Execution Costs – Mysterious or manageable?

One of the less well understood areas of finance is the impact of transaction costs on standard risk-reward models. While market makers with deep experience know that transaction size impacts costs, this is often not communicated to end market users in a transparent or quantitative manner.

In this first of a series of pieces, I use the efficient-market hypothesis to examine a number of hedging approaches and their impact on deal outcomes. I will show that averaging can be relatively efficient regardless of transaction size, but also that averaging’s benefits are positively correlated to deal size.

Crucially I use historic data to demonstrate that all-in cost probabilities can be quantified.

The Black-Scholes option pricing model transformed modern finance. Whereas prior to 1973 option prices could only be guesstimated, Black-Scholes presented a ground-breaking framework that birthed standardised pricing.

Coupled with the advent of the personal computer, Black-Scholes changed the manner and speed with which markets calculated risk. While arguments as to the limits of the model abound, elements of the original framework can be readily applied to advance our thinking in other domains.

In this piece I draw on the hotly contested efficient market hypothesis, which posits that market movements are essentially unpredictable, and might be thought of as a 50:50 hypothesis. I have often thought of it as simply that “markets are just as likely to go up, as they are to go down.”

As we shall see, while the hypothesis doesn’t perfectly hold, we can leverage it to assess the efficacy of different dealing execution strategies probabilistically. In this piece I use it to demonstrate that a carefully formulated execution strategy can minimise execution costs.

A market example

Let’s start by defining a simple scenario with key assumptions, of which I have chosen four:

As a hedger we are concerned about adverse market movements in the standard 3-year Australian dollar interest rate swap (IRS) market.

We are worried about adverse movements over the coming 3 months.

We have only two choices of how to execute our hedge:

a. At-Close Risk Cover - a single transaction executed at the end of three months, or

b. Progressive Risk Cover - transacting equal portions daily, accumulating in the outright exposure at the end of three months (i.e., approximately 1/60th hedged per day without exception).

All dealings are conducted at closing rates without execution costs.

I purposely chose the divergent forms of execution since they sit at extreme ends of the hedging spectrum. This is to highlight the importance of hedging strategy and the impact that deal size has on transaction costs.

For the sake of scenario framing, the following chart displays 3-year close-on-close swap yields from February 1991 until May 2023, which has been used in this analysis.

What becomes immediately obvious is that there has been a serial decline in yields (a generally rallying bond market) since 1991. We should remind ourselves that while historic outcomes don’t predict the future, the historic hedging outcomes show serial bias, and this has tended to favour swap payers.

Payers were favoured under At-Close Risk Cover ...

Under At-Close Risk Cover, the hedger is exposed to open market risk through the 3-month period, from initiation to close, with final cover being achieved only at the end-of-period closing price.

If the efficient market hypothesis held, we should expect a broadly 50:50 dispersion of favourable versus adverse outcomes, between payers and receivers.

However, as predicted, the long-term decline in 3-year yields within the dataset skews the outcome in favour of paying hedgers under the At-Close Risk Cover since 1991:

Payers, 53.46%

Receivers, 46.3%

Sum of favourable outcomes, 99.80%

Notice here that I have calculated the sum of favourable outcomes, which seems unnecessary. While this may seem superfluous the sum can be used to illustrate an important point and it gives us our results at base-100 which assists make our key point.

Notice, also, that in the case of At-Close-Cover the results do not precisely sum to 100%. This is because of 8,355 observations; a zero return was found on 17 occasions. On those dates neither payers or receivers obtained an advantage.

…. and Payers were likewise favoured under Progressive Risk Cover.

Under a Progressive Risk Cover model, it is assumed that it is possible to hedge the 3-month/3-year IRS risk at the mid-market daily close in equal daily proportions. This results in an ‘achieved transaction rate’ that is equal to the arithmetic mean of closing rates for sixty trading sessions.

The range of achieved rate outcomes (average rate minus initial rate) should still adhere to the efficient market hypothesis, that is: approximately 50:50 outcome split between payers and receivers.

Again, while our analysis uncovers a favourable bias for payers, it remains fairly close:

Payers 53.96%

Receivers 46.04%

Sum of favourable outcomes, 100.00%

And in this case the sum of favourable outcomes sums neatly to 100%.

What happens when we incorporate execution costs?

The two execution scenarios I have described here rely on the ability of hedgers to transact with perfect efficiency. That is: we’ve assumed hedging can be conducted at market-mid, which is obviously unrealistic.

So, what do we find in more realistic settings?

When transaction costs are included in our analysis, we find three things:

Favourable hedging outcomes are inversely related to transaction size under all execution approaches.

Progressive Risk Cover is more efficient than At-Close Risk Cover regardless of size,

The costs related to At-Close Risk Cover are positively correlated with increased transaction size, both nominally and relative to Progressive Risk Cover.

These findings will be unsurprising to market makers and those with deep markets experience. In fact, those who understand the nature of such costs will be right to ask, so what?

While we have proven the seemingly obvious, the point is:

The magnitude of transaction costs and their impact in large transactions, often fail to be quantitively defined for end users.

And yet there are few reasons for this lack of transparency.

While our experience in this domain would allow us to make reasonable transaction cost estimates, we have conducted soundings with market peers to arrive at indicative spreads.

The following graph collates these estimates of transaction costs and plots the impact they play on efficiency relative (based on 100 being perfectly efficient) to transaction size.

What does this show?

The difference in percentage-favourable results is quite stark.

· The blue line plots the percentage-favourable outcomes under Progressive Risk Cover,

· The red line plots the percentage under At-Close Risk Cover.

What we find is that under all deal size scenarios Progressive Risk Cover outperforms At-Close Risk Cover in terms of transaction costs. And as we noted, deal efficiencies decline as deal size grows for both approaches but maintains near-100 efficiency for Progressive.

Motive Asymmetry?

The field of behavioural finance is strewn with examples of the skewed perspectives found between those who seek to avoid risk and those who actively seek risk for profit. What should be clear is that regardless of motive, transaction costs can alter the standard efficiency paradigm no matter whether you are risk seeking or risk avoiding.

What should also be clear is that how you execute matters, and that the extent of that impact is magnified as deal size grows.

This makes specialist approaches to large or highly complex transactions a must, since a carefully formulated execution strategy can minimise both market risk and execution costs.

What next?

My next blog will focus on the risks associated with different execution approaches, again using progressive versus at-close scenarios and historic data quantitatively. This we will tie in with our work on premium illusion to demonstrate that there really is no such thing as a ‘free lunch’ when it comes to managing risk.

For those who would like to discuss the scenario, its outcomes, and/or the frameworks we use to quantify hedge-efficient approaches, please reach out at: info@martialis.com.au.

Term SOFR or not Term SOFR

My last paper made the case for the wider use of Term SOFR. My argument was based on the fact that the potential users of Term SOFR would only occupy approximately 1% of USD derivative turnover and would, therefore, hardly represent a systemic risk. Wider Term SOFR use, together with robust fallbacks, could significantly ease the operational risk and pressures on the end-users, i.e., the counterparties paying spreads to dealers.

On 21 April 2023, ARRC published ‘Summary and Update of the ARRC’s Term SOFR Scope of Use Best Practice Recommendations’ which reiterated and described their approach to the use of Term SOFR. The ARRC continues to recommend the restrictions on the use of Term SOFR which are reflected in the CME license agreement (CME is the administrator of the most commonly referenced Term SOFR).

The current restrictions will most likely continue to support the basis between Term SOFR and compounded SOFR, specifically Term SOFR is around 3 basis points above compounded SOFR for term (say 5 year) derivatives. This is because the restrictions encourage a one-way derivatives market where users can only pay Term SOFR but are restricted from receiving Term SOFR.

This paper looks at some alternatives to Term SOFR which may help end-users achieve the outcomes of Term SOFR without referencing Term SOFR and potentially offending the CME license conditions.

Let’s start with an example

Clients often have had loans linked to LIBOR and fixed debt issues swapped to LIBOR. The combination of floating and fixed liabilities has been managed using derivatives to the desired mix of LIBOR and fixed rates.

As assets are added or changed, the derivative market was a convenient and efficient way to trade into the desired exposure for the asset/liability balance. But this is about to change as USD LIBOR is discontinued from 30 June 2023. From July 2023 the USD market transition will force market users to alternate reference rates, including compounded SOFR, Term SOFR among others.

In the current system, a loan referencing Term SOFR can be hedged to a fixed rate using a derivative, so in this situation there is essentially no change from the situation faced under LIBOR.

However, using a derivative to swap a fixed rate debt issue to Term SOFR is not encouraged (ARRC recommendations) or permitted (CME license).

This is very clear from Scenario 7 in the ARRC publication reproduced below.

This is a significant change from the LIBOR experience.

The end-user may have a preference for Term SOFR referencing liabilities which is allowed via a loan but cannot be achieved by swapping a fixed rate debt issue to the same Term SOFR. The only way forward is to swap the fixed rate to compounded SOFR and run the basis risk between Term SOFR and compounded SOFR.

This is hardly ideal and potentially introduces new interest rate and operational risk.

Can you manage this risk using a basis swap from SOFR to Term SOFR?

The ARRC recommendations appear to allow this activity. Specifically, Scenario 8 shows the following transaction:

The accompanying commentary seems to imply this activity is permitted but the two scenarios below would not be in the spirit of the ARRC recommendations:

swap fixed coupons to compounded SOFR; then

swap compounded SOFR to Term SOFR (Scenario 8).

This does not appear to be permitted in the CME license as the Term SOFR risk is not embedded in a cash instrument, i.e., a loan.

So, the following arrangement of an end-user issuing fixed debt, receiving fixed/pay compounded SOFR and simultaneously receiving compounded SOFR/pay Term SOFR in a basis swap would not, in all likelihood, be allowed or, at the very least not be encouraged.

So, we appear to be left in a difficult situation where the end users may be forced to manage Term SOFR and compounded SOFR where previously they were only exposed to LIBOR.

Other ways forward for end-users

Many clients do not wish to manage the Term SOFR/compounded SOFR risk which they would acquire as part of a loan and fixed rate debt liability combination.

However, all is not lost. This could be managed with an active approach to the coupon dates of the debt and the calculation dates of the derivative.

Approach 1 – manage compounded SOFR to Term SOFR for a fixed debt issue:

Trade with the dealer as receive fixed/pay compounded SOFR (permitted) with terms and dates matching the debt issue.

Each rollover (coupon date), pay the USD OIS (1, 3 or 6-month as appropriate) to swap the compounded SOFR to a fixed rate to replicate Term SOFR.

While this approach achieves the desired outcome of fixing the SOFR rate for 1, 3 or 6-months, there are some challenges:

The operational risk of diarising and executing the USD OIS trades needs to be closely managed.

Term SOFR is calculated from rates across the CME trading day (see note below) and there may be slippage between Term SOFR, and the USD OIS rate traded on the day.

It is important to carefully match the settlement dates for each leg to ensure there is minimal impact on the cash management which could attract significant costs.

This approach is actually quite effective and could be a practical alternative to Term SOFR under circumstances where Term SOFR cannot be referenced.

Approach 2 – choose a point in time for your firm to fix the rate

In this approach, the firm decides on a specific time to transact the USD OIS and accepts there will likely be a difference from Term SOFR.

This is operationally much easier but can provide tracking errors if other components of the portfolio are referencing Term SOFR.

Term SOFR calculations and timing

Term SOFR is calculated in a very different way to the current USD LIBOR.

USD LIBOR is determined at a point in time, specifically 11 am London. If a firm were trying to replicate LIBOR, then trading at 11 am London in a market closely connected to LIBOR (e.g., a single period swap) would likely have little slippage.

However, Term SOFR is not calculated at a point in time.

Term SOFR is calculated as follows (CME description):

‘A set of Volume Weighted Average Prices (VWAP) are calculated using transaction prices observed during several observation intervals throughout the trading day. These are then used in a projection model to determine CME Term SOFR Reference Rates. Full details of the calculation methodology are available on the Term SOFR webpages.’

If you wish to replicate Term SOFR, you will need to trade a proportion of the USD OIS risk at each time CME accesses the price for the VWAP. This is made even more difficult because CME uses random times in each time bucket!

In practice, CME uses fourteen , 30-minute intervals with random time sampling which is not possible to exactly replicate without knowing the timing of each sample.

In practice, this makes it difficult to manage a USD OIS process to replace Term SOFR

USD OIS trades to replicate Term SOFR

Our analysis of USD OIS and Term SOFR since May 2019 (when Term SOFR was first published) gives some comfort that a practical approach could be found.

Example 1 - Trade half the USD OIS risk CME near market open and the other half near the close.

Average slippage is 1 basis point (bp).

Standard deviation is 4 bps.

Maximum is 26 bps.

Minimum is -22 bps.

The average and standard deviation are quite acceptable to many firms, but the outliers (maximum and minimum) are less attractive outcomes as the slippage is substantial.

The average slippage is within 2 standard deviations for 99.9% of time which may provide some comfort.

Example 2 – Performance over a 3-year quarterly swap traded each day.

Over the twelve rate fixes in a 3-year quarterly swap, the statistics are:

Average slippage is 2 bps.

Standard deviation is 1 bps.

Maximum is 4 bps.

Minimum is -1 bp.

The averaging process appears to be quite effective, with the maximum and minimum much reduced.

Over a 3-year swap, there may be some significant slippage days but, on average, the total outcome may be acceptable.

Summary

The recent ARRC announcements include recommendations which may allow end-users to hedge a wider group of Term SOFR exposures. But CME licensing still appears to restrict the use of Term SOFR to cash instruments and derivatives directly linked to those cash instruments.

Should the CME position change, firms could reconsider the Term SOFR use case.

In the meantime, there are practical and effective ways to replicate Term SOFR, some of which are described above.

But there are some risks and caveats:

Term SOFR is difficult to match exactly using USD OIS trades because of the timing and random nature of the Term SOFR calculation.

There can be slippage between USD OIS and Term SOFR which may cause tracking issues if parts of the portfolio reference Term SOFR.

There are operational aspects of trading USD OIS which need to be closely managed including date and settlement timing.

On the positive side:

The slippage appears to average out over time and across the rolls for a multi-roll swap.

A process could be put in place to manage the USD OIS trading and achieve quite acceptable rate fix and operational exposure.

In summary, if you need Term SOFR but are not able to access it for licensing reasons, there are alternatives.

How can Martialis assist?

Martialis can assist in this process by:

Designing appropriate operational procedures to manage the USD OIS trading and risk management;

Providing practical advice on establishing trading relationships;

Transacting and recording the USD OIS trades to ensure date and settlement matching;

Calculating any slippage to Term SOFR; and

Monitoring risks and pricing requirements.

While replicating Term SOFR appears to be complex, our experience shows this can be managed effectively and methodically if processes are robust and established proactively.

The Case for Wider Use of Term SOFR

In my last paper I looked at the trends in USD derivative turnover from BIS Triennial Surveys 2010 – 2022. In this paper I focus on the 2022 Survey and how it supports the wider use of Term SOFR than is currently permitted under existing use limits.

Many of our clients have concerns that SOFR is difficult to use compared with LIBOR. Most of their issues are related to operational problems, forward cash management and accounting calculations. LIBOR, as a forward-looking rate allows clients the time to manage their processes before settlement, whereas SOFR is a daily update which causes additional effort and forecasting. Term SOFR appears to be an easier transition as it shares many of the more desirable attributes of LIBOR.

Simply put, Term SOFR presents an easier transition from LIBOR than is compounded SOFR: CME’s own data tends to support this.

In the past I have looked at the use case for Term SOFR. Risk.net has published on this topic a few times in 2021, 2022 and 2023 outlining the various rules which are currently restricting the use of Term SOFR.

While many people, including myself, support the ARRC and Fed view that widespread use of Term SOFR may be problematic, I also believe that some easing of the restrictions may benefit end-users and not present systemic risks. This is supported by the Survey results as I explain below.

This paper looks at the 2022 BIS Triennial Survey for a breakdown of the users of SOFR and LIBOR. We can reasonably assume the LIBOR users will become SOFR users after 30 June 2023 (i.e., LIBOR cessation) so we can look at the total as a reasonable approximation of market turnover and user mix for SOFR.

Also, we could assume SOFR turnover is at or probably greater than in 2022 based on the trend in USD turnover to higher turnover over the past 10 years.

Firstly, let’s look at the product breakdown per participant grouping.

Turnover of USD derivatives by market participant groups

The Survey does provide some breakdown of the turnover of USD per market participant type. The trades are reported by Reporting Dealers and they separate their trades with other counterparties as follows:

Reporting Dealers – other banks reporting turnover;

Other Financial Institutions – financial institutions which are not Reporting Dealers (e.g., investment funds); and

Non-Financial customers – End users not included in the 2 groups above (e.g., corporates).

There may be derivative transactions between firms who are not Reporting Dealers: these trades would not be included in the Survey. Such trades could be between Other Financial Institutions so their market share may be even larger than that in the Survey.

The following chart shows the breakdown and the market percentage of each group.

The main points I see here are:

Overnight Index Swaps (SOFR) and LIBOR derivatives have comparable turnover.

Other Financial Institutions are the dominant payers with 80% of the total (SOFR + LIBOR) turnover.

Trading between Reporting Dealers is19% of market turnover and considerably less than the trading between Reporting Dealers and Other Financial Institutions.

Trading with Non-Financial customers is a minor part of market turnover and only represents 1% of the market.

Where is the turnover located?

USD is the largest derivative currency by turnover in the Survey as shown in the following chart.

Focusing on the USD, the turnover per country is varied as shown in the next chart.

USD derivatives are predominately traded in USA and UK with some turnover in other countries as well.

Conclusions from the Survey

The 2022 Survey is very clear that:

USD derivative trading is the largest by currency (44%).

The majority of that trading is in USA (68%) followed by UK (24%).

Trading between Reporting Dealers and Other Financial Institutions dominated the trading (80%).

Trading between Reporting Dealers and Non-Financial customers is a very minor component (1%).

As the USD derivatives markets, and presumably debt markets, move from LIBOR to SOFR, I reasonably expect the four points above to continue to be relevant.

How does this impact the use of Term SOFR?

The ARRC and Fed have reiterated their view that the use of Term SOFR should be restricted to a narrow range of products as described by Risk. The CME license terms for referencing Term SOFR reflect the ARRC recommendations and effectively prohibit using derivatives except between dealers to customers to hedge Term SOFR debt to a fixed rate.

The reasons provided by ARRC include to restrict the use of Term SOFR include:

avoiding a repeat of LIBOR with Term SOFR;

inter-dealer trading of Term SOFR could grow rapidly if permitted; and

trading Term SOFR could cannibalise trading SOFR itself.

The main fear is that easing restrictions on Term SOFR to allow for more use by end-users could unleash a torrent of inter-dealer and dealer to customer trading.

The 2022 Survey results do not appear to support this if trading Term SOFR had some restrictions to support dealer-customer and limited dealer-dealer trading.

The trading with end users in LIBOR (no restrictions and the vast majority of this trading based on my last paper) and/or SOFR (minimal in 2022) is only 1% of total market turnover in USD derivatives.

If all the LIBOR trading for Non-Financial customers is replaced by Term SOFR then it still only represents 1% of the market.

If interbank trading of Term SOFR was allowed (under certain restrictions) then it may also be around 1% of the market to clear offsetting risks between dealers.

So, even with a relatively unrestricted approach to allowing Reporting Dealers to trade with Non-Financial customers, the percentage of market turnover could be expected to be in the 1% – 2% range which unlikely to create a systemic problem if Term SOFR is discontinued sometime in the future.

Summary

The BIS 2022 Triennial Survey has many interesting features.

Among these is the interesting fact that trading between Reporting Dealers and Non-Financial customers is approximately 1% of market turnover in USD derivatives.

This has important implications for the use case for Term SOFR.

If trading in USD derivatives referencing Term SOFR is restricted to Non-Financial customers, then it is likely to be similarly around 1% of USD derivative turnover if all LIBOR and SOFR trading references Term SOFR.

This is not significant and would be unlikely to present systemic issues if Term SOFR was discontinued at some time.

Of course, contracts referencing Term SOFR would have fallbacks to accommodate a permanent cessation of Term SOFR.

I believe there is a good argument to allow wider use of Term SOFR for end users. A moderate relaxation of the CME licensing rules would allow a more balanced market (i.e., Term SOFR to fixed and fixed to Term SOFR derivatives) and address the reasonable concerns of the end users in the transition from LIBOR.

Bidding credit sensitivity adieu…

Credit sensitive benchmarks have been fundamental to corporate finance for many years. The loss of this sensitivity adds a systemic burden to deposit taking institutions. Why? Because corporate loan books no longer adequately reflect and compensate for the funding risk in the manner of the LIBOR-based system.

The magnitude of this mispricing depends on the extent to which corporate assets pervade bank balance sheets and the adjustment that bankers have made to lending margins. With banking sector credit risk returning to prominence recently, it is timely to look at this annoying, obscure, yet potentially impactful problem.

Our analysis concludes that while US banking market capitalisation has notably rebounded from GFC lows and appears capable of withstanding a major credit induced event; post-Libor risk-free rates may not adequately reflect the risk undertaken by lenders. This potential interest forgone is of a material magnitude.

Hypothetical Interest Forgone under SOFA during the GFC

We described some important work done by Professor Urban Jermann in our post of August 2022.

Professor Urban is Safra Professor of International Finance and Capital Markets at the Wharton School of the University of Pennsylvania, and we showcased his major work from 2021:

Interest Received by Banks during the Financial Crisis: LIBOR vs Hypothetical SOFR Loans.

This estimated the amount of interest that would likely have been forgone by US banks had US business loans been indexed to SOFR during the GFC:

“The cumulative additional interest from LIBOR during the crisis is estimated to be between 1% to 2% of the notional amount of outstanding loans, depending on the tenor and type of SOFR rate used”.

With cumulative interest forgone estimated at:

U$32.1 billion if loans had instead followed compounded SOFR; or

U$25.0 billion had they followed Term SOFR

To recap, these numbers represent the hypothetical interest income foregone if corporate facilities had been indexed against the major SOFR variants over the period 1st July 2007 and 30th June 2009.

To contextualise the GFC moves, 3m LIBOR versus 3m SOFR Overnight Index Swap (OIS) rates are plotted on the following graph. This credit sensitivity proxy is generally known as the LOIS spread.

The LOIS spread averaged 10.7 basis points for the five years prior to July 2007. This average LOIS spread rose to 89.1 basis points through the GFC, as defined by Professor Jermann.

A non-trivial amount

In a follow-up article in Knowledge at Wharton, editor-writer Shankar Parameshwaran highlights what Professor Jermann was driving at:

“The $30 billion in interest income due to the credit sensitivity of LIBOR is not a trivial amount”.

Inviting hurried back-of-the-envelope calculations, Parameshwaran calculates that:

“On March 6th, 2009, when bank share prices tanked, the top 20 commercial banks from 2007 had a combined market capitalization of $204 billion.”

According to NYU-Stern School of Business, forward price-earnings ratios for money center banks today sit at around 9x earnings.

Those wanting to interpolate what might have been should take care to note that Professor Jermann’s calculations were for hypothetical interest foregone over two years, whereas P/E ratios are based on annualised earnings measures.

Nonetheless, sector annualised interest forgone of between $12 and $17 billion (i.e., halving Professor Urban’s numbers) in an environment where stocks are trading on 9x multiples is very worrying, especially considering the sector market cap of only $204 billion.

2023 – What of the situation today?

Taking Professor Urban’s raw calculations and assumptions and applying sector asset growth, US banks across 2023/24 would likely forgo:

U$59.4 billion if loans follow compounded SOFR; or

U$46.3 billion if loans follow Term SOFR

This is a simple estimate if the credit moves of the GFC period are replicated in the coming two-year period; but system risk appears much lower given the expansive sector market caps.

For the sake of comparison, the market capitalisation of the 20 largest financials in the US sits today at around U$1.54 trillion at mid-March 2023 by Martialis calculations (U$1,541.29 billion to be precise). This represents an impressive rebound and growth of 755% since the height of the GFC.

Corporate lending has grown far less quickly.

According to the St Louis FED, total financial assets of the domestic US financial sectors grew only 85% over the corresponding period (a surprisingly large lag). For the sake of framing, it’s worth noting that the US economy is only a third larger than March 2009 in terms of annualised real GDP, so we’re within reasonable ballpark.

This suggests that the system could handle GFC like conditions, but that the interest likely forgone if GFC-like conditions re-emerge, is still quite material.

What of the latest credit stress event?

To simplify how we look at credit stress we’re starting to favour Invesco/SOFR Academy USD Across-the-Curve Credit Spread Indexes, known more generally by their acronym ‘AXI.’

AXI is starting to gain interest given its constituent make-up and methodology, and we like the clean picture of credit sensitivity it provides in USD:

AXI is a weighted average of the credit spreads of unsecured US bank funding transactions with maturities ranging from overnight to five years, with weights that reflect both transaction volumes and issuances.

AXI can be added to Term SOFR (or other SOFR variants) to form a credit-sensitive interest rate benchmark for loans, derivatives, or other products.

The historic picture of AXI across 1m, 3m, and 6-month tenors from 2018 is as follows:

Credit sensitivity is highlighted over the period of COVID market stress and more recently as bank funding costs have risen with the Silicon Valley Bank and Credit Suisse events of early 2023.

For those interested in further AXI resources, please refer to:

How is AXI tracking the current stress?

Here I compare 3-month AXI with 3-month LOIS (LIBOR-OIS) over an analogue period, starting 90-days prior to the largest jump above one standard deviation in LOIS from 2007, which occurred on 9th August 2007.

While the base of AXI commences somewhat higher than LOIS, at +19.3 versus +8.8 basis points in the ninety days to Day-0 (identified by the dotted red line), the credit sensitivity of the subsequent period shows remarkable similarities at the start of both periods of credit deterioration.

Conclusions

What is clear is that despite the move to risk-free rates (RFRs), rational investors remain rational; demanding higher risk premiums to compensate for the risk of funding banks.

What’s less clear is the extent to which banks are able to pass-on a higher cost of funds to cover their various assets; and this is a systemic problem.

While higher rates are almost uniformly beneficial across mortgage and smaller variable finance segments, it’s not clear how banks compensate for the absence of LIBOR-like credit sensitivity in their corporate assets.

With these points in mind, we encourage bankers to ask three questions:

How long will banking sector credit remain elevated?

Are we receiving sufficient compensation for corporate lending in a risk-free-rate world?

Should corporate loan margins be recalibrated accordingly?

Widespread failure to address these seems to us to have rather obvious consequences.

The Triennial BIS Survey – USD Derivatives

Every three years I eagerly await the BIS Triennial Survey as it rarely fails to surprise. The 2022 Survey was announced in October 2022 and I have been remiss in not looking into the details of the data.

Hidden in the tables are many interesting facts which correct the market thinking on the state of the FX and derivatives markets, the trends over many years and potentially what to look forward to in the future.

This paper is the first of a series on the 2022 Survey and looks at looks at USD derivatives as was a comparison across the 2010 to 2022 Surveys. I will look more carefully at the 2022 Survey for USD next blog but this will start the process of a longer series on the derivatives markets.

I plan to look at the top 4 currencies (USD, EUR, GBP and AUD) as well as the total market over the next papers.

The USD derivatives market has seen strong growth in average daily turnover (blue line) since the 2007 (i.e., the 2010 Survey which uses data from 2007 – 2010). In fact, the turnover has increased by over 7 times from around 300,000 million to 2,200,000 million per day.

While this is impressive growth, it has not been equal for all market participants.

The Reporting Dealers (orange) have had a moderate decrease in the percentage of the total from 33% to 17% now.

The Other Financials (grey) have increased their share from 54% to 80%.

The Non-Financials (yellow) were never a major component of the turnover but have decreased from a high of 20% in 2013 to around 1% now.

The growth story - Other financials

The growth story (I think unsurprisingly) is the Other Financials, i.e., those who are non-reporting financial firms and typically non-banks.

This group dominates the market with around 80% share of both LIBOR and SOFR markets in the 2022 Survey as shown in the following chart.

This group has grown with the SOFR and LIBOR markets and has largely crowded out other market participant and now represents around 80% of market turnover.

Since 2010, the Other Financials have been well over 50% of the market and have represented the largest group in all the Surveys since 2010. Note that the separate reporting of SOFR started in 2019 and this group has been just as active in SOFR as in LIBOR.

Falling involvement - non-financials

If I then look at the Non-Financials only and compare the percentages of the LIBOR and SOFR markets, the decline of market share for this group is clear in the following chart.

In the Surveys prior to 2019 (when SOFR swaps derivatives were not separately reported), the Non-Financials were not major participants in derivatives. Since 2016, the share of the total (LIBOR and SOFR) has declined.

Since 2019, the share of both LIBOR and SOFR has declined similarly. The Non-Financials appear to be a very small component of the overall derivatives markets in USD.

What could be causing the fall in the Non-Financial percentage?

While it is not clear what caused this decline in percentage, one thought was the interest rate environment.

The following chart shows the Non-Financial percentage and the USD 3-month LIBOR and the USD 5-year LIBOR swap rates. This is to ‘test’ whether the percentage is impacted by the direct or outright short term (LIBOR) or longer-term (5-year swap) rates.

There is no obvious connection between the direction or level of LIBOR/5-tear swap and the percentage for Non-Financials. While the percentage did rise from 2010 to 2016 which corresponded with the fall in interest rates, this was not repeated in the 2019 – 2022 falls in interest rates.

The actual turnover for Non-Financials have been falling as well as the percentage (see the first chart).

Something is happening over the most recent Surveys which indicates the Non-Financials are a relatively small component of the USD derivatives market.

Summary

The trends in the USD derivatives markets can be observed over many years using the BIS Triennial Surveys.

Since the 2010 Survey:

The Other Financials have continued to dominate the USD derivatives market turnover and now represent approximately 80% of the market.

The Reporting Dealers are a declining percentage of the market and now represent approximately 19% of the turnover.

The Non-Financials are showing a multi-year decline in percentage and are now around 1% of the market.

As the USD market transitions to SOFR in its various forms (Term SOFR, compounded and averages) the main users will adopt a standard form of SOFR. The LIBOR reporting will disappear and be replaced by SOFR.

I expect the Other Financials to continue their dominance of the market turnover and potentially increase their share over the next 3 years.

Non-Financials are still a mystery play; will they remain at very low growth levels of turnover or will they return to the markets as rates rise and/or increase in volatility? Will they also adopt SOFR and/or Term SOFR to replace LIBOR or simply hedge in other ways?

My next blog will look further into the USD 2022 Survey for any hints as to how the USD derivatives markets may evolve in the near future.

Term rates are crucial market infrastructure

Late in 2022 the Canadian Alternative Reference Rate working group (CARR) announced it would accede to market pressure and develop a Term-CORRA interest rate benchmark.

Somewhat unusually, CARR’s announcement was made prior to release of summary responses to their consultation on a potential new term rate. This was released on January 23rd.

Leaving aside the unusual delay, it is instructive to review the summary of the consultation’s responses. As I hope to explain, survey responses to regulatory surveys such as these give us important insights into the financial infrastructure requirements of a modern economy.

The market demand for Term-CORRA is telling. It tells us that Term Rates are crucial market infrastructure, not just a addition.

Recapping CDOR’s demise

We took a look at Canadian benchmark reform last year, see here, but to recap, the principal elements within Canadian benchmark reform are:

The mid-2024 cessation of Canadian Dollar Offered Rate, CDOR, the primary interest rate benchmark in Canada since market inception, with the proposed replacement rate being:

The Canadian Overnight Repo Rate Average, CORRA.

CORRA is Canada’s official risk-free rate based on daily transaction-level data on repo trades. These measure “the cost of overnight general collateral funding in Canadian dollars using Government of Canada treasury bills and bonds as collateral for repurchase transactions,” and is thus quite similar to USD-SOFR.

Similar to the approach taken in both the UK and US, and mirrored elsewhere, CARR has published its own well-laid transition roadmap to guide participants:

Source: https://www.bankofcanada.ca/wp-content/uploads/2022/05/transition-roadmap.pdf

What had been lacking from the Canadian plan was the development of a term rate similar to Term-SONIA and Term-SOFR.

Respondents emphatic call for Term-CORRA

To address the absence of a term rate solution, on May 16th CARR surveyed Canadian market participants to “seek feedback on the need for a potential forward-looking term rate (i.e. Term CORRA) to replace CDOR in certain loan and hedging agreements.?”

The survey responses were emphatic and instructive, for example:

Question 1) Does your institution need a Term CORRA rate?

All non-financial firms “wanted a Term CORRA benchmark”.

As did a majority of financial firms.

Overall, a clear majority (37 of 42 respondents) supported its creation.

Which to our mind is as emphatic a statement of end-user demand as any consult on this topic we have seen, clearly prompting CARR’s response as announced in October:

‘In response to the overwhelming support for a Term CORRA, CARR members agree to try to develop a Term CORRA, so long as a robust and IOSCO compliant rate can be created’, my emphasis added.

However, it was the feedback received on why firms felt they needed Term-CORRA that was most instructive.

To help summarise the feedback, I have bracketed the stated respondent reasoning into two areas:

1. Functional/Operational Reasoning:

cash flow predictability, including the need for accurate cash flow forecasting given hedge accounting considerations;

operational simplicity, thus obviating the need for treasury system overhauls, and reducing operational burdens on staff, particularly among smaller firms;

reducing the liquidity risk where a significant change in interest rates were to occur towards the end of an interest-period, firms may have difficulty acquiring adequate cash to meet interest by the due date; and

as a market basis for discount calculations where a present value is needed (e.g., financial reporting).

2. Commercial/Product Reasoning:

Non-financial companies noted:

hedging loan facilities (e.g., for derivatives products to hedge term SOFR-denominated USD borrowings to a CAD term equivalent) and other term rate exposures;

transfer pricing for inter-company loans;

as a reference rate when negotiating contracts with third parties (e.g., vendors, JV partners, customers) or related entities (e.g., partnership loans);

as a rate for inventory/receivables financing;

securitization products with floating rate tranches (asset-matching); and

financial leases.

Financial companies noted:

clients’ hedging activity (i.e., where firms require hedges for Term CORRA interest rate swaps, caps and floors based on the same benchmark);

derivative products, including the hedging of Term CORRA derivatives in the inter-dealer market (as US banks offering Term SOFR products are facing substantial issues managing the associated risks);

securitisations of Term CORRA-based lending; and

where operational constraints on some of the parties to the contract limit their ability to use overnight rates.

To which we are inclined to add:

Sharia-compliant products fundamentally require forward-looking rates (i.e., to establish rates of profit in-advance);

import/export financings of capital projects, in order to forecast cash flows or arrange outgoing foreign currency denominated payments; and

trade and commodity prepayments, for a range of calculations that by definition require forward-looking rates.

Which are all reasons why Term-RFR benchmarks can’t not exist…

We have delved into the topic of Term-RFR rates from several dimensions over the past year:

All of which have served to buttress our view that term rates simply can’t not exist in post-LIBOR finance; they are fundamental to the proper working of whole industry segments.

Taking this further, we see the proper evolution of term rates (bother in RFR and credit sensitive formats) as a desirable goal for the global regulatory family, particularly given trade and capital linkages between jurisdictions.

Then there’s the question of risk dispersion

As the CARR consult respondents noted, Canadian financial respondents wanted the ability to access an inter-dealer market:

Derivative products, including the hedging of Term CORRA derivatives in the inter-dealer market (as US banks offering Term SOFR products are facing substantial issues managing the associated risks) – my emphasis again.

Our evolving view is that while use-case limits are a not unreasonable consideration, they are a) likely unnecessary, and b) possibly responsible for a build-up of essentially un-hedgeable basis risk in dealer swap books that cannot be a positive for financial stability.

And understanding the Use-Case Limits

As I explored last year in Term RFR use limits; what use are they?, if use-case limits are here to stay, firms should start considering the use-case environment and their response quite carefully:

Ensure that use-case controls prevent dealing activity that contravenes regulator or industry preferences, and/or licensing requirements.

Establish a rules-based exceptions mechanism for allowance of Term-RFR use where use is warranted, and processes that document and track artefacts where use-case exemptions are approved.

Understand the peculiar reset risk that exists where Term-RFR’s are hedged via traditional OIS products.

Define and tag Term-RFR products as such, including within risk systems where unexpected basis and reset risk can emerge (between Term-RFR and traditional OIS hedges).

Ensure key staff understand term rates, their role in finance, their use-case limits, particularly where such staff are customer facing.

For Canadian-dollar risk, we would add that it will be important to understand the subtle variation that CARR has flagged already:

This appears to open up the possibility that a Canadian term rate could trade in interdealer markets, though how that might be ‘policed’ is another matter.

To our mind it would be better if the wish list of CARR’s Canadian respondents were met fulsomely, and preferably with a generous relaxation of use-case limits – a topic which we intend to explore in greater detail through 2023.

Summing up

Canada continues to surprise markets with the evolution of CORRA, and now a Term-CORRA benchmark solution. This is in a helpful alignment to developments in the US, where CME Term-SOFR activity continues to develop apace.

Other jurisdictions should be thinking about the market infrastructure developments that the Canadians see as crucial building blocks for finance and financial markets in an IBOR world.

From where we sit it really is hats off to the Bank of Canada and their Canadian Alternative Reference Rate Working Group.

Challenges in using SOFR for all loans

Bank funding risks

Many of our clients are asking about the impact of using risk free rates such as SOFR and SONIA in loan products which allow for discretionary drawdowns. This is especially challenging in the case of revolving credit facilities and particularly those with multi-currency options.

The choices of when, how much and which currency a bank can allow a borrower client to draw down in certain products has always been a challenge to manage. For example, in times of significant stress (e.g., GFC and COVID) the clients can suddenly draw cash from revolving facilities which can create liquidity and pricing problems for the banks.

In the past, the pricing of these facilities was somewhat easier because the reference rates were intrinsically linked to credit-sensitive benchmarks such as LIBOR. When liquidity and credit was stressed, LIBOR typically rose faster than Fed Funds (i.e., the TED spread increased) and the pricing of the loan facilities reflected the increased cost for the banks. This was automatically transferred (in the most part) to the borrower as the reference rate (LIBOR) closely tracked the bank’s borrowing rate.

This affected the bank profitability, the cost of the loans based on that expected cost/return and the behaviour of the borrowers. Banks could reasonably accurately price the facility based on expected costs (additional spread) and borrower drawdowns (expected liquidity requirements) and so were generally prepared to offer competitively priced products to clients.

The recent paper published on 22 December 2022 on the Federal Reserve of New York site and authored by Harry Cooperman, Darrell Duffie, Stephan Luck, Zachry Wang, and Yilin (David) Yang looks at the possible costs and therefore pricing challenges for banks when using SOFR rather than LIBOR for certain loans.

For those whose holiday calendar resulted in them missing this important paper, I really urge you to read the full transcript. In the meantime, I will outline some of the main points and my view of how these may impact banks and their clients.

One word of caution: the authors do note that the paper does not necessarily represent the views of the NY Fed or the Federal Reserve.

Bank Funding Risk, Reference Rates, and Credit Supply – Federal Reserve of New York – 22 December 2022

The paper references some very interesting data and does some really great analysis. The work focusses on the revolving credit loans that give borrowers the option to draw funds up to the credit limit at any time under agreed terms and pricing.

These credit facilities are widely offered by banks and are often used by their clients to guarantee funding for short periods of time even when liquidity conditions in the broader market may be challenging. It is this optionality and the very real likelihood that clients will require the funds at short notice in difficult markets that dictates the terms and pricing of the facilities.

The facilities tended to use credit-sensitive reference rates (e.g., LIBOR) which reflect the actual borrowing rates for the banks at a point in time. In this case, the underlying market conditions are automatically included in the LIBOR pricing for the clients and the banks can offer these products at competitive prices and terms.

The authors look at the impact of replacing LIBOR with risk free rates such as SOFR. They run some simulations for GFC (2008) and COVID (2020) and compare the performance of the products (LIBOR plus a fixed credit spread versus SOFR plus a fixed credit spread).

Without the credit sensitivity (i.e., using SOFR), the banks would be very likely to have a lower margin (NII – Net Interest Income). This was particularly evident in GFC (-6.48 billion) while the COVID experience was lower (-1.59 billion).

This is demonstrated in the following chart used by Ross Beaney previously.

These results can be found in Section D of the paper – Accounting Counterfactual Assumptions & Additional Results, Appendix D.

Why does this matter?

The authors conclude that the choice of reference rate (LIBOR or SOFR) affects the supply of revolving credit lines.

Under LIBOR referencing facilities, the bank and the client share the embedded liquidity risk. As the market supply of funds decreases, the cost increases (i.e., LIBOR rises relative to Fed Funds) are largely passed on to the borrower. The lender (the bank) still retains some risk as their individual ability to borrow funds from the market may be impacted by their own credit compared with other banks and this may diverge from LIBOR.

Point 1

This could result in the banks increasing the pricing for revolving credit facilities linked to SOFR or restricting the supply of these products. Because the risk is now firmly with the bank, the pricing and supply must reflect a ‘worst case’ scenario where the bank has limited ability to borrow from markets and/or an increased cost.

Note that this is not such a major issue for standard, term loans. These products can be term funded at a known margin and do not have the optionality for drawdown. In this case, there is little or no uncertainty about the principal and timing of the drawdown and repayment of the loan.

The authors do not consider multi-currency revolving credit facilities in their work. In my experience, the multi-currency option creates even more issues for banks and their clients. If you use a credit sensitive reference rates for the optionality within one currency (e.g., AUD BBSW) and a risk-free reference rate for another currency (e.g., USD SOFR), then under certain market conditions, one alternative could be far better than another for the borrower. For example, with a fixed spread to SOFR, if the actual market rate is above SOFR plus the fixed spread, then the rational borrower would logically opt for the USD.

Point 2

Multi-currency revolving credit facilities present additional problems for pricing and supply of the product. A bank must reasonably use the worst-case spread for a risk-free rate or risk being drawn on the facility when liquidity spreads exceed the fixed spread in one or more currencies referenced in the facility.

Is there another way to resolve this?

Fortunately, several credit-sensitive alternatives exist which could be used to replace LIBOR and be used with or instead of SOFR. We have previously written on this subject here, here, and here.

In the USD market these include:

Across the curve Spread Indices – SOFR Academy and Invesco

Bloomberg Short-Term Bank Yield

Credit Inclusive Term Spread/Credit Inclusive Term Rate – S&P Global – not yet available for licensing.

Published by AFX

I will not describe each of these alternatives, but the links are provided for further information if you are not already familiar with the reference rates. In all cases, they have reasonably tracked LIBOR in the past and add back a level of credit sensitivity.

If Messrs Cooperman, Duffie, Luck, Wang, and Yang are correct in their conclusion that SOFR-linked revolving credit facilities may be affected (I.e., negatively compared with the outgoing LIBOR equivalents), using the newer credit-sensitive rates above may help restore the risk balance. This may allow the banks to continue to offer these products as they do now.

Summary

The 22/12/2022 paper (and I appreciate the alliteration!) highlighted some particularly important challenges in the transition from LIBOR to SOFR for revolving credit facilities. The authors rightly point out that pricing and supply of these facilities may be negatively impacted.

While they did not look at multi-currency facilities, these present even more problems for banks who now provide these to clients.

Many end-user borrowers have such facilities to ensure they can have liquidity available under all circumstances. They may be expensive but are essential components of good risk management for many corporate and investor firms.

If the supply and/or price of these products is negatively impacted, there is a real risk that the end-users may face increased risk to liquidity crises in the future.

ESG maturing, far from settled…

We have been asked on several occasions whether we believe ESG-Investing has reached a state of reasonable maturity in capital and financial markets?

On each occasion I have proffered a rather hurried and wholly inadequate answer in the negative. In this blog I attempt to address this by cataloguing evidence of where greater maturity and/or standardisation is needed.

By way of reminder, Martialis takes no sides in the question of whether ESG investing adds value. If there is a value-assessment debate it is for others to determine, though we view the ultimate goals as laudable.

What follows should not be considered complete. While I have attempted to filter objectively, the starting point for the catalogue is inevitably opinion-based, or based on our experiences, and as usual – everything is contestable.

Some fundamentals

Let me start by making two general observations on the question of whether matters-ESG are ‘settled.’ This is a somewhat different question to whether they are, as yet, mature.

Firstly, modern investing owes much to the earliest open-air markets that started to evolve in and around the Warmoesstraat in Amsterdam in the late 15th Century. In their seven hundred-plus years evolution various approaches to investing have advanced and diversified, but never settled. Hence, at this relatively early stage, we should expect the ESG-investing domain to likewise advance and potentially diversify over time.

Secondly, while the world’s capital markets are truly enormous, it’s not clear whether there are sufficient ESG-rated securities to meet demand at any point. For example: if the world’s savings pool were directed entirely at ESG-rated assets above a certain score, their availability would be an obvious limitation. This is also food for thought for those who might be concerned at prospective concentration and/or asset hoarding risk (a topic for another day.

With this aside, I focus on reasonably objective areas that demonstrate that more mature ESG investing environment remains ahead of us.

The catalogue

John Feeney’s recent blog underscored the benefits of industry standardisation in benchmark setting, noting that:

“Markets depend on a level of benchmark standardisation that makes each dealer and end-user confident of the performance and valuation of each product.”

And:

“Most deep and liquid markets depend on a standard benchmark for risk resetting which is widely available and used in the majority of traded products.”

While John was pointing to the benefits across traded products, I think it is reasonable to extend these contentions to global finance more generally.

What we know is that in domains such as, say, transport, standardisation that turned cargo freight into uniform cargo in the form of ISO-standardised containers and pallets has driven incredible efficiencies. We can also agree that in financial markets high degrees of homogeneity have dramatically improved the efficient movement of capital between economic agents.

Thus, the catalogue that follows leans heavily on our enterprise view of the attractiveness, benefits, and likely efficiency-gains of adopting highly standardised and transparent approaches in markets:

ESG Ratings

Whereas the credit rating domain settled around a group of core agencies with well-understood approaches and ratings actions, the ESG ratings space continues to evolve.

As John noted, ESG evaluation criteria vary between multiple different rating platforms and are typically not independently verified, thus there is “no existing robust and standardised measure of ESG which captures a wide range of inputs and could be classified as a financial benchmark.”

Separately, it’s reasonably clear that ESG ratings are themselves an emerging specialisation, evidenced most recently in the unfortunately high ratings achieved by FTX on governance measures by a prominent ESG ratings firm.

Investment managers should note that ratings and ratings standards are neither fixed, nor a one-way bet.

2. Pricing (particularly sustainability premium or ‘greenium’)

We would normally view pricing as the rather obvious interaction between buyers and sellers known as price discovery in transparent markets, but this is a feature of mature markets. In less mature settings the pricing of individual deals may be shrouded by ‘tailored estimation’ (in the absence of an observable markets), and price discovery may be problematic given the one-sided nature of demand.

And this appears to be the case with ESG deal price-setting.

We note that in a recent ISDA survey, The Way Forward for Sustainability-linked Derivatives, the association asked members how ESG premiums are determined. Of 69 survey respondents a clear majority (45) indicated they “did not know how these premiums are determined.” ISDA also referred to the SLD market (sustainability linked derivatives market) as being “nascent” and described the sustainability premium or “greenium” as a “new concept in derivatives trading.”

These are obvious features of illiquid or partially formed markets such as those found in the price of highly complex derivatives.

3. Primacy

Corporate finance valuations have generally advanced down return or risk-compensated return dominant pathways. This was the logical advance of finance theory driven by advances in thinking around CAPM models and the like, aided by return-based concepts such as RoIC, RoCE, and RoE and broader economy concepts such as those found in the macroeconomics field.

While the layering of ESG filters within investment processes can take many forms, the question of ESG primacy arises. At what point should ESG filters be applied? Is there a fixed line, or some flexibility? What of exceptions? Should ESG factors take precedence, before traditional valuation approaches are applied?

We note that there are a variety of approaches being taken among clients, and other investment entities with whom we are close. Few are attempting a strict Blackrock ETF-like approach, though all have found themselves under pressure to respond in some fashion.

4. Portfolio Construction

Portfolio construction and asset allocations are considered by many to be at the heart of investment management performance.

Linked to the question of ESG-primacy is the question of whether a filtering process (particularly very strict approaches) may have unintended consequences in terms of optimal portfolio construction?

This is an emerging yet important topic. Is a traditionally risk-efficient portfolio, one suited to one or more beneficiaries under traditional allocation approaches, corrupted when ESG filters are applied (particularly if stringent filters remove whole sectors from consideration)?

There are a range of views on this, and I do not propose to dig into them here, however, we note that ESG scores for certain investable sectors are more readily achieved than in some others. At a minimum, we would expect this to have a bearing on portfolio concentration (and this may have played-out across the sweeping return-themes of 2022, in the dramatically skewed returns to energy sectors compared with new-economy stocks).

5. Emerging Standards

Perhaps the greatest area driving ESG towards maturity at present is that of the impending transparency, particularly in the sustainable finance edge of ESG. We see this as being driven by a range of government and regulatory agents.

There are simply too many global initiatives in-train to mention at present, but by way of example:

Australia - National Sustainable Finance Strategy,

We view these as likely to shape and enhance ESG maturity by bringing a degree of standardisation, but this will take time.

In this sense such initiatives are to be welcomed, but they are not yet embedded or systematically applied. They are also occurring on a multi-jurisdictional basis, and though we can acknowledge the work of the UN, there appears to be only vague international coordination.

We urge investment managers to watch these developments closely, since differing or changing standards can have a bearing on portfolio composition considerations.

6. Fiduciary Risk

We covered this topic in my blog of November 9th; ESG & Mandate Risk, which received reasonable interest and viewership. Judging by the number of follow-up engagements on the topic we expect the fiduciary question to linger.

Opinions certainly vary among readers as to whether fiduciary risk rises or falls away, but this itself is a sign that the question of fiduciary responsibility is not entirely settled. It may also be prone to shifting political sands on a jurisdictional basis (down to state level in the US as one example).

More recently, we have seen additional thought pieces on this topic appear, for example, Does ESG investing have a problem with fiduciary duty?, and related news that demonstrates there is a distance to travel before maturity is reached:

We continue to assess the various risks within this space.

Summing up

To sum up, we have been taking stock of the ESG domain for considerable time and have had several interesting client engagements on the topic. Much of what I have expressed here has been driven by such engagements, which have been highly productive and somewhat illuminating.

Our role is always to consider what is happening and be in a position to help inform decision-makers as their navigational needs arise, and as they ask where they should be positioned as events unfold To this end, it is helpful to be challenged on any topic, but on the question of how mature the ESG domain is for investment managers this has been very much the case, and we expect the challenges to continue.

While we are inclined to point out that there is a potentially long way to go, we can at least note that ESG investing is maturing but not yet settled.

As always in finance, some complexity remains, and market participants will have to keep adjusting.

Trading ESG Risk

Deep and liquid traded markets

Many financial risks can be acquired or modified through trading of securities and/or derivatives. For example, derivative products related to interest rates have been traded for many years and has seen the considerable growth of markets to shift risk from firm to firm. An active market to trade the risk has enhanced the ability of investors and borrowers to settle on the type and amount of risk best suited to their needs.

Another example is equity risk which also have deep and tradable markets. In this case, derivatives often reference an index such as Dow, S&P500 and NASDAQ which allow participants to trade the general direction of the market or alternatively trade sectors or even individual names. In each case, the underlying floating rate or index is clear and readily referenced to benchmark the trade.

Markets depend on a level of benchmark standardisation that makes each dealer and end-user confident of the performance and valuation of each product. Even the much-maligned LIBOR played a pivotal part in the development of traded interest rate markets. Without a standardised measure for risk setting such as LIBOR, derivative markets, for example, would have been impossible to trade in such a simple and definable way. And as LIBOR was replaced by Risk Free Rates such as SOFR and SONIA, the traded markets have adapted and continued to grow.

Likewise, equity markets have developed effective benchmarks for pricing in markets and allow for efficient risk transfer.

Most deep and liquid markets depend on a standard benchmark for risk resetting which is widely available and used in the majority of traded products.

The ESG markets – the next frontier

The ESG markets do not, at present, have the ability to trade the ESG risk in an equivalent way to interest rate or equity risk. There is no inter-dealer ESG derivative market and no standardised rate or benchmark to reference in a similar way to interest rates or equities.

A few firms do produce ‘ESG Scores’ which are not, technically, benchmarks. These include:

rating agencies such as S&P, Moody’s and Fitch;

Data providers such as Bloomberg and Refinitiv; and

Others such as ISS, MSCI, Datalytics etc.

While these agencies and vendors produce a ‘score’ from publicly available data (such as annual reports from companies) they are quite clear that these are not independently verified. In this sense, they are not benchmarks and could not be used under the regulatory requirements of many jurisdictions for the purposes of a benchmark, I.e., typically defined as refixing a variable rate or valuing a security.

So, there is no existing robust and standardised measure of ESG which captures a wide range of inputs and could be classified as a financial benchmark.

Why does the lack of a benchmark matter

If you have a risk or a desire to trade a financial product, you usually look at a screen where the bids and offers are posted for the products in which you have an interest. The products have standards and definitions which are supported by contracts and documentation such as that provided by ISDA for derivatives.

Whether it is a swap for fixed against floating or a fixed rate security, there is a need for an index or benchmark to provide the floating side of the trade and/or the valuation of a security. This is at the very heart of ‘price discovery;’ itself an important efficiency-driver.

It is particularly useful to use a standardised benchmark for obvious reasons. Once the benchmark is defined and readily available then there is a consequent reduction in the complexity of the trading because everyone is referencing the same rate or index.

Without a standardised benchmark, ESG products are difficult (I.e., near impossible) to trade in the inter-dealer market which means everyone simply builds up risk with no effective way to trade this into a market where the other side may be found.

One-sided or two-sided markets if an ESG benchmark can be developed

There is a market view that any ESG market would only be a one-sided (i.e., everyone wants to receive ‘fixed’ and pay ‘floating’ ESG). It is likely the result of the rush into ESG exposure and the perceived lack of floating rate investments that seems to drive this argument.

However, I take a slightly different view. Let’s take the example of a company with a debt linked to ESG performance. These have been transacted where the margins on the fixed or floating debt reduces as ESG performance improves (however that is measured!).

In this case, if the company had assets with fixed returns, then they may be a natural fixed rate payer of the derivative to match the asset risk to the liability risk. So why have ESG linked debt? Well, investor demand may be such that ESG debt represents cheaper funding, but it needs to be swapped for better risk management.

The investor argument is also important. Not every fund is ESG focussed, and some investors may actually need additional non-ESG exposure if they can only acquire assets with ESG links in the names they need for diversification.

I am a believer in traded market efficiency. If there is a market which is clear and standardised, a basis may form but equally the arbitrageurs will move in if that basis is unfounded. Price discovery is fundamental to their work.

Summary

The ESG market is growing and evolving as borrowers and investors respond to changes in demand. The current products are generally customised and structured for individual needs and are therefore not easily tradeable.

For deep and liquid markets to develop, there will need to be considerable development of standards and documentation for products (see ISDA survey) and credible benchmarks to support the products. While there are some ‘scores’ available there are no robust benchmarks to apply to products.

Along with the products for borrowers and investors, a supporting derivative market is essential to allow firms an efficient way to move and diversify the risk. A derivatives market needs a benchmark, and this is one of the major components of the market yet to develop.

ESG & Mandate Risk

Recent events in various US jurisdictions have highlighted an important set of questions around ESG investing. We believe these need to be considered by those holding a position of trust in the management of investor funds. Specifically, questions have been raised publicly about the nature and form of mandates governing the actions of funds.

In this blog we take no sides in the question of whether ESG investing adds value. Instead, we take a closer look at questions related to investment mandates under ESG and find that it may be worth those with fiduciary responsibilities taking their mandate into full and frank account.

Recent Challenges

Environmental, Social and Governance – ESG - investment platforms made unexpected headlines in the United States through Q3.

This included certain reports.

19 US state attorneys general wrote to BlackRock, arguing that the investment manager’s ESG investment policies may violate the ‘sole interest’ rule, which in the US requires that conflicts of interest in fiduciary relationships be avoided.

Attorneys General in Indiana and Louisiana issued warnings to their respective state pension boards that ESG investing may be a violation of their fiduciary duty.

West Virginia barred Blackrock, JPMorgan, Goldman Sachs, Morgan Stanley and Wells Fargo from contracting for new business in the state after determining that through ESG policies they were boycotting the fossil fuel industry.

Texas identified 10 companies, and 348 investment funds whom legislators labelled ‘boycott energy companies’, including BlackRock, Credit Suisse and UBS, prohibiting them from contracting with state agencies and local governments.

Our attention was drawn to this by a recent Wall Street Journal piece which noted that the principles invoked in the letters sent to Blackrock are “part of the common and statutory laws of almost every state.”

While it may be tempting to dismiss the Journal’s authors as partisans assembling contestable assertions, see here and here, we leave the tactical debate to others, for example:

Harvard Business Review:

o Yes, Investing in ESG Pays Off; versus

o An Inconvenient Truth About ESG Investing,

What we find interesting is that:

The various state-based challenges reignite a debate around fiduciary responsibilities that emerged when Corporate Social Responsibility, started to emerge in the early 2000’s; and, more importantly

ESG investment may be argued to contravene the Uniform Prudent Investor Act, adopted by 44 US states and the District of Columbia, which states:

No form of so-called "social investing" is consistent with the duty of loyalty if the investment activity entails sacrificing the interests of trust beneficiaries – for example, by accepting below-market returns -- in favor of the interests of the persons supposedly benefitted by pursuing the particular social cause.

The Journal’s writers, William Barr and Jed Rubenfeld, go on to note that “a defence to ESG investing asserts that ESG factors, though nonpecuniary, are material to profitability and that ESG investing will therefore produce superior outcomes.”

This appears contestable, as the varying Harvard studies amply prove, but when canvassing for views from among Martialis clients and contacts one message stood out: most managers have been inundated with requests for ESG-overlay and careful observance, not the opposite.

Fiduciary Duty in Australia

We hope to follow up on this blog with a more detailed look at the nature of fiduciary responsibilities in an Australian context. The aim will be to get a much clearer definitional picture from experts, so watch for that in coming issues.

What we do note is that there appear to be similar provisions within the Corporations Act to those written-in to the US’s Uniform Prudent Investor act. For example, a responsibility under the Australian Act is that responsible entities (of registered schemes) duties include acting “in the best interests of the members and, if there is a conflict between the members' interests and its own interests, [to] give priority to the members' interests."

Perhaps the risk for fund directors lies in the definition of what constitutes a member's interests? Is it to maximise returns with an ESG filter or overlay, or simply to maximise returns?

In our view, risk here can likely be distilled into to a fundamental question of fund mandate.

Where a fund has ensured beneficiaries are aware of the nature of the decisions being made – whether ESG-based or otherwise – a mandate sets the parameters within which a portfolio is managed, thus setting properly informed beneficiary expectations.

But what of funds that have started overlaying ESG filters without addressing beneficiaries or their mandate?

To us, this seems problematic.

A problematic greenium

As the market transparency of ESG investing modes develops it will be increasingly easy for fund beneficiaries to assess the decision-making path of fund managers.

To reinforce this, we note that Bloomberg has embarked on an extensive ESG program designed collect some data to the ESG metrics.

Bloomberg’s Environmental, Social & Governance (ESG Data) dataset offers ESG metrics and ESG disclosure scores for more than 14,000 companies in 100+ countries. The product includes as-reported data and derived ratios as well as sector and country-specific data points. In addition to the extensive ongoing data coverage, we provide historical data going back to 2006.

This allows Bloomberg subscribers to gain access quite remarkable decision-making tools and transparency.

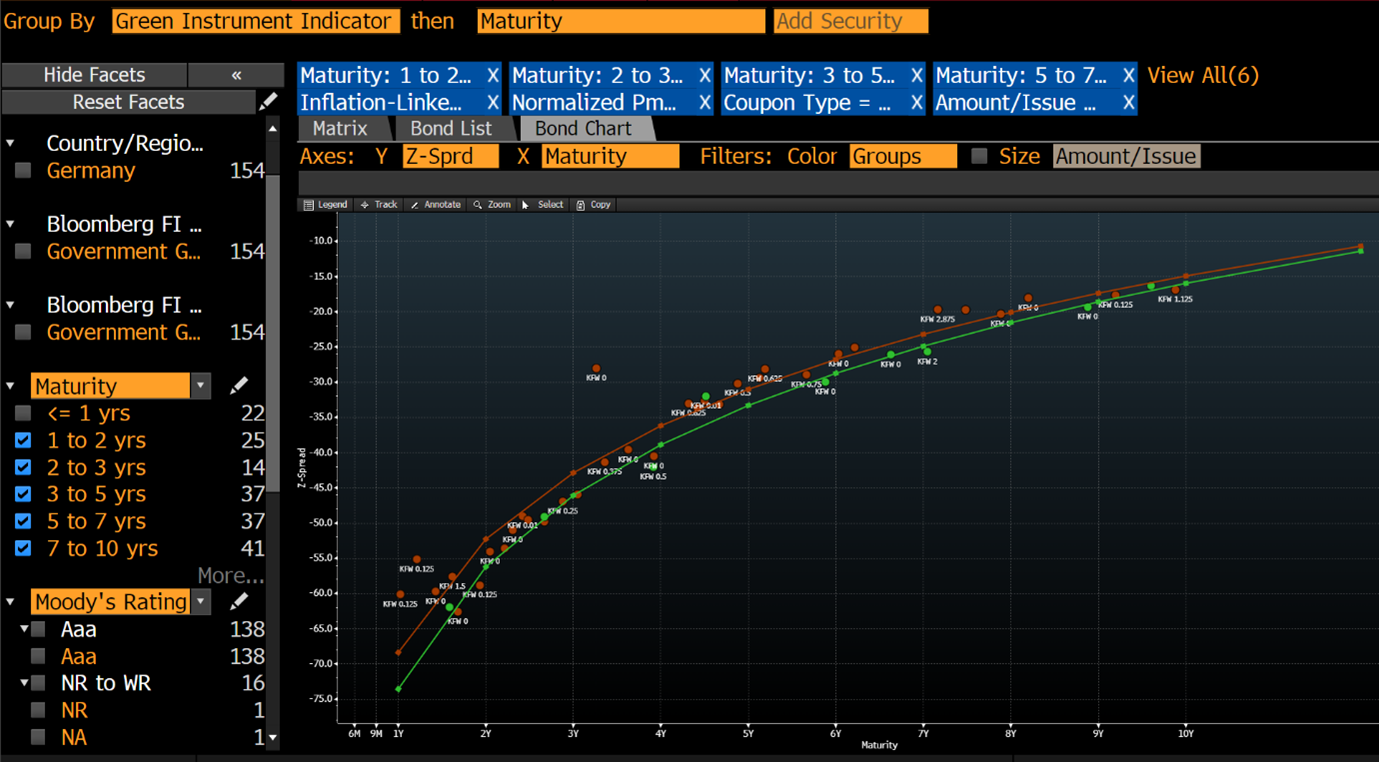

For example, here is a screenshot of Bloomberg’s Green Instrument Indicator:

Which means that transparency is assured.

What then of a situation in which, for example, a bond fund manager is considering a purchase of bonds/bunds of, say, a noted green issuer - the Federal Republic of Germany?

The German state issues both green and non-green bonds, and has gone to impressive lengths to distinguish between the two:

The use of proceeds from Green German Federal Securities always corresponds to federal expenditure from the previous year. Spending from the previous year’s budget that qualifies as “green” is assigned to the securities. The Green Bond Framework lists five main green expenditure categories that can be assigned to Green German Federal Securities.

These are:

Transport

International cooperation

Research, innovation and awareness raising

Energy and industry

Agriculture, forestry natural landscapes and biodiversity

Noting that the yield differential between a 10-year green and traditional bund is around 5.0 basis points, it’s not hard to see a potential fiduciary risk problem emerging.

If our bond fund manager notes the differing market yield representing the ‘greenium’ (which we imply as resulting in a lower monetary yielding outcome for the investor) and has no mandate for such a product we suggest there is a potential problem.

Why?