ‘need’ as well as ‘want’.

Summary

The Term rates are gaining in popularity and use as more market participants appear to find them appropriate for their businesses. The loan and debt markets are expanding their use of term rates, and this shows no signs of slowing.

But there could be additional costs and restrictions. End-users will have to weigh the costs against the benefits for term rates in many processes and situations where they are appropriate.

Sell-side firms will likewise have to carefully consider how they price and manage the term rate risks while still offering a competitive product to their customers.

Assessing the Term Rate Menu

John recently updated the case for alternative US term rates, focusing on the emerging alternatives to compounded SOFR. Market evolution has seen at least six rather new alternative offerings emerge, all of which provide welcome, forward-looking competitors to compound or Term SOFR.

In this blog I add to John’s work by sharing some of our questions and listing some of the distinguishing features that make these evolving rates all subtly different. I also look at some of the recent pricing relativities, using the period of market stress generated by the Ukraine-Russia conflict.

We believe market participants need to understand the new offerings, particularly since, as John noted, turning a whole market from LIBOR to compounded SOFR is not without challenges, and for some a transition to backwards looking rates may not even be possible.

Questioning the Menu

Use of the Swedish ‘smorgasbord’ as a metaphor for the emerging alternatives to compound or simple risk-free-rates was very deliberate in my blog of October 2021.

The point?

Financial markets are proving different post-LIBOR; moving from the familiar, ubiquitous, and operationally simple system that LIBOR delivered, to a multi-rate environment, with a menu that includes the opportunity to avoid heightened credit sensitivity if one wishes to do so.

So, what is on the term rate menu?

At Martialis, we’ve followed the evolution of the menu with great interest from the ring-side seats of the consultant. Our part is not played as end-users, and we’re not financial product providers. Properly, we are benchmark agnostic, but we have been watching this space closely and from our vantage-point the need to amplify our call for end-users to better understand the new array of benchmarks continues to be real.

Questions

Distilling our view is best achieved by recounting some of the various questions we have raised ourselves, or that clients have raised and to which we’ve responded.

What follows is not an exhaustive list but are those we feel are of salient importance.

QUESTION: Under LIBOR the credit margin for any given credit was easily distinguished, simple to convey, and readily comparable among adjacent credits. Borrowers were easily able to compare quotes in any RFQ. In a multi-rate system, where each benchmark has distinctive characteristics within a mix of credit sensitive and insensitive alternatives, how do firms properly assess the price of a distinctive credit?

This appears almost impossible to answer at present. Markets will likely take time to adapt and settle within the multi-rate environment, and we can’t discount the possibility that a particular benchmark may eventually become dominant.

What we know is that some providers continue to lean on the ISDA Credit Adjustment Spread methodology to engineer a LIBOR-like base, essentially placing a transition-tool fixed spread based on a quite aged fixed five-year lookback of LIBOR-OIS basis.

It seems to us unlikely for this to continue indefinitely. Bank funding costs are a moveable feast, as the COVID and Ukraine war credit-stress events so ably reminded us (see graph below).

What we fear is a dilution of pure credit risk may take hold. Any blurring of the lines between sector credit risk and individual credit price is a bad outcome. Efficient capital allocation is not advanced in a system in which credit risk is blurred.

QUESTION: We are seeing some use of Term-RFR plus the fixed BISL spread across corporate finance; does that mean borrowers are realising some inherent advantage exists?

It may be that a perceived advantage exists, and the attraction of Term-RFRs has both an operational dimension (they’re relatively easy to implement), as well as a ‘credit insensitivity’ dimension.

This may prove illusory in the longer run, since banks themselves face variable funding; a reality that can’t easily be ignored ad-infinitum. If an extended period of more expensive bank funding were to emerge it is hard to see how a RFR or Term-RFR plus historic fixed spread could be sustained.

Consequently, we believe some interesting ‘credit’ pricing outcomes could emerge, for example it is possible that for realised yield outcomes the following may hold in some cases, and possibly persist in some markets:

(Term-RFR + Margin X) = (Term-CSRx* + Margin Y),

where Margin X > Margin Y

Note: CSRx = some Term Credit Sensitive Rate.

If this condition were to become common, it would imply that investors/lenders and/or the sell-side were willing to discount credit margins where customers elected to accept a credit-sensitive benchmark. This is a topic we intend to explore in a coming blog.

QUESTION: SOFR Academy (who partnered with Invesco Indexing as administrator) recently published prototype rates of their Across the Curve Credit Spread Index, or AXI, a dynamic credit-spread ‘add-on’ to SOFR. Could the use of such add-ons become common-place?

Note: Any prospective user of AXI that would intend to also use CME Term SOFR in developing an interest rate for Cash Market Financial Products or OTC Derivative Products would require a license with CME Group for use of CME Term SOFR.

Rather than pass comment on an individual alternative, I decided to ask the CEO of New York based SOFR.org, Marcus Burnett, for his thoughts on this question.

CEO Burnett: I think the vast majority of institutional liquidity will go to SOFR, whether compound, simple, or Term-SOFR, and recent data tends to support this.

It’s important to note that AXI can be applied to any variation of SOFR, so end-users have quite wide degrees of freedom as to the underlying convention that best suits them.

In launching AXI we will not create a path for banks to skip over SOFR, which is a key distinction between our offering and other credit-sensitive alternates. A loan that references AXI will also reference SOFR, so AXI is supportive of the SOFR-First initiative.

We believe SOFR plus a higher overall credit margin has the potential to be higher than SOFR + AXI + Credit Margin because banks have to include an insurance premium for their funding costs when the credit spread is embedded within an overall margin. Borrower margins traditionally only increase due to credit events such as a ratings downgrade.

We note that such an add-on affords users to retain their link to what we might regard as the official sector’s preferred rate (SOFR).

Which encourages us to think there is a long way to go before markets settle on a particular favourite, but credit add-ons present a particularly interesting dimension, and we cannot exclude major banks favouring their use. If syndicates were to follow-suit, a period of heightened market credit stress might forge their lasting use.

We’ll continue to monitor this topic with interest.

For those interested in the movement of various USD term rates through the Ukraine war credit stress event, I have taken simple daily benchmark rates and plotted them for Q1, 2022.

It’s interesting to note the relative stress differences, and to highlight these I simply use max-min to give an indicator of comparative credit stress.

We intend to look at credit stress events in greater detail in a coming blog but leave readers to draw their own conclusions on the interesting relative credit sensitivity evidenced here.

For those who’d like to receive a copy of our up-to-date Term-Rate summary paper, please e-mail us at info@martialis.com.au to request a copy.

Developments in USD Reference Rates

I have commented in the past on the emergence of alternatives for compounded SOFR in the USD market. Just as a reminder, compounded SOFR is the recommended replacement for USD LIBOR where the daily SOFR rate compounds this over a specific period and the rate is calculated a few days (typically 2 or 5) prior to the end of the relevant period.

As James Lovely pointed out to me in my previous blog, I neglected to mention Ameribor in my list of alternatives which will be corrected here! My reasoning at the time was that the target user base for Ameribor was quite different to the Martialis blog reader base but it should be included for completeness.

Current alternatives to compounded SOFR

Certain users of reference rates who have traditionally referenced the soon-to-be-discontinued USD LIBOR, can have requirements which do not naturally lend themselves to compounded SOFR. Turning a whole market from LIBOR to compounded SOFR is not without challenges and this transition may not be possible for some users.

The case for alternatives is very real for many users.

Here are the current alternatives (in alphabetical order):

Ameribor (AFX);

AXI (SOFR Academy);

BSBY (Bloomberg);

CRITS/CRITR (IHS Markit);

ICE Bank Yield Index (ICE BYI);

Term SOFR (CME); and

Term SOFR (ICE).

Right now, Ameribor and Term SOFR (CME) appear to be well supported with the other options still developing.

Firstly, let’s have a quick review of the features of the alternatives.

In general, there are 2 categories of alternative: risk-free and credit sensitive. Of the 6 alternatives above, only the Term SOFR is risk-free.

Risk-Free, Term SOFR

A risk-free rate does not include appreciable credit risk. SOFR, and therefore Term SOFR, is a secured lending rate with minimal credit risk.

In many cases, this is a particularly appropriate rate for users. For example, a corporate borrower can set the risk-free reference rate against an observable and defined rate (I.e., one which is close to the Fed target rate) and effectively pass on the liquidity and credit risk to the lender.

Any variations in the actual funding rate will be absorbed by the lender if it differs from the risk-free rate. Depending on the maturity and type of lending product, the cost or benefit will be priced into the lending rate and could be expected to reflect the risk to the lender.

For example, a 3-year bullet loan would simply include the known cost of funds that the lender could access for that maturity and principal. However, a revolving credit facility where the principal and term of the funding are not typically defined when the contract is negotiated, would have to price the uncertainty of the timing and amount of the loan as well as the potential market liquidity at the time.

While the risk-free rate may provide more certainty for the borrower, it may come at a price which reflects the risk to the lender in the product.

Credit Sensitive Rates

LIBOR has a credit and liquidity component embedded in the rate. Look at the USD LIBOR – SOFR spread since early March! It has moved up 30+ basis points. That is credit and liquidity in action.

The other non-SOFR rates have moved up as well and partly replicate LIBOR in performance. While they still replicate LIBOR much more closely than Term SOFR or compounded SOFR there are some differences. We will come back to this in later blogs.

The dynamic nature of the credit and liquidity spread within the credit-sensitive rates may make them attractive to some users. After all, LIBOR did have a use for over 30 years and did not attract any realistic competitors.

Ameribor, AXI, BSBY, CRITS/CRITR, ICE BYI and AXI are all variants of credit-sensitive reference rates. They all manage to include the same aspects of LIBOR which tracked actual market rates but ground the rates in actual transactions (unlike LIBOR).

It is this connection to the ‘real’ world which makes credit-sensitive rates attractive for some users. It is relevant to borrowers and lenders as the credit and liquidity pendulum swings both ways. Sometimes credit-sensitive rates benefit borrowers (e.g., the past 2 years where the LIBOR – SOFR spread was at a relatively low level) and lenders (e.g., now where LIBOR—SOFR spread is above average level).

Benchmark longevity and fallbacks

History suggests that benchmarks may come and go: LIBOR is a great example. Will all or any of the alternatives survive until the end of a contract?

Although this may be a risk, the management of that risk is something which should be factored into the use of any benchmark. The simplest way to manage this is to ensure each contract has an effective fallback to be used in case of a benchmark failure.

Summary

There is no right answer for which reference rate to use: it all depends on the person and the use case.

It is clear that there are alternatives to compounded SOFR and these are being used in USD transactions. The extent of their use will continue to develop as users are made aware of them and adopt the most appropriate reference rate for their needs.

The nature of premium illusion in finance – Part II

I noted in my last blog that I intend to write a series of blogs that examine premium illusion, describing it as an issue that market risk decision-makers may not realise they even encounter.

Premium illusion is a related topic within the field of financial loss aversion, which has been studied extensively, and which holds that it is basically natural to have a heightened sensitivity to losses versus gains. However, the not unnatural fear of financial loss from the paying of option premiums is quite chronic, but can be found to be unwarranted (illusory).

In this blog I’m going to turn from a market in which I knew (well, in truth I suspected) there would be solid evidence of illusion, to one that I don’t: the Foreign Exchange market.

I’m surprised by what I find with this rather simple analysis. I suspect readers will be too.

Premium illusion defined

In my last blog I did a rather poor job of explaining premium illusion.

Readers should note that the work presented here is predicated on my personal definitions, formed after having worked in markets for financial options for many years. They should also be aware that I have at times been a very heavy user of financial options and a serial payer of option premiums in various dealing settings.

Of definitions, there are plenty of obscure and some better-known financial texts that contain different definitions to my own. What’s important is not necessarily the neatness of the definition, but what readers are able to make of the data analysis presented in this piece.

With those caveats out of the way, I want to try and clear up a key distinction; while premium illusion is related to premium aversion, there are subtle differences in the financial markets’ product context. This is particularly the case where market participants consider the use of option products versus what we might call ‘non-premium’ products:

Premium aversion is the desire or preference to avoid paying premiums, regardless of the assessed value of an option holding in a particular risk setting,

Premium illusion is a mistake of premium value-interpretation and comes in two forms:

the impression that premium expenses are almost certainly irrecoverable, or typically worthless; and

the impression that non-premium instruments are ‘free’ or contain no potential future premium in the form of opportunity, or actual loss.

I should also mention that while option products are somewhat similar to insurance products, there are key differences, which is perhaps a topic for another blog. What readers should note is that typical price-setting frameworks for financial options consists of professional, two-way markets, where premium payers and earners trade freely with each other in increasingly transparent markets for implied volatility (that crucial common determinant of options value).

A crazy way to assess option value?

In keeping with the approach to assessing options value of my first blog, I look at value in a comparative setting between competing products, one containing an up-front premium, and one that does not. Readers will recall that I make no attempt to conduct an assessment of whether premiums paid resulted in positive option pay-offs at expiry.

Why?

Because the terminal pay-off approach can be quite misleading where risk-hedging is concerned. Also, studies of terminal payoffs have been done many times elsewhere, and of course such studies tend to show that options have a chronic tendency to expire worthless (another potentially misleading result and another possible future blog topic); our task here is to demonstrate whether there is a genuine value to holding intertemporal choice!

My approach is very simple. To recap:

Assume you are tasked with hedging a future short exposure to the AUD/USD exchange rate with a 1-Year horizon (i.e., typical of an Australian exporter)

Your mandate requires that you must hedge, but you’re left free to choose between:

entering a 1-Year forward purchase (i.e., hedging fixed)

buying a 1-Year call option to the forward expiry

Here, I exclude the choice of doing nothing for the reason that I am wanting to demonstrate premium illusion between competing financial markets products (doing nothing is certainly a valid strategy, but it does not involve competing products).

Data selection?

While it may be instructive to look at randomly selected data, and this may become a topic for a future blog post, in this study I am simply using ten years of AUD/USD FX data up to February 2022, comprising:

Outright Spot

1-year Forward

1-Year at-the-money forward call premium

There is nothing particularly special, and certainly nothing random about ten years (2,368 observations) of AUD/USD FX data. It is, however, topical for local and some international currency hedgers, and I hope to be able to show some serial features of premium illusion that local readers will be familiar with.

Why only 2,368 points in ten years? A typical market standard of options users is to apply a 262-trading day approach to annualization. However, while we have ten years of historic spot data, we only have nine full years of outcomes.

What are we looking for in the data?

This is the simple bit; we are asking the following question in 2,368 trials of call option outcomes versus outright-long forwards:

How often did subsequent SPOT fall below FORWARD minus CALL premium prior to expiry?

That is, having purchased a CALL option for a premium of X, how often did SPOT AUD/USD market subsequently move to a more favourable level below the outright forward adjusted for the up-front cost (X) of the option.

More favourable level? Yes, that’s the level where the hedger can purchase (and swap forward) at a rate more favourable than the prevailing forward. It’s typically referred to as the break-even level, but we have to be careful with that terminology in the context I am using it (since it typically refers to in-the-money break-even).

What are we ignoring?

The framework I’m using here is extremely basic; ignoring elements of potential options value that are particularly hard to assess.

A more robust study, including residual options values, requires a serious data analysis package and ten years of option ‘volatility surface’ data, thus making it a very large computing challenge. This may also become a topic of interest for us in future blogs, where we will be able to more fully demonstrate illusion.

What’s important to note is that the analysis presented below will certainly understate the full extent of premium value, and therefore the illusion in the AUD/USD market for CALL positions. This is for two reasons:

I make no attempt to estimate the extent of residual premium one could recoup by selling back purchased options when favourable spot levels present (wildly underestimating the value of the options strategy).

Likewise, I make no attempt to asses the extent of forward-rate conditions when spot falls to favourable levels, which given the fact that AUD typically trades at a forward discount to USD are likely to be quite advantageous (all-bar 31% of the observations in the data here).

However, notwithstanding the extent to which my basic analysis underestimates the potential value of optionality or intertemporal choice, value is still quite clearly indicated.

How often did a 1-Year CALL present greater value than a forward?

I mentioned in the introduction that even I was surprised by the results of this analysis.

Why?

Because I was unsure what it would show (there’s that randomness), and the results suggest there is a consistent advantage. Consider the following:

To interpret this, think of the results at each end of the spectrum shown here:

41.3% of the time a call option strategy outperformed a forward hedge within 3-months of its purchase date.

75.8% of the time a call option outperformed a forward hedge at some point in its comparable life.

Within 6 months of purchase, at some point, the option product typically outperformed the forward hedge (by quite a robust margin – above 60% of the time).

What the data is not saying?

It’s important to note that the question I asked of the data was how OFTEN did the call strategy beat the forward, not HOW MUCH did it beat it by. That is; I make no attempt to determine the average value gained when the option strategy pays off, since such an analysis would be too cumbersome and require too many forced assumptions to be viable (though I may take a shot at this in the future).

It’s also important to judge potential gains versus the average option premium paid to engage the CALL strategy. This averaged 0.03035 (303.5 USD pips per AUD) over the ten years, which is the average loss relative to the forward when the CALL strategy failed (i.e., 24.2% of the time).

As an early lecturer once made abundantly clear: there is no free lunch with options.

An example

By way of exemplifying the potential value I selected a single random date where there was a positive CALL outcome relative to the forward: 15th February, 2018.

Sticking with our simple hedger-example, we assume that on this day the choice of hedge for a 1-Year exposure is between:

A: An OUTRIGHT FORWARD at 0.79623

B: A CALL Option struck at 0.79623, costing 0.02605

The CALL can only potentially outperform the OUTRIGHT FORWARD if spot falls below 0.77018 (i.e., 0.79623 less 0.02605) at some point is the 12 months prior to expiry of the option.

Which is suggestive of a significant outperformance of the CALL in this single sample.

If we add in a rebate for the sell-back of the remaining CALL option value on three dates (3, 6, and 9 months respectively), the relative outperformance of the CALL can be calculated.

What about PUTS?

At this point it is reasonable to ask: Would PUT options analysis of the same data-set show similar results if we assume the hedge required were to protect against a falling AUD/USD rate.

It turns out that the results for PUTS are not wildly different to CALLS:

In other words, it hasn’t mattered whether we are looking at up-side or down-side hedges, option products appear to have a strong tendency to present favourable hedge outcomes in the historic data.

Is this sufficient to confirm premium Illusion?

The evidence of favourable relative value outlined here is quite strong, perhaps surprising, but is it sufficient to confirm widespread premium illusion?

The answer is no, not in isolation.

In an attempt to confirm the evidence of premium illusion I turned once more to Bank for International Settlements BIS data, which shows (as it did for IR-Swap versus Swaption data) that options use is far outweighed by that of outright spot/forward in product usage:

In other words, FX Spot/Forward product use appears to run at a factor approaching 7-times (6.8x) that of comparable FX-Options products, despite evidence of more balanced value outcomes between the competing products (and this despite the fact that the bulk of FX Options turnover is interdealer driven – approximately 3-1x).

Which suggests there is something fundamental that deters hedgers from deploying option products within hedge programs.

That something is likely to be premium illusion mixed with an overabundance of outright premium aversion.

Cross currency basics 5 – Portfolio versus individual deal hedging

This is the fifth instalment of my series on cross-currency swaps. Previous articles have covered the basics, looked at some pricing aspects and the revaluation challenges brought about by changing conventions and some examples of how cross-currency swaps are priced in practice.

In this blog I will look at how the portfolio and individual deal hedging works and some of the challenges for end-users.

Firstly a few definitions:

1) Portfolio hedging

Some firms, such as investment funds, have a number of portfolio managers and currencies where returns have to be converted back to the domestic currency. Other firms, such as corporates, may have revenue and costs in different currencies which likewise must be managed and/or converted to their domestic currency.

Some of these firms use a portfolio hedging approach where they broadly manage the risks and cashflows with a few cross-currency swaps and separately manage the cashflow mismatches with short-term products such as forward FX.

The following diagram shows this approach for EUR and JPY exposures swapped with two cross-currency swaps to USD.

1) Individual deal hedging

Another way to manage the currency exposures is to exactly match each risk with a specific cross-currency swap which converts each cashflow into the domestic currency. The aim is to minimise the mismatches and remove any currency risk from cashflows.

The following diagram shows this approach for the same EUR and JPY exposures but individually swapped with six cross-currency swaps to USD.

Portfolio and individual deal hedging each has benefits and challenges which need to be carefully considered before trading and also during the lifetime of the trade.

Portfolio hedging

This approach uses an overlay technique to provide a broadly-based hedge rather than look at individual risks. It is often used by larger firms who consolidate their currency hedging into a single desk. For example:

Large investment firms often use a mix of external and internal fund managers to spread risk and returns across currencies and management styles. This can result in many currency exposures which need to be converted to the domestic currency.

Large corporates can have a variety of debt and revenue exposures across currencies and maturities. This leads to a complex exposure where they need to balance the assets and liabilities per currency and ultimately back to the domestic currency

In these examples, the number of exposures and currencies can make a portfolio approach more efficient and easier to manage both operationally and for risk.

Benefits and challenges of portfolio hedging

Benefits include:

The number of trades is reduced, often resulting in more tractable system and process management.

The number of settlements is also reduced which can save on operational costs and reconciliation processes.

Challenges include:

The exposures are only approximately hedged which can lead to cashflow mismatches and tracking differences.

Accounting treatment can be complex (hedge effectiveness tests).

Short-term cashflow differences need to be managed with other products such as forward FX which can lead to additional costs and complexities (more on this in a later blog).

The maturity of the cross-currency swaps may not match the underlying risks leading to the potential for over or under hedging.

Allocation of the costs and benefits to each portfolio can be challenging.

Individual deal hedging

This approach exactly matches each exposure with a cross-currency swap. Many firms, especially ones with limited exposures to other currencies adopt this technique. For example:

Investment firms with only a few offshore investments tied to specific assets with known returns and maturities.

Corporates with offshore debt issues and domestic assets that the funding is directly supporting.

Individual deal hedging is attractive to many firms but, like portfolio hedging, has benefits and challenges.

Benefits and challenges of individual deal hedging

Benefits include:

The cross-currency trades will match the underlying exposure and the cashflows will net in the non-domestic currency thereby reducing the need for additional cash management.

Accounting can be simplified with the one-to-one match.

Challenges include:

The number of trades could be significant leading to additional system and process requirements to manage the settlements and reporting requirements.

This is not scalable – it is only effective for a relatively small number of exposures.

Which approach is better?

There is no answer for this question: it all depends on your circumstances. However, there are a few basic inputs to any decision:

How many exposures do I have or are likely to have? A small number may mean the individual deal rather than the portfolio approach as a more efficient and appropriate solution.

How sophisticated is my trading capacity? The portfolio approach assumes a high level of trade management and ability to successfully manage many settlement mismatches in various currencies.

How will my systems and processes manage? A large number of trades, which may result from the individual deal approach, may require advanced systems and processes. The potentially smaller number of trades in the portfolio approach can simplify the swaps but may complicate the forward FX management.

Do I have specific accounting and reporting requirements? This is definitely a consideration as it may favour one approach over the other.

Could I use both approaches? Yes, this is possible and may actually suit many firms with segregated businesses and/or exposures. For example, a single debt issue may be individually hedged but revenues may use the portfolio technique to better advantage.

As I said above, it all depends.

Summary

There is no simple way to approach the complex task of swapping non-domestic currencies to the domestic currency. Every firm with an exposure will have to manage the cashflows in some way and this is often done with cross-currency swaps.

It is vital to assess your operational and risk management capacity to make a decision. A recent blog by Ross Beaney about the need for clear frameworks is very applicable here. Without an honest assessment of your capabilities and an agreed framework for any actions, there is a real probability of a sub-optimal (i.e., disastrous) outcome.

A thorough analysis of your capabilities and exposures is a great start, or a great review of a current process. We have done this many times and really recommend a structured approach to minimise the risk of operational mayhem and/or pricing errors.

The nature of premium illusion in finance – Part I

Over the past three months I’ve devoted blog space to describing the nature and benefits of robust frameworks in the financial markets context. Changing tack from frameworks to a related issue, I’m going to write a series of blogs that examine an issue that those faced with market risk decision-making may not realise they encounter: the problem of premium illusion.

In doing so, I’m going to attempt to show that premium illusion is quite real, and why it can be a serial problem for those whose hedging frameworks exclude the use of option-based products.

To make these pieces more digestible I’m going to look at three simple cases that to me exemplify the problem, starting with the extended period of seemingly forever falling interest rates in the Australian interest rate markets. I want to stress up front that I chose, ex-ante, the Australian short-end rate market before I conducted any tests for actual evidence of premium illusion.

Falling rate persistency

As of this blog’s publication it is 4,131 days since the Reserve Bank of Australia last moved to raise the RBA Official Cash rate. That is, official rates have moved ratchet-style in only one direction for more than eleven years.

Mirroring these official moves, key interest-rate (IR) markets have moved in generalised lock-step with the prevailing cash rate, albeit with the kind of advance-and-lag process experienced dealers will be familiar with. This includes the recent heightened expectation of looming cash rate rises.

For all intents and purposes rates have been a one-way ‘bet’ for at least nine of the past ten years, and up until quite recently it has only rarely paid to hold outright paid-fixed IR-derivative positions.

For those tasked with interest-rate hedging, traditional IR- Swap programs that seek opportunities to fix forward rates have proved a burden throughout the seemingly never-ending decline in yields.

How can we be certain?

Here I will leave aside comparisons of floating-reset realised rates versus comparable spot-starting IR-Swaps for like tenors. This is because the nature of ultra-low short-term yield curves in the relevant period makes this a wholly unfair comparison.

Instead, I will look at realised rates of 1-Year into 1-Year (1y1y) forward-starting swaps versus comparable spot swap rates at each forward start date going back ten years.

Terminal Payoffs

Consider the case of a treasury dealer who has been required to periodically lock-in forward IR hedges via paid AUD 1y1y IR-Swaps.

Acknowledging that this is analysis by hindsight, it is still instructive to ask: how did this simple 1y1y forward hedging strategy perform against doing nothing (then swapping fixed via vanilla spot-swaps)?

The answer is, not well at all; the fall in rates was simply too persistent for forward paying to be of benefit.

Of 2,363 observed AUD 1y1y paid swaps, the realised outcomes since 1st February 2012 were:

In other words: 87.8% of the time the 1y1y forward rate paid exceeded the eventual 1y spot swap.

To summarise: IR-Swap hedging programs designed to periodically fix borrowing rates proved overwhelmingly costly versus simply doing nothing in the past ten years.

There was a persistent realised premium associated with forward hedging when we apply the following simple formula to the historic data:

What of comparable 1y1y payers swaptions?

For those unfamiliar with swaptions, an IR-Swaption is simply an option that gives the holder (i.e., the buyer) the right but not the obligation to enter into either a paid-fixed, or received-fixed IR-Swap (or a cash settlement amount equivalent to the intrinsic value of the swaption at the moment of expiry).

For all intents and purposes, swaptions markets operate like any other market for options, and OTC swaptions in major derivatives trade in $ trillions each year. They are quite liquid.

The standard pay-off for a swaption is quite similar to other such instruments.

For the purposes of display, I’ve created a hypothetical 1y1y PAYERS Swaption whose attributes I’ve made up from the rounded-up averages of available market data (May 2013, to the present):

Expiry: 1-Year

Underlying Swap: 1-Year Swap

Strike: 1.60%, i.e., at-the-money (ATM)

Premium: 0.45%

The counterintuitive

Having been involved in various options markets for many years I’m convinced that standard option “pay-off” diagrams that adorn the texts have served to mislead those who might otherwise use them as hedging instruments. In part, this has led to a chronic misunderstanding of the reason one should consider using option-based products when circumstances might make such consideration reasonable

Why?

Somewhat counterintuitively, the main benefit of option products when deployed as hedging instruments (not as expressions of trading views) is actually when the market moves against the prevailing strike, i.e., when the option FAILS to pay off.

Payoff diagrams serve to encourage the view that option buyers benefit only when the option moves in the direction favourable to the strike, but here I urge readers to think in terms of relative realised costs compared to fixed-rate alternatives.

Taking the example of our 1.60% PAYERS Swaptions, consider that:

1. If rates rise, the swaption protects the borrower at 1.60% for 0.45%, for an effective all-in swap of 2.05% fixed – the swaption can at no point ‘beat’ a paid-fixed swap at rates above the swaption strike price.

2. If rates fall, the borrower holds the option to let the swaption lapse and PAY swap rates at favourable levels (and if rates fall very quickly the borrower might PAY on swap at a favourable moment and sell back the swaption for whatever extrinsic value as can be recouped).

Point 2 almost perfectly describes the latitude the swaption actually provides which theoreticians call: intertemporal choice, which is a rather fancy concept that means the holder has time to pick a more favourable rate if one emerges. It describes the value of time in options products, affording holders freedom to choose favourably among given market states.

This is a long-underappreciated feature of option-based products, and associated strategies.

The 1y1y PAYERS Swaption versus 1y1y PAID Swap?

Over the slightly shorter 2,037 trading days (7 years, 9 months) for which we have swaption pay-off data what should be clear is that the swaptions performed similarly poorly to outright swaps. The rate markets rallied; rates went down throughout, both PAID Swaps and PAYERS Swaptions lost money outright.

But what about relative outcomes?

It turns out that PAYERS Swaptions outperformed PAID swaps with a not inconsiderable frequency:

To clarify

Let me pause here to recap and clarify what the data is telling us:

1. In the prevailing interest rate environment since 2012 forward IR hedges of all types proved costly,

2. Hedges proved costly almost 90% of the time (87.8% in the 1y1y)

3. The average hedging cost was 45.6 BP worse than doing nothing.

4. The alternative of PAYER Swaption hedges would have reduced this cost around 40% of the time – and likely more (given intertemporal choice), had they been used in place of PAID IR-Swaps.

It’s important to note that I’m comparing relative terminal outcomes between competing products, not expressing a view of outright gains or losses, nor am I seeking to push a product bias. As we will see in my next blog, there have been times when option-based hedges have been serially wasteful.

For those who maintained a hedge program, there are questions that could be asked:

§ Could deeper product appreciation of the potential benefits of optionality be deployed to your advantage?

§ Have you developed an approach to assessing whether fixed or options-based products are better tailored to your view or the prevailing environment?

How can we tell there is premium illusion?

In the market history I selected for this case study (1y1y AUD forwards, selected ex-ante) it’s clear that swaptions created opportunities for better hedge rates for vanilla swaps with good strong frequency, but I should concede I had an advantage in selecting the data, having traded my first option in 1989. The persistent fall in rates is a classic case for use of option-based hedges in preference to fixed hedges, and of course I knew this.

Yet, despite the 38.1% edge we find in the historic data, and the fact that option-based hedging instruments were clearly better tailored to a prevailing rate-environment, it’s not clear that the advantages hidden away behind pay-off diagrams are well known in the wider financial markets community.

So, I ask this question: if option-based hedges can be shown to be valid market instruments, why are they so infrequently used in hedging interest rate risk?

We know from long experience, from Depository Trust & Clearing Corporation (DTCC) data, and from elsewhere, that the use of options as hedges is dwarfed by fixed hedges across almost all markets.

The BIS data shows the poor take-up of option products emphatically:

Proportional market use by product-types:

Source: BIS

To our knowledge the use of interest-rate-options in global financial markets has at no time been above 10% of total USD derivative product usage, and in some jurisdictions the usage has been even lower. Worse, in our recent experience we have seen nothing to suggest any higher degree of interest in IR-Option hedges across markets, despite the volatility associated with COVID-19 and heightened uncertainty.

Which suggests there is something fundamental which deters people from deploying these products.

There are many possible factors at play here, some of which I will explore in a follow-up blog; but to my mind premium illusion or premium-aversion is very real, and at play. It alone probably explains the lion’s share of why market participants are so reluctant to actively consider options-based hedges.

As I believe this select example has shown it can be demonstrated that a lack of robust product understanding can really detract from hedging performance.

It simply doesn’t need to.

Cross currency basics 4 – Uses for buy-side and complex pricing

This is the fourth instalment of my series in cross-currency swaps. Previous articles have covered the basics, looked at some pricing aspects and the revaluation challenges brought about by changing conventions. This time I move to some of the uses for cross-currency swaps and how the trades are structured and priced.

Many buy-side participants in the market are looking to hedge real risks and/or move exposures or capital from one currency to another. The final price is often built from several markets and the outcome may be confusing or opaque. The inputs can use different reference rates such as SOFR or LIBOR, have 3, 6 or 12-month floating refixes and settlements and many other variants.

All this can be complex to price and understand when looking at a transaction.

This blog looks at some examples of commonly used cross currency-swaps and how some of the inputs to the pricing are used to build a final product.

Fixed to floating cross-currency

A very common trade is related to debt instrument issued in one currency with the proceeds to be used in another currency. An example is where an Australian issuer taps the USD debt markets with a fixed rate debt issue and wishes to use the proceeds for activities in AUD. The size of Australia’s considerable capital flows makes this trade a vital component of the financial system.

Another example is a French issuer also tapping the USD debt markets and swapping the proceeds back to EUR.

The outcomes are quite interesting and offer some insights to the pricing.

5-year USD fixed rate debt issue by Australian firm looking for AUD BBSW

In this example, the inputs and pricing approach is as follows:

Fixed rate debt is issued with yield 3.00% semi fixed coupons

USD IRS (semi 30/360 against 3-month LIBOR) with yield 2.00%

Calculate the LIBOR spread, SL = 300 – 200 = 100 bps

USD LIBOR to 3-month SOFR with spread 23 bps

Calculate the SOFR spread, SF = 100 + 23 = 123 bps

USD SOFR to AUD BBSW 3-month with spread 9.625 bps

Calculate the AUD BBSW spread, SA = 132.625 bps

As we can see, the number of pricing inputs and calculations is substantial, but the simple math works out ok.

However, this calculation ignores any convexity impacts. The correct price is actually SA = 133.625 bps which is 1 basis point higher because AUD interest rates are higher than USD interest rates and the convexity effect increases the spread.

Of course, points 2 -5 can be changed if the SOFR IRS is used instead of the LIBOR IRS. But remember that the SOFR OIS is typically quoted with annual fixed coupons which will also have to be adjusted to semi-annual 30/360 for the pricing to calculate SF.

5-year USD fixed rate debt issue by French firm looking for EUR Euribor

This example is quite similar to the AUD version except an additional basis market (€STR versus Euribor) is included:

Fixed rate debt is issued with yield 3.00% semi fixed coupons

USD IRS (semi 30/360 against 3-month LIBOR) with yield 2.00%

Calculate the LIBOR spread, SL = 300 – 200 = 100 bps

USD LIBOR to 3-month SOFR with spread 23 bps

Calculate the SOFR spread, SF = 100 + 23 = 123 bps

USD SOFR to EUR €STR with spread -20 bps

Calculate the EUR €STR spread S€ = 103 bps

EU €STR to Euribor with spread 16.20 bps

Calculate the EUR Euribor spread SE = 86.80 bps

As we can see, the number of pricing inputs and calculations have increased but the simple math still works out ok. Note also that we had to add points 8 and 9 because the USD/EUR cross-currency is quoted as SOFR/€STR and we are looking for the relevant spread to Euribor.

This calculation again ignores any convexity impacts. The correct price is actually SE = 78.10 bps which is 7.7 basis points lower because EUR interest rates are lower than USD interest rates and the convexity effect reduces the spread.

Implications for buy-side users

The number and complexity of the pricing inputs coupled with convexity impacts can make the whole process quite cumbersome and complex.

Market quotation conventions and inputs can vary across currencies and can sometimes be quite challenging to discover. Even small changes to conventions can make significant changes to the price.

As I mentioned in the previous blog, booking and valuation systems are also challenging for many users. The cross-currency trade you book will have to be revalued at some time and the inputs required to reconstruct to price are the same as the original inputs. All of these must be carefully defined in systems if you are to avoid valuation disasters.

Summary

I highly recommend all users fully understand the inputs to the pricing and at least perform a ‘back-of-the-envelope’ calculation to get an initial price check similar to the steps above. But nothing replaces a full pricing process which will adjust correctly for all conventions and convexity impacts.

An accurate price at inception is essential and it has to be supported through the life of the transaction for any amendments and valuations in systems and processes.

The possible uses for Term Risk Free Rates (RFRs) and credit-sensitive reference rates such as Ameribor and BSBY will be covered in a future blog. While these reference rates are not widely used at present, there is considerable interest from buy-sude users as they may be a better fit than compounded RFRs for them.

Martialis is actively supporting our clients in pricing generally and cross-currency in particular. We see these issues regularly but they quite solvable with some dedicated assistance.

That’s not a framework…

At Martialis, we routinely advise in situations where an absence or the presence of adequate frameworks has led to problems that client firms might otherwise have avoided; which explains our somewhat obsessional interest in promoting frameworks.

Obsessions aside, we do not suggest every minor firm issue needs a framework -far from it. But those that feature prominently in firm outcomes, particularly where issues may undermine the outcomes for firm shareholders, should be considered (if nothing else).

In this blog I venture into listing the attributes of what we believe constitute healthy frameworks, sharing the collected Martialis house view. It’s not the work of academia or a collection of on-line material, rather it is our experience of how solid framework brings positive results.

I start with an example of a framework which has stood the test of time.

An example of solid frameworks - Ray Dalio

Connecticut based, Bridgewater Associates is one of the world’s largest and most successful hedge fund managers. With circa U$150 billion under management, in certain size categories it would be considered the world’s largest, just as in certain return-series the firm’s returns have been simply Buffet-like, astounding.

Founded in a Manhattan apartment in 1975, Bridgewater has been a success at almost everything it has touched; from consulting, to research, and through to money management (particularly), and many readers will associate the firm with its founder and inspirational leader, Ray Dalio.

Aside from the many successes of Bridgewater, one of the things that singles the firm out as unique is Dalio’s preparedness to spread his view of how to build a great business (or great anything really).

He does this by promoting access to the firms Principles: Life and Work, which has been variously turned into:

Having read the earliest versions of Dalio’s work (in its initial e-book stage), like so many of my peers in financial markets I wanted to get a feel for how the Bridgewater founder thought; what was his firm’s recipe for success? At a mind-numbing list of actual principles (I haven’t counted them, but the condensed version lists 157), I love so many aspects of the list, but I’m not sure they can easily be lived by, and Dalio himself doesn’t suggest one actually try.

In making a point about Ray Dalio in a work exploring the importance of frameworks, readers should note that Principles mentions ‘framework(s)’ literally only three times. This might present as strange, but the reason for this is simple: Ray Dalio actually considers his work a framework in its own right, noting eventually (see page 315) that Principles is: “a framework you can modify to suit your needs (Principles: Life and Work, Ray Dalio, Simon & Schuster, New York, Page 315).

Which is my point.

Bridgewater’s success is well known to be the result of the firm’s leadership embracing Dalio’s Principles as their overarching framework. A framework that guides how people operate within the firm, not necessarily as we might infer, some codified system of rules and/or controls that manage specific matters.

The key is that Bridgewater has an amazing high-level framework that guides staff when they make decisions; witness the quite staggering compound benefits.

Principles or Frameworks?

One could easily argue all day about what constitutes a principle and what constitutes a framework. The two concepts are obviously related, though subtly different, but we believe they play important and somewhat different roles at different points in the hierarchy of firm management and control.

And the difference, subtle or otherwise, should not be dismissed.

Taking the Oxford Dictionary definitions in turn:

Principle: a moral rule or a strong belief that influences your actions

Framework: a set of beliefs, ideas or rules that is used as the basis for making judgements, decisions, etc.

Perhaps the best way to explain the difference is by resorting to the example of the founding of the United States as an independent nation.

The framers of the US constitution settled on a set of five guiding principles for the system of government they wanted to establish; which included: federalism, limited government, popular sovereignty, republicanism, with checks and balances.

These were enshrined throughout the Constitution that was eventually crafted, and it – The Constitution for the United States - became the crucial written framework for how the US form of government would work.

At Martialis, we believe that in a firm-management context it is this latter distinct and crucial difference between principles and frameworks that matters when it comes to how best to order firm workings:

Principles provide high-level guidance with respect firm directions and values

Frameworks establish rules-based structures in particular areas, circumstances, and where enterprise risks are present

Which brings us to the question of what constitutes a healthy framework?

Principles of Healthy Frameworks

In formulating the following, we naturally lean towards our experience within financial markets. However, we believe in most cases these could be applied to firms in almost any industry setting.

There are seven Martialis principles for healthy frameworks, in what is still for us a work in progress:

Principle 1 - Tailored for Task

Individual frameworks should be tailored for the specific circumstance, task, objective, or risk the firm wishes to manage or control; no more, no less.

The degree of tailoring is theoretically limitless, but we believe should be calibrated based on relevant elements such as:

Degree of subject-matter complexity

Degree of prescriptiveness desired

Formality, for example: guidance versus policy

In financial-market risk, macro-economic factors and correlations should also be considered and/or formally assessed when tailoring.

In assisting clients in a range of subject-matter, we are often tasked with cross-reference reviews into firm frameworks. In this we often note that elements of quite workable frameworks sit in disparate fragments, while others can be beautifully crafted and perfectly concise, while sitting hidden in tome-like volumes. We therefore recommend that any individual framework be tailored in ways that avoid fragmentation or the risk of the work becoming submerged (out of sight, out of mind).

Principle 2 - Designed to avoid reactive decision-making

Reactive decision-making can be argued to invite randomness into firm outcomes, particularly in financial-market risk settings. Ensuring a framework minimises reactive decision-making is crucial.

It’s important to note that for Martialis, we believe this should apply on both sides of firm outcomes, avoiding reactivity across different states, such as:

When markets deliver unfavourable conditions,

When market conditions are favourable,

When market conditions are stable/unremarkable

I note that very few of the frameworks we have encountered have any definition of what might be done when market conditions present opportunities.

In my most recent blog I recounted the story of a firm that had a ‘do-nothing’ framework based on a buffer-rate, while maintaining a significant (actually existential) firm sensitivity to an exchange rate. This unfortunately ensured that when currency market conditions favourable to the setting of longer-term risk hedges were reached the firm continued to do nothing.

In our view firms who seek to manage outcomes need to be mindful of the practical impact of the framework at both ends of the risk continuum, not simply on one side. In favourable circumstances rainy-day hedges can prove highly beneficial. Frameworks should encourage latitude to manage the upside as well as the downside.

Principle 3 - Accountabilities should be clearly defined

Where decision-making accountabilities are involved unambiguous accountabilities as to delegated authority are vital, and ideally formally maintained. This includes decision-making forums, particularly where a quorum is needed before time-sensitive decision making is prevalent.

Who is delegated to make a decision?

Who can make the decision in the event they cannot?

To whom is the decision-maker responsible, and to whom can a decision be escalated?

On what basis can they make their decision? E.g., do they require formal advice?

What is the boundary on the extent of their decision-making delegation?

What decision-making artefacts should be preserved once a decision is taken?

We mentioned in Principle 2, that reactive decision-making invites randomness into firm outcomes. This is often due to the fact that key decisions are often forced upon firms in time-sensitive settings, particularly where financial market risk is concerned. It is also the case that risk-reward asymmetry can play a role (a topic for a future blog, but losses are psychologically different to gains). Healthy frameworks are those devised to minimise decision-making ambiguity in all its guises’.

Put another way: ambiguity invites eventual disaster.

Principle 4 - Thresholds should be thoughtfully calibrated and consequential

Where circumstances demand the imposition of framework thresholds, for example in areas of stopping risk or losses, it’s important that the thresholds themselves be:

Carefully considered (and maintained on an ongoing basis where appropriate)

Respected

Monitored

Policed if necessary

This remains the case regardless of the decision-making latitude afforded to key staff.

Our firm has deep experience in managing teams in various financial markets settings, including settings which afforded key-staff quite generous decision-making latitude. It’s important to note that in these settings robust frameworks were not devised to prevent active management of financial risk, but quite the opposite.

Well thought out thresholds, for example: well thought-out loss tolerances, can promote good decision-making, but only if thresholds set and agreed are meaningfully policed.

Principle 5 - A framework should be formally recorded

Lack of formal recording of frameworks, particularly risk-bearing elements such as delegations and authorities can be as dangerous as the absence of a proper framework. We recommend a reasonable degree of formality be associated with the task, and proper recording is not difficult once a framework has been tailored and agreed upon.

Proper recording has many associated benefits, not limited to:

·Minimising confusion and downstream dispute

Ensuring stakeholder awareness

Facilitating appropriate 2nd/3rd line ex-post review

As a record of decisions-taken,

As mentioned in my last blog, the absence of formal record keeping of firm policies can present as a weakness of governance where firms are targeted in acquisitions.

Here I will simply remind readers of our standard refrain: If it’s not written down, it doesn’t exist.

Principle 6 - Good frameworks are memorable, and readily accessible

Overly complex frameworks and/or frameworks that are inaccessible in normal conditions to reasonably well-informed staff should be avoided.

In Martialis experience, illogical or overly complex frameworks can be self-defeating and open firms to dispute and/or policy non-adherence. Where framework records are poorly kept or buried within excessively large policy manuals similar problems can arise.

Logical, internally consistent, and easily understood policies that can be retrieved from internal firm libraries should be thought of as good practice that promotes framework effectiveness.

It was the highly regarded Austrian-American management consultant and educator, the late Peter Drucker, who coined the phrase: “what gets measured gets managed.” We’re not as certain of Drucker’s claim in the age of big data, but we do agree with the thrust and suggest firms consider what happens when things that can and should be managed are poorly managed.

Our experience suggests that if staff can’t give a reasonable elevator pitch about a particular topic, they either don’t understand it, or they aren’t aware of it. The same is true of frameworks. Well calibrated frameworks with appropriate thresholds that are readily retained by key staff are more likely to be deployed when circumstances demand they be deployed; not left open to the vagaries of chance or random outcomes.

Principle 7 - Good frameworks are memorable, and readily accessible

We believe frameworks should be subject to ongoing review, particularly in situations where market circumstances can change rapidly. Markets and economies are constantly evolving, hence frameworks judiciously formed in one setting can be found wanting, or even inappropriate.

This does not mean that the tempo of review has to be disruptive, nor onerous, but a degree of regularity can be expected to pay dividends.

We note that firms that review policies and procedures keep their frameworks current, and the simple process of review can lead to improvements not recognised at framework inception.

There are few elements of business that couldn’t benefit from a commitment to ongoing review. For firms in financial markets the post-GFC regulatory environment has turbo-charged the extent of necessary policy and compliance standards that firm policy-libraries are now basically overflowing.

But this is not likely to change; which means adaptation is key.

We believe that firms who accept the realities of ongoing review and adapt to the environment stand a better chance of negotiating future risks, and of maintaining the operational poise to gain from future opportunities.

Thus, well laid policies and protocols, modern and judiciously maintained, have an intrinsic value far beyond the costs of production and ongoing maintenance, and a regular tempo of review only adds to that value.

A tedious topic?

The topic is tedious, certainly; but should it be ignored?

We intend to write more on frameworks in coming blogs, which is something of a measure of how much emphasis we believe firms should place on their proper formation: making them and keeping them fit-for-purpose.

In the context of the risk-bounty found in financial markets, I will leave you with a simple quote from Ray Dalio, explaining his personal success in his 2019 CBS 60-Minutes expose.

Ray Dalio: “It’s 100% in those principles, in other words, principles are like, um, when you’re in a situation, what choices should you make? “

Cross currency basics 3 - Pricing and Revaluation Rate Sources

On 5 and 19 January 2022 I posted blogs looking at the basic features and some pricing examples of cross-currency markets. The focus was on the ways in which end users of cross currency swaps price and transact in the markets. In many cases, the concepts can be complex to understand, and the pricing can be difficult to unravel.

Many users are currently experiencing significant revaluation issues as the markets change from using USD LIBOR to USD SOFR as the basis for pricing. Screens and data sources are often unclear on which reference rate is being used. Pages and tickers that may have been sourced for many years have changed their reference rates which can cause disruption in the revaluation process. This can lead to differences in collateral requirements and accounting entries.

This blog looks at several currencies where the connection between the Risk-Free Rate (RFR) and LIBOR versions of the cross-currency market quotes may be less than clear. As the reference rates and market conventions change then what you see on a screen can also change.

Current market conventions

Cross-currency market quotes were, until late 2021, quoted against USD LIBOR and the currency IBOR. The ‘SOFR First’ effort of late 2021 encouraged cross-currency markets in the LIBORs to move to RFRs in late September 2021 and other, non-LIBOR currencies in December 2021. Now (February 2022), cross-currency swaps are commonly referenced to USD SOFR and the currency RFR.

Examples are:

Up to late 2021 Current

EUR/USD LIBOR/Euribor SOFR/€STR

GBP/USD LIBOR/LIBOR SOFR/SONIA

JPY/USD LIBOR/LIBOR SOFR/TONA

AUD/USD LIBOR/BBSW SOFR/BBSW

CAD/USD LIBOR/CDOR SOFR/CDOR and SOFR/CORRA

The two standouts are AUD and CAD.

In the AUD case, the markets currently adopt a mis-match approach with the AUD leg continuing with BBSW rather than AONIA (RFR).

CAD is quoting both CDOR and CORRA (RFR) but has announced the discontinuation of CDOR so I expect CORRA to prevail in the near future.

Other markets have local IBORs still being used mainly because of a lack of viable RFRs.

Pricing differences

How do the new quotes appear relative to the old versions? The following table might help with examples for the 5-year cross currency (XCCY) swaps. It shows the actual quotes for cross-currency trades and the LIBOR rates derived from the quotes and the relevant IBOR/RFR basis swaps.

Firstly a few key notes:

The IBOR/RFR spread for GBP and JPY is fixed since the LIBOR pre-cessation announcement on 5 March 2021

Other IBOR/RFR spreads are market rates

The quoted rate does differ (column 4) from the derived rate (column 6) particularly in the JPY/USD. I suspect the market quotes are using a simple calculation (i.e., subtracting the currency IBOR/RFR from the SOFR/LIBOR spread) and perhaps do not fully adjust for convexity. This will make a larger difference in JPY due to the interest rate differential between JPY and USD.

Quote implications for users

When you price a new trade or revalue an existing trade, it is essential you understand the quote basis of your price. The quote difference (column 5) shows how much the quotes can differ between the LIBOR (column 4) and RFR (column 2) versions.

In several cases, the actual reference rates are not clear in the screen quotes which can make the process of using the correct basis somewhat challenging for some users. Certainly, we have seen this when advising our clients.

System implications for users

Booking and valuation systems are also challenging for many users. If the quotes are using different reference rates to your trades, then they must be correctly transformed into the ones required. For example, if your trade is USD LIBOR/ Euribor and the quoted price is SOFR/€STR then your system will need some additional basis swaps, SOFR/LIBOR and €STR/Euribor, and the algorithm to incorporate them into the valuations to make all this work.

In many cases, systems are simply unable to use multiple basis swaps because they have not been updated with the required patches. When this situation occurs, the calculations must be performed ex-system and the required cross-currency basis swaps (e.g., LIBOR/Euribor) then used for revaluation.

This is a complex, manual process but cannot be avoided if the system cannot manage the new quotes.

Summary

Moving from the LIBOR/IBOR cross-currency market quotes to the new quotes has been a challenging process for many users.

Many quotes are now based on SOFR but many trades still reference USD LIBOR, at least until 30 June 2023. Some quotes use the currency RFR while others use the existing IBOR (AUD). Some are in the process of moving from the currency IBOR to the RFR (CAD).

It is essential to get the pricing and revaluations correct to ensure the accounting entries are accurate and collateral calculations, where required, will align with those of the counterparty.

Systems for pricing and recording cross-currency swaps often need to be updated. Where this is not possible, then some calculations will have to be done outside the system and the required rates then entered into your system in a second step.

Martialis is actively supporting our clients in this effort. We are seeing quite a few challenges, but careful analysis and planning can make the transition to new cross-currency markets and quotes a little less painful.

Why Robust Frameworks Matter…

At Martialis, we have a simple standard refrain: if it’s not written down it doesn’t exist.

In my mid-December blog I introduced the topic of decision-making frameworks and why they can be used to promote outcomes of higher quality in a range of fields exposed to uncertainty. I extended this into the area of hedging market risk, since financial markets are a field shrouded in uncertainty.

In today’s blog I am going to expand on this theme by presenting a catalogue of reasons why firms should carefully consider robust frameworks for managing market risk.

Charles had a framework

Working in financial markets in Melbourne in the early-1990’s I’d occasionally take a call from my entrepreneurially gifted friend Charles (a great friend to this day, but not his real name).

Since I worked in a major dealing room, Charles was always interested in what I thought of the Australian dollar exchange rate. It didn’t matter that I’d moved across from an utterly failed stint as a currency trader (FX-options) to an equally questionable time running a bond-option/swaption book, Charles wanted to know what I thought ‘Aussie’ might do (markets love their pet names); where was Aussie headed?

Charles business imported a unique brand of high-end outdoor gear and consequently had a particularly acute sensitivity to the value of the AUD/USD rate. His suppliers demanded monthly payments in USD while his sales were uniformly made in AUD, as is common among Australian businesses. Charles was “long-AUD,” in market parlance; if the Aussie fell his average cost of sales would balloon and his business would suffer accordingly.

Every so often I’d gently try to encourage Charles to ponder hedges that might help manage the obviously concerning risk. I’d find myself pricing up indicative combinations of forwards and various option structures, but I had to be careful; we were good friends and Charles needed formal advice from someone who didn’t have friendship skin in the game. That wasn’t me.

Then, in late 1995 on one of our calls, a large penny dropped for me: to the extent that Charles had a hedging framework it was that he’d simply budgeted on a low break-even exchange rate for the business. That is: all things being equal the business could survive profitably if the AUD remained persistently above USD 0.6400.

Charles had accepted a buffer based on an excessively big assumption, but not much else, and for an extended period the buffer strategy worked very well:

· Charles’ business average A$ rate for the five years to April 1998 for import goods approximated 0.7305, i.e., well above the necessary break-even.

· Through the 1996 calendar year the business enjoyed an average A$ of 0.7849.

· By simply covering payments with spot deals, Charles avoided the visually costly forward hedges that prevailed at that time (routinely 75-100 pips discount in the 1-year).

Until it didn’t.

In early 1998, with the global and Australian response to the Asian Financial Crisis, Australian term yields fell below comparable US rates and the AUD/USD dropped through 0.6400. It stayed below Charles’ business break-even for twelve months.

From April 1998 the average month-end spot rate was 0.6171, 229 basis points below Charles’ buffer, and a level which helped him decide to wind-up an otherwise successful retail business.

Despite this early-career setback, Charles managed to prosper in subsequent ventures and put the events of the Asian Financial Crisis behind him.

As my title of the December blog (The decision to do nothing is still a decision) attests: doing nothing is a decision, but could Charles outcome have been modified in the presence of a formal currency risk-management framework?

The answer is almost certainly yes, and I will mount a series of arguments as to why in the form of a high-level catalogue explaining the advantages.

Formality holds advantages (written policy matters)

It is worth considering the inverse of our axiom that what’s not written down and/or signed-off in a business doesn’t really exist, to-wit: what’s written down and signed-off matters and can matter a lot in certain circumstances.

While major firms lean heavily on formality, the establishment of well-written formal policy can matter in any business context in firms of any size and circumstance, for example in a well-defined market risk hedging program:

delineating who in a firm can hedge what, when and how;

avoiding confusion, inertia, and/or internal disputes ex-post and otherwise, and

promoting accountability, particularly decision-making accountability.

For firms exposed to market-risk that is meaningful (particularly relative to non-market factors) the presence of a written policy is crucial if the business is ever required to demonstrate that enterprise-outcomes were overwhelmingly the result of carefully geared management, not the result of unrepeatable factors or random chance.

This has proved a particularly sensitive topic in the case of businesses being targeted by an interested acquirer with the thorny question of: how did you decide to hedge or not hedge?

Delegations define latitude